Health insurance and health care cost management (individual and group)

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

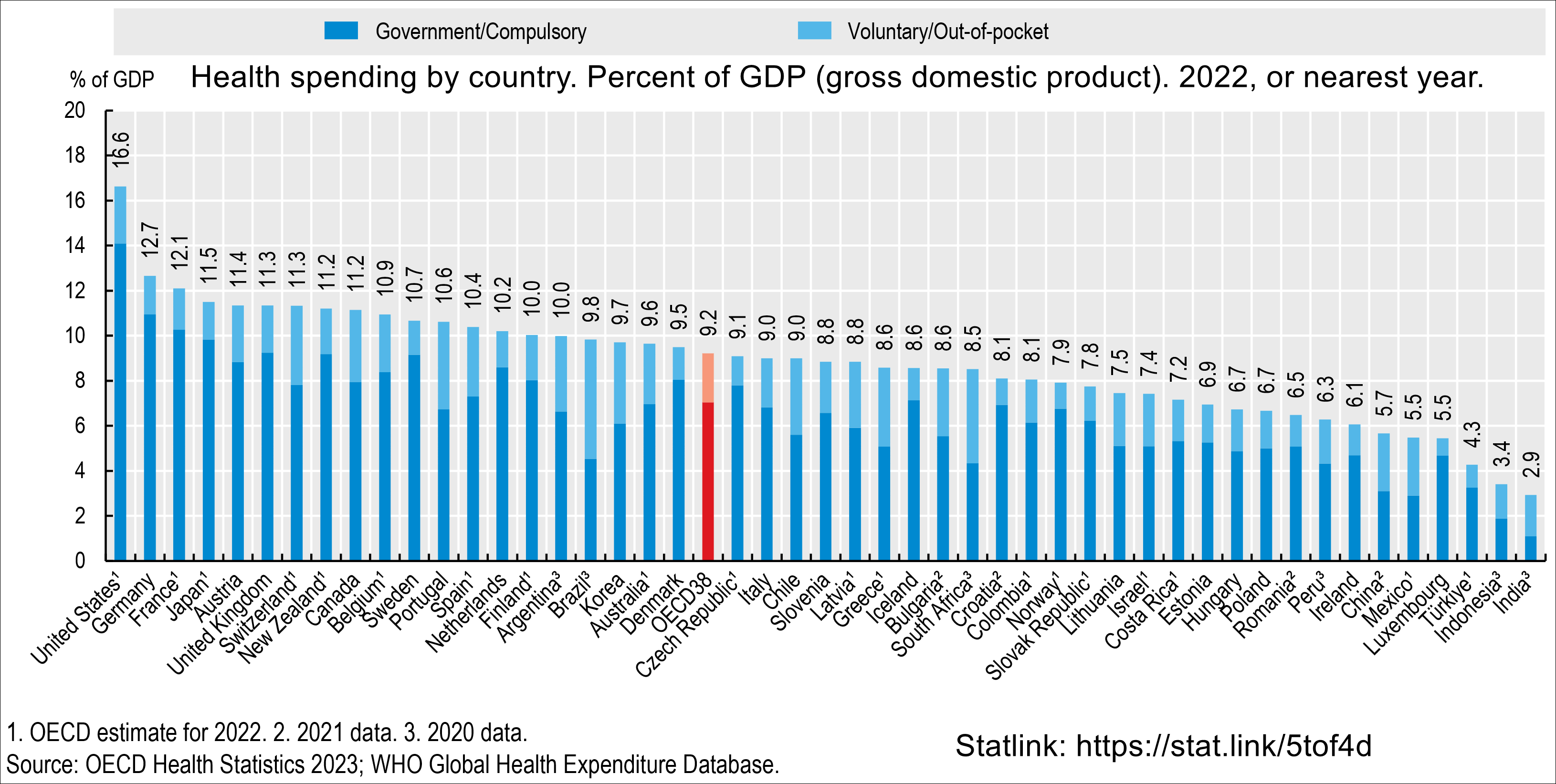

A financial plan is a fortress, meticulously constructed over decades to protect a client’s wealth. Yet, without a rigorous strategy for health care cost management, that fortress has no moat. A single catastrophic medical event can breach the walls, liquidating carefully compounded investment portfolios and triggering cascading tax liabilities. For the financial planner, mastering health insurance is not an administrative afterthought; it is the fundamental mechanism of risk transfer that ensures the rest of the plan survives contact with reality. To navigate this landscape, we must first understand the strict mathematical boundaries of cost-sharing, decode the architecture of managed care networks, and master the profound tax advantages of modern health savings vehicles.

Before we can evaluate different health plans, we must isolate the variables that dictate a client's out-of-pocket exposure. The cost-sharing structure of health insurance is essentially a chronological sequence of cash flow that begins the moment a client purchases a policy and accelerates the moment they seek care.

First is the baseline cost of admission. A health insurance premium is the fixed monthly cost paid by the insured to maintain active health insurance coverage. It must be paid regardless of whether the client ever sees a doctor. Because it is a baseline maintenance cost, monthly health insurance premium payments are explicitly excluded from the calculation of an insured individual's annual out-of-pocket maximum.

When care is actually needed, the risk-sharing mechanics activate in three distinct phases:

- Health Insurance Deductible: This represents the specific dollar amount the insured must pay out-of-pocket before the insurer initiates claim payments. Think of this as the client's upfront retention of risk.

- Copayments and Coinsurance: Once the deductible is met, the client and the insurer share costs. A health insurance copayment is a fixed dollar amount the insured is required to pay for a specific covered healthcare service (e.g., $40 for a specialist visit). Conversely, health insurance coinsurance represents the percentage of costs for a covered service the insured is responsible for paying after meeting the deductible (e.g., a 20% coinsurance on a surgical procedure).

- The Health Insurance Out-of-Pocket Maximum: This represents the absolute limit an insured will pay for covered in-network services during a plan year. Once this ceiling is breached, the insurer covers 100% of remaining eligible costs. It is the ultimate fail-safe protecting your client from medical bankruptcy.

When advising a client on health plan selection, you are primarily helping them negotiate a trade-off between premium costs, network flexibility, and administrative friction. We evaluate plan types by looking at two structural elements: the presence of a "gatekeeper" (the Primary Care Physician) and the permeability of the network "boundary."

HMOs and PPOs: The Anchors of Managed Care

An Health Maintenance Organization (HMO) is a fortress with a strict gatekeeper and an impermeable wall. An HMO plan requires the selection of a primary care physician (PCP). This doctor acts as the ultimate gatekeeper; an HMO plan requires a referral from a primary care physician to see a medical specialist. Furthermore, an HMO plan completely excludes coverage for out-of-network care outside of medical emergencies.

Conversely, a Preferred Provider Organization (PPO) relies on financial incentives rather than strict boundaries. A PPO plan does not require the insured to designate a primary care physician. Therefore, a PPO plan permits the insured to see medical specialists without obtaining a prior referral. It also features a permeable boundary: a PPO plan allows the insured to seek care from out-of-network healthcare providers. The catch? A PPO plan assesses higher out-of-pocket costs to the insured for out-of-network care compared to in-network care.

EPOs and POS Plans: The Hybrids

The Exclusive Provider Organization (EPO) and Point of Service (POS) plans mix and match these features.

- An EPO plan covers in-network healthcare services without requiring a referral to see a specialist (no gatekeeper), but like an HMO, an EPO plan strictly denies coverage for all out-of-network healthcare services except for medical emergencies.

- A POS plan operates as a managed care model requiring the designation of a primary care physician, meaning a POS plan requires a referral from a primary care physician to see an in-network medical specialist. However, like a PPO, a POS plan provides out-of-network healthcare coverage at a higher cost to the insured.

| Plan Type | Primary Care Physician (PCP) Required? | Referral Needed for Specialist? | Out-of-Network Coverage? (Non-Emergency) |

|---|---|---|---|

| HMO | Yes | Yes | No (Strictly excluded) |

| PPO | No | No | Yes (At higher cost) |

| EPO | No | No | No (Strictly denied) |

| POS | Yes | Yes (For in-network) | Yes (At higher cost) |

A High Deductible Health Plan (HDHP) generally features lower monthly premium costs than traditional HMO or PPO plans. In exchange, a High Deductible Health Plan mandates a higher annual minimum deductible than traditional health insurance plans. However, to incentivize wellness, a High Deductible Health Plan fully covers preventive healthcare services before the insured satisfies the annual deductible.

But the true power of the HDHP for the financial planner is that it unlocks the Health Savings Account (HSA).

The Ultimate Tax Vehicle

The HSA is arguably the most structurally advantageous account in the U.S. tax code. It features a "triple-tax advantage":

- Taxpayers can claim an above-the-line tax deduction for personal contributions to a Health Savings Account. Furthermore, employee contributions to a Health Savings Account made through payroll deductions avoid federal income taxes and avoid FICA payroll taxes.

- Investment earnings and interest generated within a Health Savings Account grow completely tax-deferred.

- Distributions from a Health Savings Account are entirely tax-free when applied toward qualified medical expenses.

Unlike a flexible spending account, unspent funds within a Health Savings Account automatically roll over to subsequent years without limitation. A Health Savings Account is fully portable and remains the property of the employee upon job termination.

Eligibility Rules and Traps

Because the tax benefits are so profound, the IRS guards the gates fiercely. A taxpayer must be actively covered by a qualifying High Deductible Health Plan to contribute to a Health Savings Account. An individual claimed as a tax dependent by another person is prohibited from contributing.

Crucially, enrollment in any part of Medicare immediately disqualifies an individual from making further contributions to a Health Savings Account.

For funding limits, remember that employer contributions to an employee Health Savings Account directly reduce the remaining annual contribution limit for the employee. For families, married couples sharing a single family High Deductible Health Plan must split the annual family Health Savings Account contribution limit.

The Age 55 Catch-Up Quirk: Individuals aged 55 and older are eligible to make an annual catch-up contribution to a Health Savings Account. The Health Savings Account catch-up contribution limit for individuals aged 55 and older is fixed at $1,000. However, HSAs are strictly individual accounts. Therefore, each spouse in a married couple aged 55 or older must open separate Health Savings Accounts to both make individual catch-up contributions.

Strategic Withdrawals and Inheritance

What counts as a qualified medical expense? The list is broader than many clients realize. Health Savings Account funds can be used tax-free to purchase over-the-counter medications without a physician prescription, and they can be used tax-free to purchase menstrual care products.

For retirees, HSA funds can be used tax-free to pay for Medicare Part B premiums and Medicare Part D premiums. However, take strict note: Health Savings Account funds are strictly prohibited from paying Medicare Supplemental Insurance (Medigap) premiums.

If a client needs cash for non-medical reasons, penalties depend on age:

- Before age 65: Non-qualified distributions from a Health Savings Account taken before age 65 incur a 20 percent penalty AND are subject to ordinary income tax.

- After age 65: Non-qualified distributions from a Health Savings Account taken after age 65 are exempt from the 20 percent penalty, but remain subject to ordinary income tax. (At 65, the HSA effectively acts as a Traditional IRA for non-medical expenses).

Finally, estate planning for HSAs is deeply sensitive to beneficiary designation. A surviving spouse who inherits a Health Savings Account assumes full ownership of the account as their own Health Savings Account. In contrast, a non-spouse beneficiary inheriting a Health Savings Account must recognize the fair market value of the account as taxable income, effectively destroying the tax-free shell.

While the HSA is a personal asset, Flexible Spending Accounts (FSAs) and Health Reimbursement Arrangements (HRAs) are deeply tied to the employer.

A Health Care Flexible Spending Account permits employees to allocate pre-tax salary toward qualified medical expenses. The entire annual election amount for a Health Care Flexible Spending Account must be immediately available to the employee on the first day of the plan year.

However, an FSA is legally owned by the sponsoring employer. Because of this, Flexible Spending Account funds are typically forfeited immediately upon an employee terminating employment. Furthermore, a Health Care Flexible Spending Account enforces a strict forfeiture rule (the "use-it-or-lose-it" rule) for unspent funds at the conclusion of the plan year.

Employers can offer minor reprieves from forfeiture, but they are limited. An employer can optionally establish a grace period of up to two and a half months for employees to utilize expiring Flexible Spending Account funds, OR an employer can optionally permit employees to carry over a limited IRS-specified dollar amount of unused Flexible Spending Account funds to the following year. Take note: an employer is strictly prohibited from offering both a Flexible Spending Account grace period and a rollover provision simultaneously.

FSA and HSA Interaction: An employee enrolled in a general-purpose Health Care Flexible Spending Account automatically loses eligibility to contribute to a Health Savings Account. The IRS considers a general-purpose FSA to be impermissible secondary health coverage. However, an individual can actively contribute to a Limited-Purpose Flexible Spending Account while simultaneously funding a Health Savings Account, because a Limited-Purpose Flexible Spending Account restricts expense reimbursements strictly to dental and vision care costs.

Lastly, do not confuse the FSA with the Health Reimbursement Arrangement (HRA). An HRA is funded exclusively through employer contributions; employees are strictly prohibited from making financial contributions to a Health Reimbursement Arrangement. Because it is employer money, the employer holds sole discretion over whether unused funds in a Health Reimbursement Arrangement roll over to subsequent years.

Health insurance planning does not exist in a vacuum; it operates on a playing field strictly regulated by federal law. Understanding these regulations is vital when navigating job transitions, early retirements, or dependent transitions.

The Affordable Care Act (ACA)

The ACA structurally altered health insurance underwriting and employer responsibilities. To protect individuals, the Affordable Care Act prohibits health insurance providers from denying coverage based on pre-existing medical conditions, and prohibits health insurance plans from enforcing lifetime maximum dollar limits on essential health benefits. It also mandates health insurance plans to extend dependent coverage eligibility for children up to age 26.

For corporate clients, the ACA enforces an "employer mandate." Large employers are required by the Affordable Care Act mandate to offer affordable health insurance to full-time employees. For the purposes of this mandate, the Affordable Care Act defines a full-time employee as an individual working an average of at least 30 hours per week.

COBRA Continuation Coverage

When a client loses their job, they face a dangerous vulnerability period. COBRA is the federal safety net allowing individuals to temporarily maintain their exact group health coverage.

COBRA continuation coverage mandates apply exclusively to employers maintaining 20 or more full-time equivalent employees. If the client is eligible, they can expect the following timelines:

18 Months of Coverage:

- COBRA guarantees up to 18 months of continuation coverage for an employee experiencing a voluntary or involuntary termination of employment. (Note: An employer is not required to offer COBRA continuation coverage if an employee is terminated for gross misconduct).

- COBRA guarantees up to 18 months of continuation coverage for an employee experiencing a reduction in work hours.

29 Months of Coverage (Disability Extension):

- An individual deemed disabled by the Social Security Administration can receive an 11-month extension to the standard 18-month COBRA continuation period.

36 Months of Coverage:

- COBRA guarantees up to 36 months of continuation coverage for the surviving spouse of a deceased covered employee.

- COBRA guarantees up to 36 months of continuation coverage for a spouse following a legal divorce from a covered employee.

- COBRA guarantees up to 36 months of continuation coverage for a dependent child who formally loses dependent status (e.g., aging out at 26).

- COBRA guarantees up to 36 months of continuation coverage for spouses and dependents of an employee who becomes entitled to Medicare.

This safety net is not cheap. The maximum premium amount a former employee can be assessed for standard COBRA continuation coverage is 102 percent of the total plan cost (the 100% premium cost plus a 2% administrative fee). If the former employee utilizes the disability provision, the premium for the 11-month COBRA disability extension period can be increased to 150 percent of the total plan cost.

Understanding these timelines and costs allows a financial planner to bridge the gap between employment, securing the client's financial fortress until a more permanent solution can be found.