Market cycles

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

The global economy does not move in a straight line; it breathes. It operates as a massive, complex thermodynamic system that undergoes a continuous, natural fluctuation of the economy between periods of expansion and contraction. For the financial planner, understanding this rhythmic fluctuation is the fundamental difference between reacting blindly to a client’s panic and strategically anticipating the next movement of global capital. When you sit across from a client terrified by a declining portfolio, you are not merely looking at red numbers on a screen—you are observing the friction of a transition between distinct phases of the business cycle and stock market cycles. Mastering these cycles allows you to diagnose the present, forecast the probable future, and align client investment strategies to navigate—and capitalize on—these inevitable shifts.

The business cycle represents the macroeconomic reality of production, employment, and profit. It consists of four distinct phases known as expansion, peak, contraction, and trough.

An expansion phase is characterized by the economic engine running smoothly and accelerating. During this time, we observe increasing economic activity, rising corporate profits, and declining unemployment. Businesses are hiring, consumers are spending, and the velocity of money increases.

Eventually, the economy reaches its physical and monetary limits, entering the peak phase. This represents the absolute highest point of economic output before a period of decline begins. Resources are fully utilized, labor is scarce, and prices begin to rise, forcing central banks to intervene.

Following the peak, the economy enters a contraction phase. This involves slowing economic growth, declining corporate profits, and rising unemployment. Businesses pull back on capital expenditures, and consumers tighten their wallets. If this contraction is severe enough, it enters the territory of a recession. A technical economic recession is commonly defined by economists as two consecutive quarters of negative Gross Domestic Product (GDP) growth.

Finally, the contraction exhausts itself, arriving at the trough phase. This marks the lowest point of economic activity before a new expansion cycle begins. The excesses of the previous cycle have been purged, creating a baseline for new growth.

The Official Arbiter: You might wonder who actually declares these phases. The National Bureau of Economic Research (NBER) officially dates the peaks and troughs of the United States business cycle. They look at a broad array of coincident economic indicators to determine exactly when the economy transitions from one phase to the next.

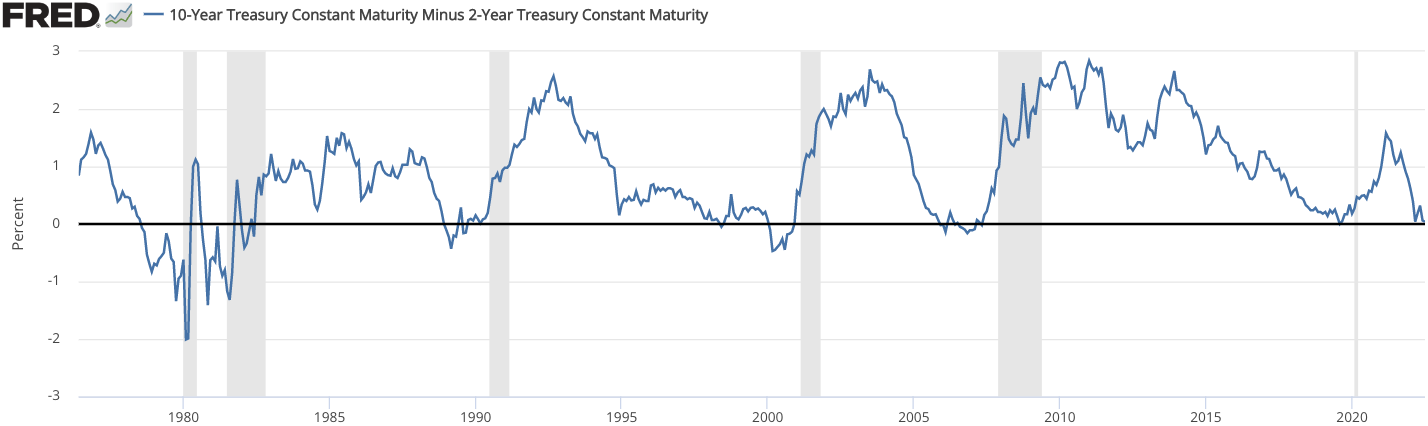

The Canary in the Coal Mine: Yield Curve Inversion

How do we know a contraction is coming before it arrives? One of the most reliable leading indicators in modern finance is the bond market. Specifically, a yield curve inversion frequently precedes the contraction phase of the broader business cycle.

Under normal circumstances, investors demand a higher yield to lock up their money for a longer period due to the risks of inflation and time. However, an inverted yield curve occurs when short-term government debt instruments offer higher yields than long-term government debt instruments. This happens when central banks aggressively raise short-term interest rates to cool an overheating economy, while long-term bond investors simultaneously drive down long-term yields because they expect future economic growth and inflation to collapse. When you see the yield on a 2-year Treasury eclipse the yield on a 10-year Treasury, the bond market is signaling that a contraction is highly probable.

Here is a paradox you will frequently encounter with clients: The economy is shedding jobs, GDP is negative, the news is entirely bleak—yet the stock market is suddenly surging upward. Your clients will ask if the market is entirely disconnected from reality.

It is not disconnected; it is simply looking ahead. The stock market cycle typically leads the economic business cycle by six to nine months. The stock market functions like the headlights of a car, while the business cycle is the car itself. Equity markets generally price in economic recoveries before official economic data reflects an improvement. By the time the NBER officially declares the end of a recession, the stock market has often already experienced a massive rally.

Just like the business cycle, the stock market cycle consists of four distinct phases, driven by the psychology and behavior of different types of market participants. These phases are known as accumulation, mark-up, distribution, and mark-down.

- The Accumulation Phase: This occurs at the darkest hour of an economic contraction. The accumulation phase occurs when institutional investors begin buying assets while general market sentiment remains heavily bearish. The news is terrible, the public is terrified, but the "smart money" recognizes that prices are irrational and the trough is near.

- The Mark-Up Phase: As economic conditions slowly begin to show signs of life, the broader market catches on. The mark-up phase is characterized by rising stock prices, increasing trading volume, and growing participation from retail investors. The trend is clearly upward, and confidence returns.

- The Distribution Phase: The market eventually becomes overheated. The distribution phase occurs when institutional investors begin selling their accumulated assets to late-arriving buyers. Retail investors are buying aggressively based on euphoric headlines and fear of missing out, while the smart money is quietly taking profits and unwinding their positions.

- The Mark-Down Phase: Once the institutional support vanishes, the market rolls over. The mark-down phase features declining stock prices and widespread negative sentiment among market participants. Panic selling ensues until the assets become cheap enough to trigger a new accumulation phase.

Understanding where we are in the cycle is interesting, but for a financial planner, the application of this knowledge is what generates value. This brings us to sector rotation.

Sector rotation is an active investment strategy involving the movement of capital among different equity sectors based on the current stage of the economic cycle. Because different industries react uniquely to interest rates, inflation, and consumer demand, sector rotation seeks to maximize returns by overweighting industry sectors expected to outperform in the upcoming economic phase.

By analyzing the characteristics of each business cycle phase, we can anticipate which sectors hold the fundamental advantage.

1. Early Recovery Phase

The early recovery phase of the business cycle follows a trough and is typically associated with low interest rates and expansive monetary policy as central banks attempt to stimulate growth. Money is cheap, and the economy is just starting to wake up.

- Financials: The Financials sector generally outperforms the broader market during the early recovery phase of the business cycle. Banks borrow at rock-bottom short-term rates and lend at higher long-term rates (a steep yield curve), rapidly expanding their net interest margins.

- Consumer Discretionary: Consumer discretionary stocks typically perform well during the early recovery phase due to anticipated increases in consumer spending. As employment stabilizes, consumers finally buy the cars, appliances, and luxury goods they deferred during the recession.

- Real Estate: Real Estate equities generally benefit from the low interest rates present during the early stages of an economic recovery. Cheap mortgages spur homebuying, and low borrowing costs allow commercial developers to initiate new projects.

2. Mid-Cycle Expansion Phase

As the recovery matures, we enter the mid-cycle. The mid-cycle expansion phase is characterized by moderate economic growth and peaking corporate profit margins. The initial explosive recovery slows into a steady, sustainable hum.

- Information Technology: Information Technology sectors tend to lead the equity market during the mid-cycle expansion phase. As corporations enjoy peak profit margins, they look to invest those profits into software and hardware that will improve efficiency and maintain their competitive edge.

- Industrials: The Industrials sector generally performs well during the mid-cycle expansion phase due to increasing capital expenditures by businesses. Manufacturing plants are expanded, fleets are upgraded, and heavy machinery is purchased as companies gain confidence in the longevity of the economic expansion.

3. Late-Cycle Economic Phase

The boom eventually creates strain. The late-cycle economic phase is associated with rising inflation, tight monetary policy, and slowing economic growth. Central banks are raising interest rates to combat inflation, which begins to choke off the expansion.

- Energy: Energy stocks often outperform during the late-cycle phase due to rising commodity prices and elevated inflation levels. As an economy operates at maximum capacity, the demand for oil and gas pushes prices upward, directly benefiting the profit margins of energy producers.

- Materials: The materials sector frequently shows relative price strength during the late-cycle phase as raw material demand peaks. The cumulative effect of years of expansion means intense demand for metals, chemicals, and construction materials just as the cycle tops out.

4. Contraction Phase (Recession)

When the tight monetary policy of the late-cycle finally breaks the economy, a contraction begins. In this environment, growth stocks are punished, and investors seek safety. Defensive equity sectors historically outperform the broader stock market during a recession or contraction phase. These are companies that provide goods and services people must buy, regardless of whether they just lost their job.

- Consumer Staples: Consumer staples represent a defensive sector providing essential goods with inelastic demand during economic downturns. People may stop buying luxury watches (Consumer Discretionary), but they will not stop buying toothpaste, bread, and toilet paper.

- Utilities: Utilities function as a defensive sector because consumers continue to pay for essential services regardless of broader economic conditions. Keeping the lights on and the water running is a non-negotiable household expense, providing these companies with highly predictable, stable cash flows.

- Healthcare: Healthcare is considered a defensive market sector due to the consistent human need for medical services in all economic environments. Illness and injury do not respect the business cycle; thus, pharmaceutical companies and healthcare providers maintain steady revenues even deep in a trough.

Summary of Sector Rotation Strategy

| Business Cycle Phase | Economic Characteristics | Outperforming Equity Sectors |

|---|---|---|

| Early Recovery | Low interest rates, expansive monetary policy | Financials, Consumer Discretionary, Real Estate |

| Mid-Cycle | Moderate economic growth, peaking profit margins | Information Technology, Industrials |

| Late-Cycle | Rising inflation, tight monetary policy, slowing growth | Energy, Materials |

| Contraction | Slowing growth, declining profits, rising unemployment | Consumer Staples, Utilities, Healthcare |

For the CFP® professional, communicating this framework turns client anxiety into strategic patience. When a client sees their portfolio shifting heavily into consumer staples and healthcare, you can explain that the yield curve has inverted and you are preparing for a contraction. When the market surges despite terrible economic news, you can explain the accumulation phase and the six-to-nine-month leading nature of equities. You are not just managing assets; you are managing the client's relationship with time.