Types of investment risk

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Picture a fleet of commercial ships navigating the open ocean. A sudden, violent squall rolls in, churning the sea and tossing every vessel, regardless of its size, its captain, or the cargo it carries. This is the inescapable reality of the environment—no ship is immune to the weather. Now, imagine a single ship within that fleet sailing into calm waters, only to slowly sink because of a localized, poorly sealed valve in its own hull. The weather did not sink the ship; a specific, structural flaw did.

For a financial planner constructing a client’s portfolio, the open ocean represents the financial markets. The macroeconomic forces that toss every asset are your systematic risks, while the specific flaws inherent to individual companies are your unsystematic risks. Understanding the precise boundary between the risks you can control through portfolio construction and the risks you must merely endure is the mathematical foundation of modern portfolio theory, and a central pillar of CFP® practice.

When a client looks at their monthly statement, they experience volatility as a singular, emotional event. But mathematically, total risk comprises the sum of both systematic risk and unsystematic risk.

Total Risk = Systematic Risk + Unsystematic Risk

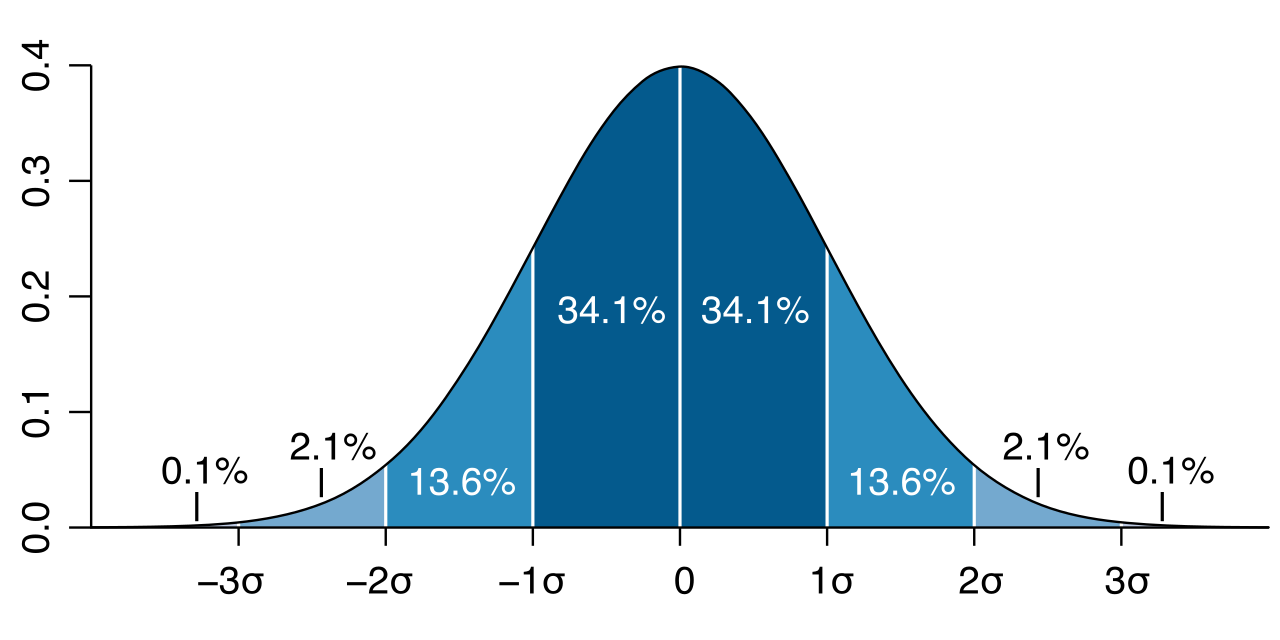

To capture this entire spectrum of volatility, we use standard deviation. Standard deviation is the statistical metric used to measure the total risk of an investment or portfolio. It does not care why an asset's price deviated from its expected return—whether it was a global pandemic or a CEO scandal—it simply measures the magnitude of the total historical deviation.

However, as a portfolio manager, you cannot treat all risk equally. You must dissect total risk into its two constituent parts.

Systematic risk is the uncertainty inherent to the entire market or entire market segment. Because it is driven by macroeconomic factors like inflation, wars, and sweeping interest rate policy, systematic risk cannot be eliminated through portfolio diversification. You cannot diversify away from a storm if your entire portfolio is on the same ocean.

Because standard deviation measures total risk, it is the wrong tool to measure systematic risk in isolation. Instead, beta is the primary metric used to measure the systematic risk of an investment relative to the overall market. A beta of 1.0 means the asset experiences the same systematic volatility as the broader market; a beta of 1.5 means it is 50% more volatile.

Financial professionals commonly use the mnemonic PRIME to remember the primary types of systematic risk that affect entire markets.

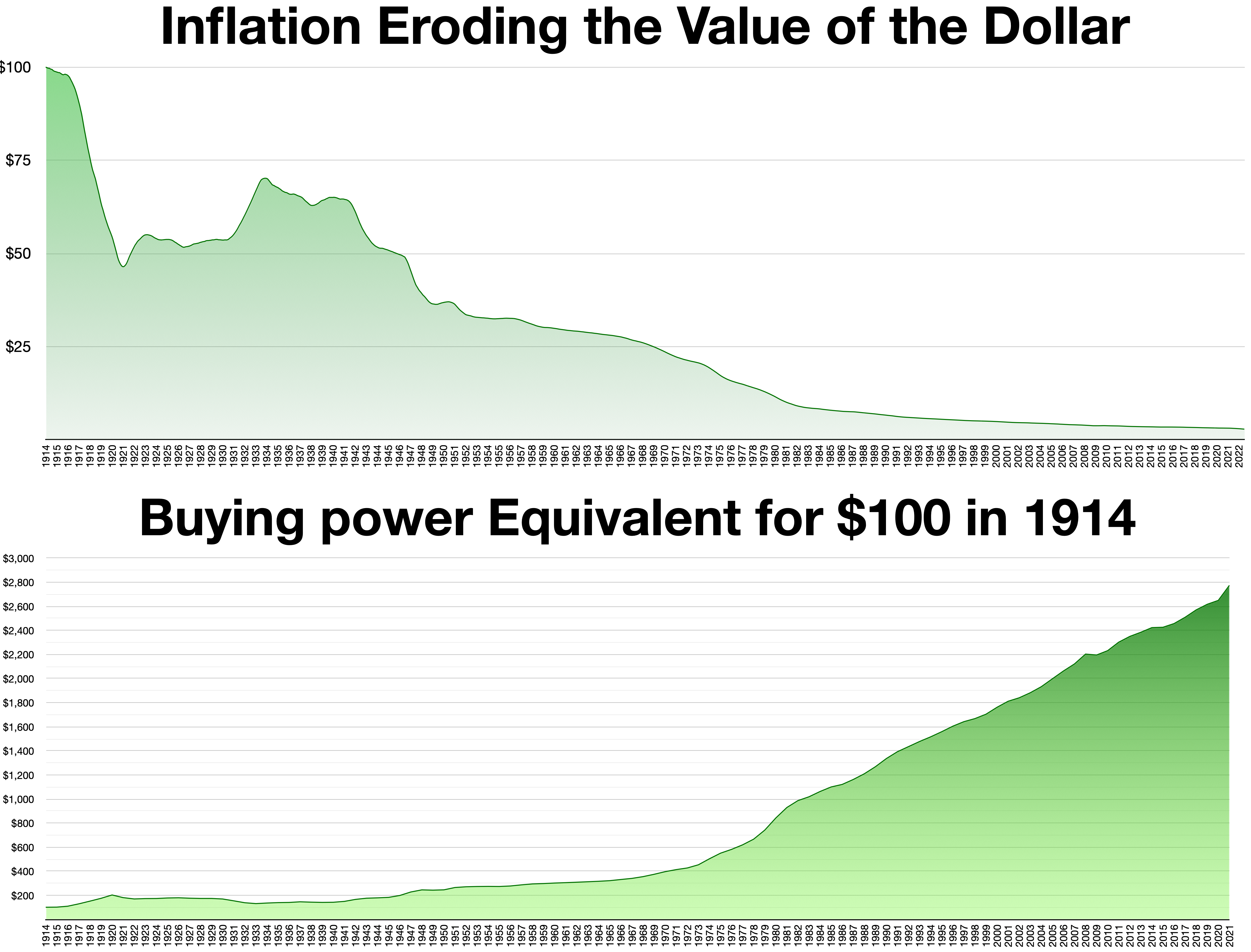

P: Purchasing Power Risk

Purchasing power risk is the danger that inflation will erode the real value of an investor's principal and investment returns. When you sit across from a retiring client who wants a "conservative" 100% bond portfolio to avoid volatility, you must warn them of this silent thief. Fixed-income securities are particularly vulnerable to purchasing power risk due to their fixed nominal payments. If a bond pays $50 a year, but inflation rises by 5%, the real purchasing power of that $50 drops. Conversely, equities generally provide a hedge against purchasing power risk over long time horizons, as companies can raise prices to keep pace with inflation.

R: Reinvestment Rate Risk

Imagine buying a bond yielding 6%. You rely on reinvesting those 6% coupon payments to achieve compounding interest. Reinvestment rate risk is the possibility that an investor will be forced to reinvest those cash flows at a lower interest rate than the original investment's yield.

Crucial Exam Note: Zero-coupon bonds have no reinvestment rate risk because there are no periodic coupon payments to reinvest during the bond's life. The return is locked in entirely by the discount at purchase and the par value at maturity.

I: Interest Rate Risk

Interest rate risk is the potential for investment losses resulting from fluctuations in prevailing market interest rates. As a foundational law of finance, bond prices have an inverse relationship with market interest rates. If new bonds are issued at 7%, your client’s older bonds yielding 4% immediately become less attractive, and their secondary market value drops.

M: Market Risk

Sometimes, the entire stock market drops due to investor panic, economic recession, or geopolitical events. Market risk is the likelihood that the value of an investment will decrease due to broad stock market declines.

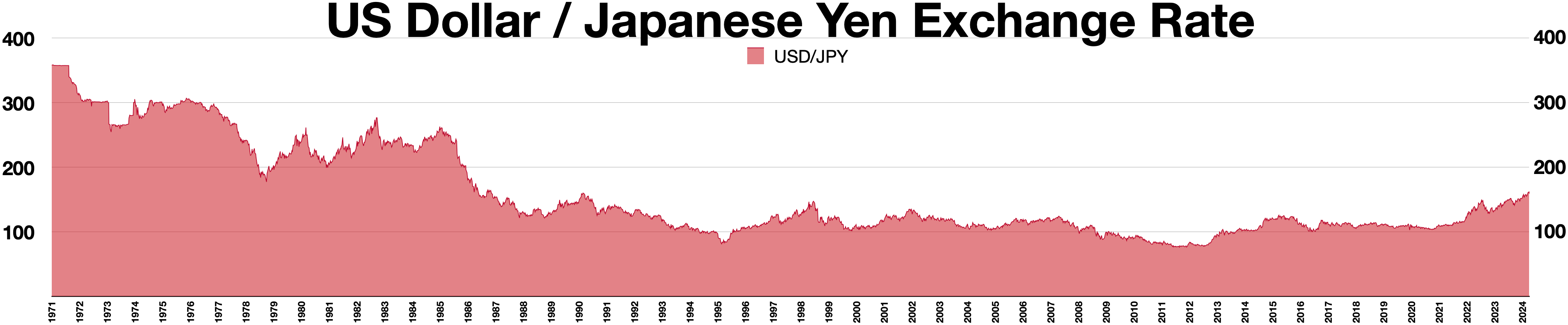

E: Exchange Rate Risk

In a globalized economy, your clients will likely hold international assets. Exchange rate risk is the exposure to financial losses caused by fluctuations in the value of one currency against another currency. If a client owns a Japanese stock that appreciates in Yen, but the Yen depreciates significantly against the US Dollar, your client’s net return in dollars may still be negative.

If systematic risk is the weather, unsystematic risk is the leaky valve on a single ship. Unsystematic risk is the uncertainty associated with a specific company or a specific industry. If a pharmaceutical company fails FDA trials, its stock plummets, but the broader S&P 500 barely notices.

Because this risk is localized, unsystematic risk is also known as diversifiable risk or idiosyncratic risk.

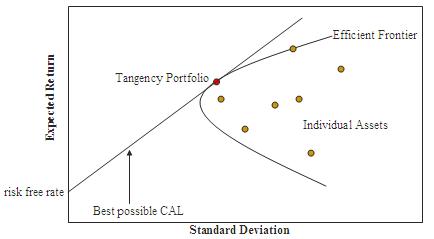

The Magic of Diversification

Unlike systematic risk, unsystematic risk can be largely eliminated by constructing a well-diversified portfolio of imperfectly correlated assets. By blending assets that do not move in lockstep, the idiosyncratic failures of one company are offset by the idiosyncratic successes of another.

Historically and mathematically, a portfolio containing approximately 15 to 20 randomly selected stocks can eliminate the majority of unsystematic risk. Adding a 50th or 100th stock provides drastically diminishing marginal returns in terms of risk reduction.

Specific Types of Unsystematic Risk

CFP® candidates must be able to identify specific manifestations of unsystematic risk in client scenarios.

Business Risk vs. Financial Risk

These two risks are frequently tested together because they relate to the corporate structure of the companies your clients invest in.

| Risk Type | Definition | The CFP® Scenario Application |

|---|---|---|

| Business Risk | Relates to the uncertainty of a company's operating income and the inherent nature of the company's core operations. | A typewriter company facing obsolescence, or a startup with a brilliant idea but no revenue. This is purely operational. |

| Financial Risk | The additional risk placed on common stockholders as a result of a company's decision to use debt financing. | A highly leveraged company that must meet massive debt obligations before paying common shareholders. This is a capital structure risk. |

Default (Credit) Risk

Default risk—also commonly referred to as credit risk—is the probability that a borrower will fail to make timely payments of interest or principal. When evaluating corporate or municipal bonds, this is a paramount concern. However, United States Treasury securities are generally considered by market participants to be free of default risk because the U.S. government holds the authority to tax and print sovereign currency.

Liquidity Risk vs. Marketability Risk

These terms are often used interchangeably by laypeople, but in financial academia, they describe distinct structural problems in secondary markets.

- Liquidity risk is the inability to sell an asset quickly without experiencing a significant concession in the asset's sale price. You can always sell a house in 24 hours if you drop the price by 60%. Thus, real estate investments typically possess a high degree of liquidity risk.

- Marketability risk is the inability to find a willing buyer for an asset in a timely manner regardless of the asset's price. Think of an obscure, privately held partnership share. You might offer it for pennies on the dollar, but if there is literally no active market or interested buyer, the asset suffers from marketability risk.

Country Risk and Regulatory Risk

- Country risk encompasses the economic and political stability of a foreign nation where an investment is physically or legally located. A coup d'état, nationalization of assets, or sudden capital controls all fall under this umbrella.

- Regulatory risk is the potential that changes in laws or government regulations will negatively impact a specific business or investment sector. For example, if Congress passes a sudden ban on specific carbon emissions, coal companies suffer a massive, localized regulatory shock.

Call Risk

Finally, we must look at a risk that creates a devastating feedback loop for bondholders. Call risk is the danger that a bond issuer will redeem a callable bond prior to maturity during a period of declining interest rates.

Why this matters in practice: Call risk rarely happens in isolation. When interest rates fall, issuers call their bonds to refinance at the new, cheaper rates. This forces the investor to take their returned principal and immediately face Reinvestment Rate risk, desperately trying to find yield in a newly lowered interest rate environment.

When analyzing a client case study on the CFP® exam, your first filter for any portfolio problem should be: Is this risk systematic or unsystematic?

If the client is heavily concentrated in a single employer stock, they are drowning in diversifiable, idiosyncratic risk. The solution is portfolio diversification (15-20 stocks). But if the client has a perfectly diversified index fund and is terrified of a looming recession, no amount of equity diversification will protect them from Market (Systematic) risk. You must use different asset classes, or manage their behavioral expectations, to navigate the storm.