Non-qualified plan rules and options

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Imagine the tax code as a heavily engineered landscape. Most employees travel along the public highway of qualified retirement plans like the 401(k)—a system built with strict speed limits, mandatory on-ramps, and rigid non-discrimination testing to ensure everyone travels at relatively similar speeds. But for highly compensated executives, this public highway is fundamentally inadequate; statutory contribution limits artificially cap their ability to replace their pre-retirement income. To bridge this gap, tax law permits the construction of a private airspace: non-qualified deferred compensation (NQDC). By stepping outside the rigid constraints of the Employee Retirement Income Security Act (ERISA), corporations can engineer bespoke, limitless compensation packages for top talent. However, this private airspace is governed by a punishing physics of its own. If the aerodynamic rules of constructive receipt, the economic benefit doctrine, and Internal Revenue Code Section 409A are violated, the structure crashes, triggering immediate, devastating tax consequences for the executive.

As financial planners, you deal with qualified plans daily. You know that to receive the tax advantages of a 401(k) or pension, a company must pass complex testing to prove they aren't favoring the C-suite.

Non-qualified deferred compensation plans allow employers to selectively provide benefits to highly compensated employees without violating qualified plan non-discrimination testing rules. Because they operate outside this framework, non-qualified deferred compensation plans are not subject to the statutory contribution limits imposed on qualified retirement plans. An executive earning $2 million a year cannot live on a $23,000 deferral limit; an NQDC plan allows them to defer hundreds of thousands of dollars, allowing for true income replacement in retirement.

But the IRS does not grant limitless deferrals without demanding a tradeoff. For the employer, the tradeoff is tax timing. In a qualified plan, the employer deducts a contribution today, even though the employee isn't taxed until decades later. In the non-qualified realm, the IRS enforces a strict matching principle: employers cannot take a tax deduction for non-qualified deferred compensation until the specific taxable year the employee actually recognizes the compensation as ordinary income.

Furthermore, the executive loses the portability we take for granted in the qualified world. When an executive retires, non-qualified deferred compensation plans do not offer tax-free rollover options into Individual Retirement Accounts (IRAs) or qualified retirement plans. The payout schedule they select is the payout schedule they are stuck with.

The Top-Hat Exemption

To legally bypass the heavy hand of ERISA, a plan must qualify as a "Top-Hat" plan. A Top-Hat plan is an unfunded deferred compensation plan maintained by an employer strictly for a select group of management or highly compensated employees.

If a plan meets this narrow definition, it enjoys incredible freedom. Top-Hat plans are exempt from the participation, vesting, funding, and fiduciary requirements of the Employee Retirement Income Security Act (ERISA).

To understand non-qualified plans, you must understand the two invisible forces of the tax code that threaten to tax an executive prematurely: the Constructive Receipt Doctrine and the Economic Benefit Doctrine.

The Constructive Receipt Doctrine states that income is taxable to an individual when funds are officially credited to the individual's account, set apart, or otherwise made available to the individual.

You cannot turn your back on money that is already yours and claim you haven't received it. If your boss hands you a bonus check and you say, "Hold onto this until I retire," the IRS says you are in constructive receipt of that money today. Therefore, an employee must formally enter into a non-qualified deferred compensation agreement before the underlying compensation is actually earned to legally avoid the constructive receipt doctrine.

The Economic Benefit Doctrine focuses not on access, but on guaranteed wealth creation. This doctrine causes an employee to face immediate taxation when employer funds are irrevocably placed into a trust or fund for the employee's sole benefit.

If an employer puts $100,000 into a vault, locks it, gives the executive the only key, and legally bars the company's creditors from ever touching it, an economic benefit has been conferred today, even if the executive cannot open the vault until age 65.

The Shield: Substantial Risk of Forfeiture

How do we defer taxation if these two doctrines are constantly pulling income into the present taxable year? We introduce a vulnerability.

Deferred compensation is not currently taxable to an employee if the right to ultimately receive the compensation remains subject to a substantial risk of forfeiture.

What constitutes this risk? A substantial risk of forfeiture exists if an employee's rights to receive deferred compensation are legally conditioned upon the future performance of substantial services for the employer. If the executive quits tomorrow, they lose the money. Because they might lose it, it isn't truly theirs yet, and the IRS refrains from taxing it.

Note on Payroll Taxes: While income tax is deferred by these mechanisms, payroll taxes operate on a different clock. Payroll taxes such as FICA and FUTA are generally due on non-qualified deferred compensation when the services are performed or when the substantial risk of forfeiture lapses. The moment the executive vests in the promised amount, FICA takes its cut, even if the income tax is deferred for another twenty years.

Executives are naturally paranoid. An employer's promise to pay $5 million in twenty years is only as good as the company's future solvency. Executives want their deferred money separated from the company's daily cash flow. To do this, employers use specific trust structures, balancing the executive's desire for security against the catastrophic tax triggers of the economic benefit doctrine.

The Rabbi Trust

Named after the first IRS private letter ruling approving its use for a clergyman, a Rabbi trust is an irrevocable trust used by employers to hold assets that fund non-qualified deferred compensation obligations.

Here is the brilliant compromise of the Rabbi trust: Placing assets in a Rabbi trust does not trigger the economic benefit doctrine for the employee because the assets remain subject to employer creditors. If the employer goes bankrupt, the executive stands in line with the rest of the unsecured creditors. Therefore, assets held within a Rabbi trust remain completely subject to the claims of the employer's general creditors in the event of employer bankruptcy.

The Rabbi trust protects the executive from change of heart or change of management (e.g., a hostile takeover), but it does not protect them from the company's insolvency.

The Secular Trust

What if the executive demands absolute protection from bankruptcy? The employer can use a Secular trust. A Secular trust is an irrevocable trust for non-qualified deferred compensation where the trust assets are fully protected from the employer's general creditors.

But remember the physics of taxation: absolute protection triggers the economic benefit doctrine. Because the money is now guaranteed, employer contributions made to a Secular trust are immediately taxable to the employee because the assets are protected from employer creditors.

Because the employee is taxed immediately, the corporate tax symmetry rule kicks in: an employer receives an immediate tax deduction for contributions made to a Secular trust.

| Feature | Rabbi Trust | Secular Trust |

|---|---|---|

| Creditor Protection | None (Subject to employer creditors) | Absolute (Protected from employer creditors) |

| Tax to Employee | Deferred until distributed | Immediate (upon contribution/vesting) |

| Deduction to Employer | Deferred until distributed | Immediate |

| Economic Benefit Doctrine | Avoided | Triggered |

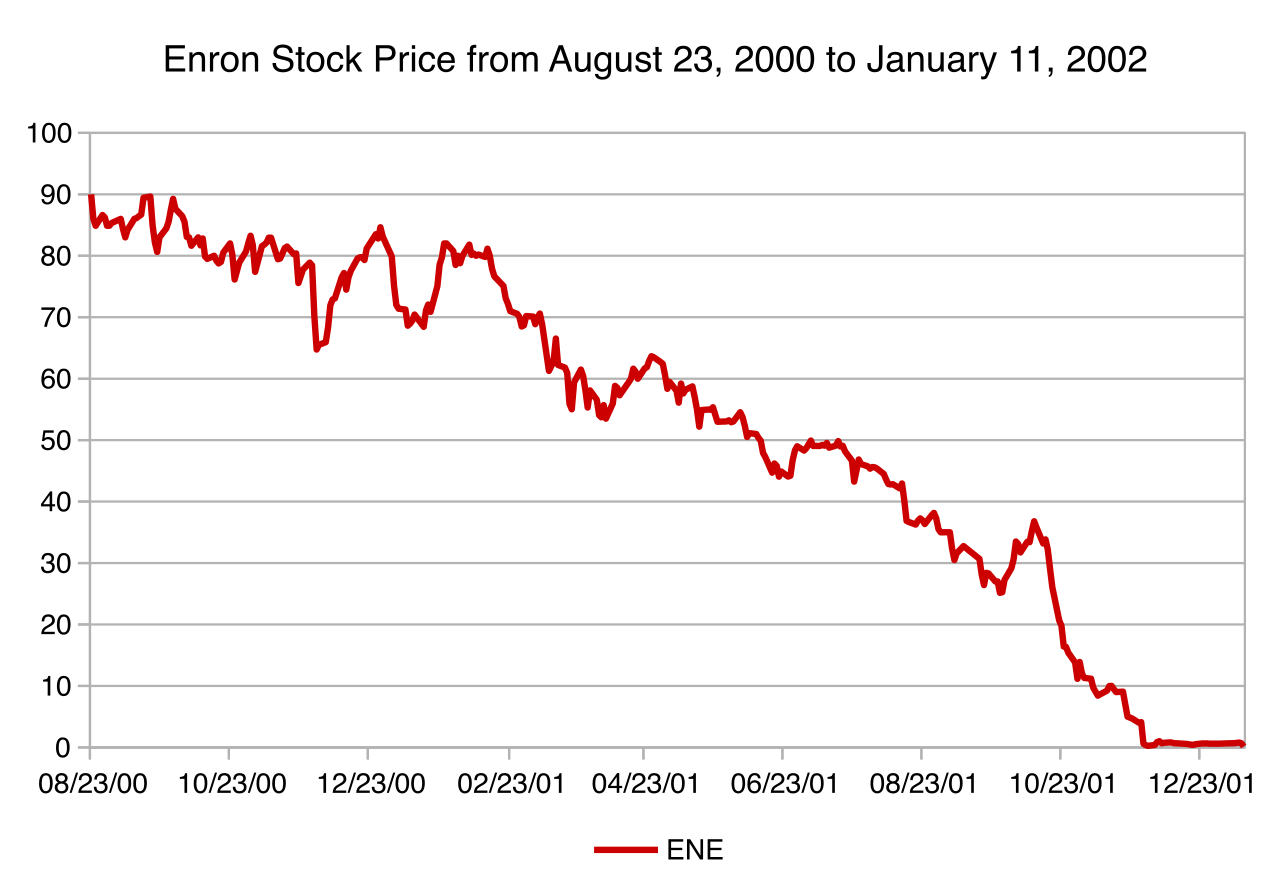

Before 2004, executives treated non-qualified plans like personal ATMs, frequently changing their deferral schedules and payout dates to game their tax liabilities. Following the Enron scandal, Congress dropped the hammer by enacting Section 409A.

Internal Revenue Code Section 409A governs the legal timing of deferral elections and distributions for non-qualified deferred compensation plans. It removed the flexibility that made these plans easily manipulated, replacing it with rigid, unyielding statutory mechanics.

Strict Timing of Deferrals and Distributions

Under the law, Section 409A requires an employee to make a binding deferral election in the taxable year immediately prior to the year the related services are performed. If an executive wants to defer a portion of their 2027 salary, the paperwork must be signed, sealed, and irrevocable by December 31, 2026.

Furthermore, they cannot simply withdraw the money when they feel like it. Section 409A permits non-qualified deferred compensation distributions only upon specific triggering events such as separation from service, disability, death, an unforeseeable emergency, or a previously specified fixed date.

To prevent the most powerful insiders from looting a sinking company just before bankruptcy (the Enron scenario), Congress added a specific speed bump: Key employees of publicly traded companies must wait six full months after separation from service before receiving non-qualified deferred compensation distributions under Section 409A rules.

The Catastrophic Penalty for Violation

Section 409A is entirely unforgiving. A violation of Section 409A rules results in the immediate taxation of all deferred compensation amounts for the affected employee.

But the IRS doesn't stop at ordinary income tax. To ensure compliance, an employee faces an additional 20 percent penalty tax on deferred amounts if the non-qualified deferred compensation plan violates Section 409A rules. For an executive in the highest tax bracket, a 409A violation can vaporize well over 50% of their deferred wealth overnight. As a planner, your ability to spot a broken 409A election is a massive value-add to high-net-worth clients.

Up to this point, we have focused primarily on traditional deferred compensation—where the executive chooses to defer a portion of their own salary or bonus. However, employers have other tools in the non-qualified toolkit designed to retain key talent.

Supplemental Executive Retirement Plans (SERPs)

Sometimes, an employer wants to build a golden handcuff entirely out of company money.

A Supplemental Executive Retirement Plan (SERP) is an employer-funded non-qualified deferred compensation plan designed to provide additional retirement benefits to key executives.

Unlike a traditional NQDC plan where the executive defers their own pay, a Supplemental Executive Retirement Plan (SERP) acts as a supplemental pension plan and does not require the executive to defer their own current salary. The company simply promises to pay the executive a set amount (often calculated as a percentage of final average pay, offset by the executive's qualified plan balances and Social Security) at retirement, provided they stay with the company.

Section 162 Executive Bonus Plans

What if an employer wants to reward an executive with a valuable asset today, utilizing life insurance, without the complexity of a Top-Hat plan or Section 409A restrictions? They turn to Section 162.

An executive bonus plan is frequently referred to as a Section 162 plan. The mechanics are straightforward, highly effective, and entirely grounded in current—not deferred—taxation.

Under a Section 162 executive bonus plan, the employer pays the premiums on a life insurance policy completely owned by the executive.

Because the executive owns the policy outright—with access to the cash value and the right to name the death benefit beneficiary—there is no substantial risk of forfeiture. The economic benefit is immediate. Therefore, the employer premium payments in a Section 162 executive bonus plan are reported as taxable income to the executive.

Since the employee recognizes the income immediately, our rule of corporate tax symmetry dictates the employer's treatment: the employer can immediately deduct the premium payments made under a Section 162 executive bonus plan as a reasonable business expense. To ease the tax burden on the executive, the employer will frequently provide a "double bonus," paying an additional cash amount to cover the income tax generated by the premium payments.

In mastering the non-qualified landscape for the CFP® exam, remember the fundamental tradeoff: extreme design flexibility requires extreme compliance. By moving outside ERISA, the executive gains unlimited deferral potential, but invites the punishing gravity of constructive receipt, the economic benefit doctrine, and Section 409A. Know the mechanics of how we shield executives from these forces, when those shields intentionally fail (like in a Secular trust or Section 162 plan), and the exact consequences of breaking the rules.