Property titling and beneficiary designations

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Imagine a brilliantly drafted will as a master set of blueprints for a building. The architect—your client—has mapped out exactly where every brick of their wealth should go. But if the land underneath that building is governed by an ironclad legal treaty that contradicts the blueprints, the treaty wins. Every single time. In financial planning, property titling and beneficiary designations are those treaties. They form the unseen machinery that automatically reroutes wealth long before a probate judge ever reads the first page of a last will and testament.

For the comprehensive financial planner, understanding how a client owns an asset is just as important as knowing what the asset is worth. Misunderstanding these mechanisms does not just lead to minor inconveniences; it results in disinherited children, catastrophic tax bills, and years of costly probate litigation.

To understand shared property, we must first define what it means to own something entirely. Fee simple absolute is the most complete form of individual property ownership. When a client holds property in fee simple, they are the undisputed monarch of that asset.

A fee simple owner has the absolute right to transfer the property during their lifetime (by selling or gifting it) and the absolute right to transfer the property at death through a will. Because this property is legally tethered to the individual owner and lacks any automated transfer mechanism, property owned in fee simple absolute passes through the probate process at the owner's death. The probate court is required to step in to legally retitle the asset according to the owner's will.

When two or more people own an asset, the rules of geometry change. The specific wording on the deed or account statement dictates who controls the asset during life, where it goes at death, and how the IRS treats it.

Tenancy in Common (TIC)

Tenancy in Common allows two or more individuals to own fractional interests in a single property. Think of this as owning shares in a corporation.

- Unequal Ownership: Tenancy in Common ownership interests do not have to be equal among the co-owners. You could have a situation where Sibling A owns 80% of a family cabin, while Siblings B and C each own 10%.

- Total Autonomy: Each Tenancy in Common owner can sell their specific fractional interest without the consent of the other owners.

- Estate Flow: Because the fractional interest belongs solely to the owner, each Tenancy in Common owner can bequeath their specific fractional interest to any chosen beneficiary through a will. Consequently, a Tenancy in Common property interest passes through probate upon the death of a co-owner.

- The Tax Reality: When one owner dies, only the deceased owner's fractional share of a Tenancy in Common property receives a step-up in basis at death.

Joint Tenancy with Right of Survivorship (JTWROS)

If TIC is like owning corporate shares, JTWROS is a biological organism—if one part dies, the surviving parts absorb it completely.

- Strict Equality: Unlike TIC, Joint Tenancy with Right of Survivorship (JTWROS) requires two or more individuals to share equal ownership interests in a property. You cannot have a 60/40 split in JTWROS.

- The Survivorship Engine: JTWROS property automatically transfers to the surviving joint tenant or tenants upon the death of one joint tenant. By virtue of this automatic transfer, JTWROS property bypasses the probate process.

- The Override: This is where estate plans fail: The survivorship feature of JTWROS supersedes any contrary distribution instructions in the deceased owner's will. If a client's will leaves "everything to my son," but their bank account is held in JTWROS with their sister, the sister gets the money.

- Severability: The survivorship feature is powerful, but fragile. A joint tenant in JTWROS can sever the joint tenancy during their lifetime by transferring their interest to a third party. Doing so breaks the legal unity. Severing a JTWROS creates a Tenancy in Common arrangement between the new owner and the remaining original owners.

- The Tax Reality: Just like TIC, only the deceased owner's fractional share of a JTWROS property receives a step-up in basis at death.

Comparative Summary for the Exam:

Feature Tenancy in Common (TIC) JTWROS Ownership Shares Can be unequal Must be equal Post-Death Transfer Governed by Will Automatic to Survivor Probate Process Yes No (Bypassed entirely) Step-Up in Basis Deceased's fraction only Deceased's fraction only

The law offers distinct forms of property ownership designed specifically to protect and define the economic partnership of marriage.

Tenancy by the Entirety (TBE)

Tenancy by the Entirety is a form of joint property ownership exclusively available to married couples. It functions similarly to JTWROS, but with added legal armor.

Because the law views the married couple as a single economic unit, Tenancy by the Entirety automatically includes a right of survivorship for the surviving spouse, meaning property held as Tenancy by the Entirety passes outside of probate directly to the surviving spouse.

What makes TBE unique is its rigidity and defensive capability:

- Mutual Consent: Neither spouse can unilaterally sever a Tenancy by the Entirety without the consent of the other spouse.

- The Creditor Shield: Because one spouse cannot force a division of the asset, Tenancy by the Entirety provides asset protection against the creditors of just one individual spouse. (If a doctor is sued for malpractice, but her home is owned TBE with her spouse who is not liable, the creditor generally cannot force the sale of the home).

Community Property

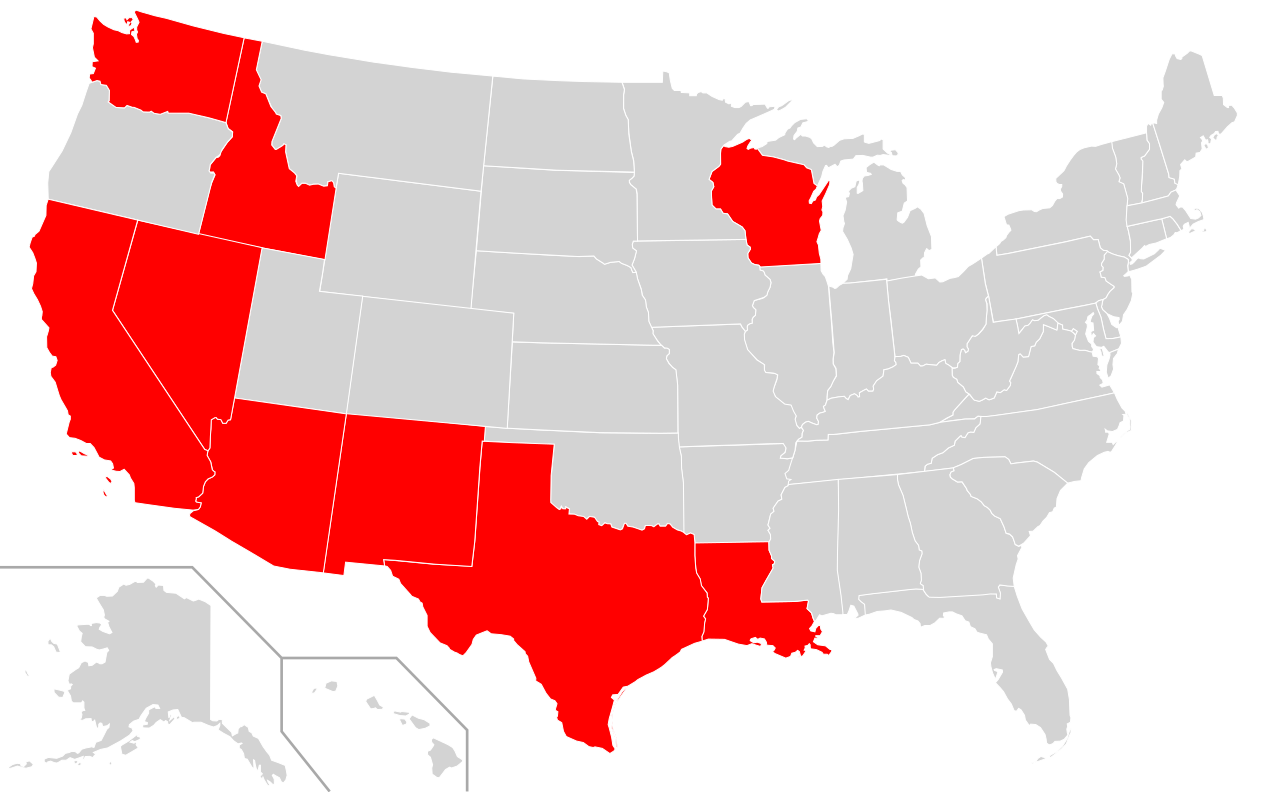

In the historical development of U.S. law, states influenced by Spanish and French civil law adopted a different framework. Community property is a distinct form of ownership for married couples in recognized community property states. For your exam, note that there are nine traditional community property states in the United States (e.g., California, Texas, Florida, etc.).

- The Default Rule: Assets acquired during marriage in a community property state are generally considered community property regardless of how the assets are titled. If a spouse earns a salary and deposits it into a bank account held solely in their own name, it is still 50% owned by the other spouse.

- The Exception: Property acquired by gift or inheritance during marriage in a community property state legally remains separate property.

- Estate Flow: Unlike TBE, community property does not inherently assume the surviving spouse gets everything. Spouses can leave their fifty percent share of community property to any chosen beneficiary through a will. Therefore, community property does not automatically include a right of survivorship unless specifically titled as community property with right of survivorship (CPWROS). Without that specific survivorship titling, a deceased spouse's half of standard community property is subject to the probate process.

- The Tax Holy Grail: This is one of the most powerful tax rules in financial planning: Both halves of a community property asset receive a full step-up in basis upon the death of the first spouse. If a couple bought a home for $100,000 and it is worth $1,100,000 when the first spouse dies, the surviving spouse gets a new basis of $1,100,000 on the entire property, allowing them to sell it entirely tax-free.

Property titling dictates real estate and physical assets. But what about modern wealth—the investments, retirement plans, and insurance policies that comprise the bulk of an average client's net worth?

These are governed by contracts. Beneficiary designations are contractual agreements dictating the distribution of an asset directly to a named party at the owner's death.

The fundamental rule of estate planning is this: Beneficiary designations legally supersede any conflicting distribution instructions written in the deceased owner's will. If a will says "all my wealth to my husband," but the client's ex-husband is still listed on the life insurance beneficiary form, the ex-husband receives the payout. The contract always wins.

Because the contract specifies exactly who the new owner is the moment the original owner's heart stops beating, assets with valid beneficiary designations entirely bypass the probate process.

Common assets utilizing beneficiary designations include life insurance policies, retirement accounts, and annuities.

Financial Account Contracts: POD and TOD

Outside of retirement accounts and insurance policies, clients can attach beneficiary designations to standard taxable accounts using specialized banking mechanisms.

- Payable on Death (POD) designations are used to name a designated beneficiary for bank accounts (checking, savings, CDs).

- Transfer on Death (TOD) designations are used to name a designated beneficiary for investment and brokerage accounts.

While the beneficiary is named on the document, the designated beneficiary of a POD or TOD account has no access to or control over the account during the original owner's lifetime. The original owner operates with absolute impunity—the owner of a POD or TOD account can change the beneficiary designation at any time prior to their death.

Contingencies and Complications

Best practice dictates building a backup plan. A contingent beneficiary receives the asset only if the primary beneficiary predeceases the account owner.

However, planners must vigilantly monitor who is being named:

- The Minor Trap: Clients intuitively want to name their children. However, naming a minor child directly as a beneficiary usually requires the local court to appoint a guardian to manage the inherited assets. This creates a costly, restrictive, and entirely avoidable administrative nightmare. (Trusts are typically the correct solution here).

- The Estate Trap: Sometimes clients, or lazy institutions, name the client's "Estate" as the beneficiary. This is a disaster. First, naming an individual's estate as the beneficiary of a retirement account formally subjects those assets to the probate process, stripping away the primary advantage of a contractual designation. Second, the tax consequences are punitive: Naming an individual's estate as the beneficiary of a tax-advantaged retirement account accelerates the required minimum distribution schedule for the heirs. Estates do not have a life expectancy; thus, the inherited funds must be drained—and taxed—far faster than if a human being had been named.

You will inevitably encounter situations where a client's desire to name a third-party beneficiary collides with their spouse's legal rights.

- The State Level (Community Property): If a client in Texas (a CP state) tries to leave their IRA entirely to their child from a prior marriage, they will encounter a mathematical hurdle. In community property states, a spouse holds a legal claim to a portion of a retirement account accumulated during marriage even if a third party is named as the beneficiary.

- The Federal Level (ERISA): Employer-sponsored retirement plans are governed by strict federal protections. The Employee Retirement Income Security Act (ERISA) requires a spouse to sign a written waiver to allow a non-spouse to be named as the primary beneficiary of a 401(k) plan. A client cannot simply log into their company's HR portal and leave their 401(k) to their sibling unless their spouse signs a legally notarized waiver consenting to the change.

Summary for the Practitioner

As a CFP® professional, your role requires you to audit the invisible architecture of your client's wealth. A flawlessly constructed will is functionally useless if an outdated TOD designation or an unintended JTWROS titling sends the assets in the opposite direction. By mastering the distinct rules of titling, basis step-ups, and contractual overrides, you transform estate planning from theoretical legal documents into guaranteed financial reality.