Tax reduction/management techniques

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Imagine wealth as a reservoir of water and the tax code as a system of spillways, dams, and valves. The goal of financial planning is not merely to accumulate water, but to control exactly how, when, and where it flows out. When a client generates income or realizes a gain, gravitational pressure forces that wealth toward the Internal Revenue Service. But as a planner, you possess three distinct mechanical levers to manage this pressure: conversion, shifting, and deferral. You can alter the chemical state of the water so it becomes immune to evaporation, pipe the water to a secondary reservoir where the structural pressure is lower, or build a dam to hold the water back for a future drought. Mastering these mechanisms transforms you from a mere allocator of assets into an architect of wealth retention.

In the physical world, water can freeze into ice or boil into steam. In the tax world, income exists in different states, and the IRS taxes these states at entirely different tax rates. Tax conversion strategies change the character of income from a higher-taxed category to a lower-taxed category. You are fundamentally changing what the income is in the eyes of the law.

The most common baseline state is ordinary income. For investors, net short-term capital gains are taxed at the taxpayer's ordinary income tax rates. If a client buys a stock and sells it at a profit ten months later, the IRS treats that profit exactly like a paycheck.

However, time acts as a transformative agent. Holding an appreciated capital asset for more than one year converts a potential short-term capital gain into a preferentially taxed long-term capital gain. Once that 366th day hits, the income changes state. Net long-term capital gains are taxed at preferential federal rates of 0%, 15%, or 20% depending on the taxpayer's taxable income. Simply waiting an extra few weeks to execute a trade can save a client thousands of dollars, fundamentally altering the math of their portfolio returns.

Conversion also applies to retirement accounts. A Roth IRA conversion changes tax-deferred retirement assets into tax-free retirement assets. You are converting future uncertainty into future certainty. However, the IRS demands a toll for this alchemy: a Roth IRA conversion requires the taxpayer to recognize the converted pre-tax amount as ordinary income in the year of the conversion. The planner's job is to calculate whether the client's current tax bracket is low enough to make paying this upfront toll mathematically superior to paying taxes on withdrawals decades later.

If tax conversion changes the nature of the water, tax shifting changes whose reservoir the water lands in. The U.S. tax system is progressive, meaning the fuller your reservoir, the higher the pressure (tax rate) on the next gallon of water. If a parent is in the highest tax bracket and a child is in the lowest, the overall family unit retains more wealth if the income flows to the child.

However, the IRS fiercely protects its revenue via the assignment of income doctrine, which prohibits taxpayers from transferring their tax liability on earned income to another person. You cannot work an extra shift at the hospital and ask the payroll department to send the check to your six-year-old to avoid taxes. In tax jurisprudence, this is famously known as the "fruit and the tree" metaphor. You cannot pick the fruit (income) and give it away while keeping the tree (the asset or labor that produced it).

Therefore, legitimate income shifting strategies require the legal transfer of the underlying income-producing asset to another individual. You must give away the tree.

Strategy 1: Gifting Appreciated Assets

Instead of selling highly appreciated stock, incurring a 20% capital gains tax, and giving the remaining cash to a 25-year-old child to buy their first home, gift the shares directly. Gifting highly appreciated capital assets to adult family members in the zero percent long-term capital gains bracket minimizes overall family tax liability. The adult child receives the stock, sells it, and because their taxable income is low, they pay 0% on the long-term gains. The family has entirely legally vanished the tax liability.

Strategy 2: Shifting Business Income

If a client owns a business, they can transfer portions of the "tree" to their children. Family Limited Partnerships (FLPs) allow parents to shift business income to children by gifting limited partnership interests. The parents retain the general partnership interest (controlling the business decisions), but a proportional share of the business's net income flows to the children's lower tax brackets.

Strategy 3: Employing the Child

What if we want to shift earned income without violating the assignment of income doctrine? We hire the child. Employing a child in a family business shifts ordinary business income from the parent's higher tax bracket to the child's lower tax bracket.

The IRS provides massive incentives for doing this correctly, provided the work is legitimate and the pay is reasonable. When structured properly:

- Wages paid to a child under age 18 by a parent's sole proprietorship are completely exempt from FICA payroll taxes (Social Security and Medicare).

- Wages paid to a child under age 21 by a parent's sole proprietorship are exempt from Federal Unemployment Tax Act (FUTA) taxes.

CFP Exam Warning: These payroll exemptions strictly require the business to be a sole proprietorship (or a partnership where both partners are the child's parents). If the parent's business is an S-Corporation or C-Corporation, the corporation is the employer, not the parent, and these FICA/FUTA exemptions evaporate.

Because shifting is so powerful, Congress built a massive roadblock to stop wealthy parents from hiding millions in stocks and bonds under their toddlers' names. This roadblock is the Kiddie Tax, and it dictates that a dependent child's excessive unearned income is taxed at the parent's highest marginal tax rate.

Notice the surgical precision of this rule: The Kiddie Tax strictly applies to unearned income such as dividends, interest, and capital gains. It targets passive investments. Conversely, the Kiddie Tax never applies to a dependent child's earned income from wages or self-employment. If a 16-year-old makes $50,000 acting in a television show or mowing lawns, it is taxed at the teenager's rates, never the parents'.

Who is caught in the Kiddie Tax net?

- The Kiddie Tax applies to children under age 19 at the end of the tax year.

- It also extends to older dependents: The Kiddie Tax applies to full-time students under age 24 at the end of the tax year whose earned income does not exceed half of their support.

The Mechanics of the Kiddie Tax

When a dependent child has unearned income, the IRS does not immediately apply the parent's rate. It processes the income through a tiered filtration system:

| Tax Tier | Treatment of Dependent's Unearned Income |

|---|---|

| Tier 1 | The first tier of a dependent child's unearned income is completely sheltered from taxation by the child's limited standard deduction. |

| Tier 2 | The second tier of a dependent child's unearned income is taxed at the child's own marginal tax rate. |

| Tier 3 (Excess) | Any unearned income beyond the first two tiers is subjected to the Kiddie Tax and taxed at the parent's highest marginal rate. |

This means a minor can still hold modest investment accounts (like a custodial UGMA/UTMA) without triggering punitive tax rates, but massive shifting of investment wealth is effectively neutralized.

If you cannot convert the tax rate, and you cannot shift the income to someone else, your next best weapon is time. Tax deferral strategies postpone the recognition of taxable income to future tax years.

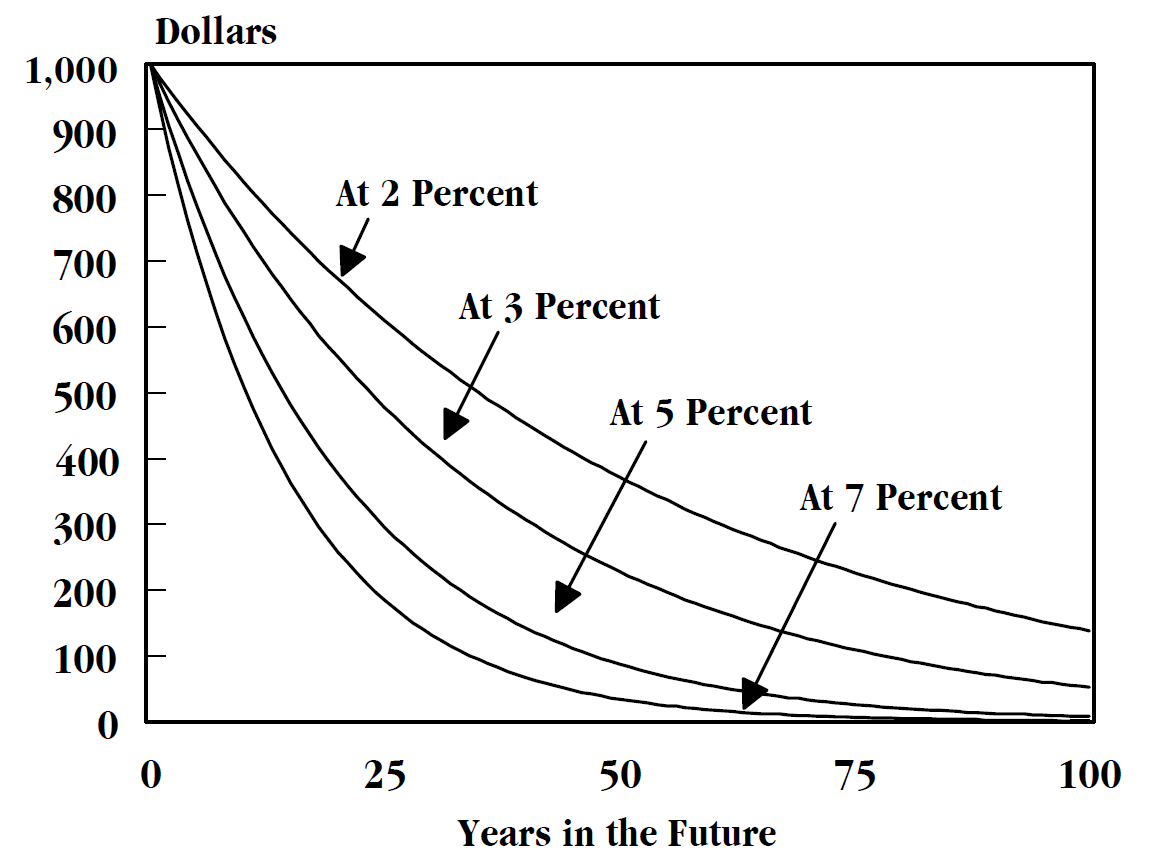

Why does this matter? The time value of money. If a client owes $100,000 in taxes today but legally defers that payment for ten years, they can keep that $100,000 invested. At a 7% return, that deferred tax payment will generate nearly $100,000 in new wealth for the client before the IRS ever collects the original principal.

- Real Estate (Section 1031): Section 1031 like-kind exchanges allow real estate investors to defer capital gains taxes by reinvesting sale proceeds into new investment properties. Instead of selling an apartment building, paying the tax, and using the remnants to buy a strip mall, the investor swaps the equity directly into the new property, deferring the tax indefinitely.

- Business/Asset Sales: Installment sales defer capital gains taxes by recognizing the gain proportionally as principal payments are received over multiple tax years. If a client sells a business for $5 million but takes payment over five years, they do not recognize all $5 million in year one. They spread the tax burden out, preventing a catastrophic push into the highest tax brackets in a single year.

Even the best investors pick losing assets. Tax-loss harvesting is the practice of selling investment assets at a loss to offset capital gains realized from other investments. You are deliberately realizing a loss on paper to act as a shield against gains elsewhere in the portfolio.

The Netting Rules (Order of Operations)

The IRS does not let you offset gains and losses randomly. You must follow strict algebraic steps. Capital losses must first be used to offset capital gains of the exact same character.

- Short-term capital losses must first offset short-term capital gains.

- Long-term capital losses must first offset long-term capital gains.

- A net capital loss remaining in one category can be used to offset a net capital gain in the opposite category.

If you have a net short-term loss of $10,000, and a net long-term gain of $4,000, they combine to leave you with a final net short-term loss of $6,000.

The Limit and the Carryforward

What happens if, after all netting is done, your client is still sitting on a massive net capital loss? The IRS provides a consolation prize:

- Individual taxpayers can use up to $3,000 of overall net capital losses to offset ordinary income in a single tax year.

- Married couples filing separately can use up to $1,500 of overall net capital losses to offset ordinary income per tax year.

If the client's losses vastly exceed this $3,000 limit, the losses do not vanish. Individual taxpayers can carry forward unused capital losses indefinitely into future tax years. A $33,000 net capital loss today will provide $3,000 of ordinary income offset every year for the next 11 years, or act as a massive shield the moment the client realizes a capital gain in the future.

You might think: "If my client owns a stock that is down $10,000, why don't I just sell it at 10:00 AM to trigger the tax loss, and buy it right back at 10:01 AM so we don't miss any market rebounds?"

The IRS anticipated this. It is a fake transaction, a round-trip to nowhere, designed solely to strip tax revenue. To stop it, Congress created the wash sale rule.

- The wash sale rule disallows a capital loss deduction if a substantially identical security is acquired within 30 days before the sale.

- The wash sale rule disallows a capital loss deduction if a substantially identical security is acquired within 30 days after the sale.

This creates a 61-day danger zone (30 days prior, the day of the sale, and 30 days after).

The Penalty for a Wash Sale

If a client triggers a wash sale, the loss is disallowed, but it is not destroyed. Think of the disallowed loss as a ghost; it detaches from the sold shares and haunts the newly purchased shares.

- A disallowed capital loss from a wash sale is added to the cost basis of the replacement security. By raising the basis of the new shares, the built-in loss is preserved for whenever the client finally sells the replacement shares for good.

- The holding period of a security sold in a wash sale is added to the holding period of the newly purchased replacement security.

By understanding these mechanics, you ensure your clients don't accidentally step on landmines while trying to harvest losses. You are the structural engineer of their tax profile. Every sale, every gift, every entity choice is a valve you are turning to keep their wealth safely within their own reservoir.