Business Taxation: Income Tax

A sole trader who sells hand-built furniture and a company that manufactures the same furniture down the street are taxed by two entirely different regimes, even though from the customer's point of view the businesses look identical. That divergence — not a quirk of drafting, but a structural feature of how UK tax law treats legal personality — is the first thing a solicitor advising a business client must get right, because it determines who signs the tax return, who bears the liability, and how the numbers are actually computed.

The trigger for Income Tax is trading profit, and the charge sits in the trading income provisions of the Income Tax (Trading and Other Income) Act 2005 (ITTOIA 2005). But who pays depends entirely on the legal form the business takes.

A sole trader has no legal existence separate from the individual who runs the business — there is no corporate veil to hide behind — so that individual is personally liable to Income Tax on the whole of the trading profit. A partnership is transparent in exactly the same way: the partnership itself is not a taxpayer for Income Tax purposes, so each partner is individually chargeable on their own share of the profit. A limited liability partnership (LLP) might sound corporate — it has separate legal personality for other purposes, such as contracts and litigation — but so long as it carries on a trade with a view to profit, it is tax-transparent, and its members are taxed exactly as if they were partners in an ordinary partnership. The one genuine outlier is the company: because a company has full separate legal personality, it is chargeable to Corporation Tax, not Income Tax, on its trading profits. Get the vehicle wrong in an exam scenario, and you have picked the wrong tax altogether.

Key distinction: Sole traders, partners, and LLP members pay Income Tax on trading profits. Companies pay Corporation Tax. The dividing line is separate legal personality, not the scale or sophistication of the business.

An individual becomes chargeable to Income Tax on trading profits from the date an activity first amounts to carrying on a trade — which raises an underrated but exam-favourite question: how do you know when a hobby has become a trade? HMRC and the courts do not apply a single test; they weigh the so-called badges of trade, a set of factors drawn from case law and HMRC guidance that together build up an overall impression. No single badge is decisive — you never win or lose on one factor alone — but the badges regularly tested include:

- A profit-seeking motive behind the activity.

- The frequency and number of similar transactions (one sale looks like a disposal; a dozen sales a year look like a business).

- The nature of the asset disposed of (an asset that produces income or personal enjoyment, like a painting kept on a wall, points away from trade; a stockpile of raw materials points toward it).

- Whether work was done to the asset to make it more marketable (buying a run-down car, repairing it, and reselling it looks far more like trading than a straight resale).

- The circumstances and reasons for the sale (an unexpected inheritance sold off is a world away from a deliberate acquisition-and-resale strategy).

Weigh these together, form an overall impression, and you have answered the "is this a trade" question the way HMRC and the tribunals actually answer it.

The UK Income Tax year runs from 6 April to 5 April the following year — a fact so basic it is easy to forget it drives everything else in the timing rules. Since the reform that took effect for 2024/25 onward, unincorporated businesses are taxed under the tax year basis: the taxable trading profit for a given tax year is the profit actually arising in that tax year, full stop, regardless of what accounting period the business happens to use. This replaced the old "current year basis," under which taxable profit tracked the accounting period ending within the tax year — a system that produced the notorious "overlap profits" problem when a business's accounting date didn't match 5 April.

Under the tax year basis, if a sole trader's accounts don't run to 5 April, taxable profit for a given tax year is simply apportioned on a time basis between the two accounting periods that straddle it. A trader with a 31 December year end, for instance, will apportion roughly nine months of one accounting period and three months of the next to arrive at the 2026/27 figure.

The transition to this system did not happen overnight. 2023/24 operated as a one-off transitional year, in which a sole trader's taxable profit was made up of two components: a standard part (profit of the normal accounting period ending in 2023/24) plus a transition part (profit arising from the end of that accounting period up to 5 April 2024). Before spreading the transition part, any brought-forward overlap relief — profit that had effectively been taxed twice under the old current year basis — is deducted from it first. Whatever transition profit survives that deduction is then spread evenly over five tax years (2023/24 through 2027/28), unless the taxpayer elects to accelerate and bring more of the charge forward sooner (useful, for example, if the taxpayer expects to be in a lower tax band in an earlier year).

Formula check: Transition part profit − brought-forward overlap relief = residual transition profit, spread over 5 tax years (unless accelerated by election).

Here is a trap that catches almost every student on first exposure: accounting profit is not taxable profit. The accounts prepared for a business's own management purposes follow accounting conventions; the tax computation follows tax rules. Bridging the two is the adjustment of profits computation, and it always starts from the same place — the net profit shown in the business accounts — before a series of statutory add-backs and deductions is applied.

The add-backs follow a clear underlying logic: strip out anything that either isn't a genuine cost of earning trading profit, or is capital rather than revenue in nature.

- Wholly and exclusively. Expenditure must be incurred wholly and exclusively for the purposes of the trade to be deductible. Anything with a dual (business and personal) purpose, or no trade purpose at all, must be added back.

- Capital expenditure. If capital expenditure has been recorded as an expense in the accounts, it must be added back — capital costs are not deductible as revenue expenses; relief for them, if any, comes separately through capital allowances.

- Depreciation. For the same reason, any depreciation charged in the accounts is added back. Depreciation is an accounting estimate of an asset's wear and tear, not a tax concept — the tax system replaces it entirely with capital allowances (see below).

- Client entertaining. Expenditure on entertaining clients is disallowed outright and added back, no matter how genuinely it was incurred for business development.

- Fines from unlawful conduct. Fines the business incurs as a result of its own unlawful conduct (a parking fine picked up making a delivery, a regulatory penalty) are disallowed and added back — the tax system will not subsidise the cost of breaking the law.

Once the adjustment is complete, capital allowances step in to give relief for capital expenditure on qualifying assets used in the trade — the tax-recognised substitute for the depreciation that was added back. The centrepiece is the Annual Investment Allowance (AIA): 100% relief in the year of purchase for qualifying plant and machinery expenditure, up to a limit of £1 million of qualifying expenditure per business per year. Spend beyond the AIA limit on qualifying plant and machinery, and the excess instead attracts a writing-down allowance (WDA) calculated on a reducing-balance basis — a smaller percentage of an ever-shrinking pool each year, rather than a single upfront deduction. Cars are the standing exception worth memorising: they never qualify for the AIA at all, only WDAs.

Exam shortcut: AIA = 100% now, up to £1m, for plant and machinery (not cars). Everything else falls back to WDA on a reducing balance.

Cash Basis vs Accruals Basis

Separately from the profit adjustment, there is a choice about when income and expenditure are recognised in the first place. Under the cash basis, a business recognises income when cash is actually received and expenditure when cash is actually paid — timing follows the bank account, not the underlying economic event. Under the accruals basis, income and expenditure are instead recognised in the accounting period to which they relate, regardless of when the cash physically moves. Since 2024/25, the cash basis has been the default method for preparing unincorporated business accounts for Income Tax purposes — a business must actively elect into the accruals basis if it wants to use it, a reversal of the historical assumption that accruals was the norm.

The Trading Allowance

For small-scale trading, the trading allowance offers a simpler alternative to tracking actual expenses: an individual can deduct up to £1,000 of trading income instead of deducting the real costs of the trade. Where gross trading income for the tax year doesn't exceed £1,000 at all, the allowance can wipe out the liability entirely — known as full relief — with no return entry needed for that income. One limit worth flagging for a multi-trade client: an individual gets only one trading allowance in total, even if they run more than one trade simultaneously.

Once trading profit has been adjusted and reliefs applied, it is added to the individual's other income sources to form total taxable income, against which the Personal Allowance and rate bands are applied.

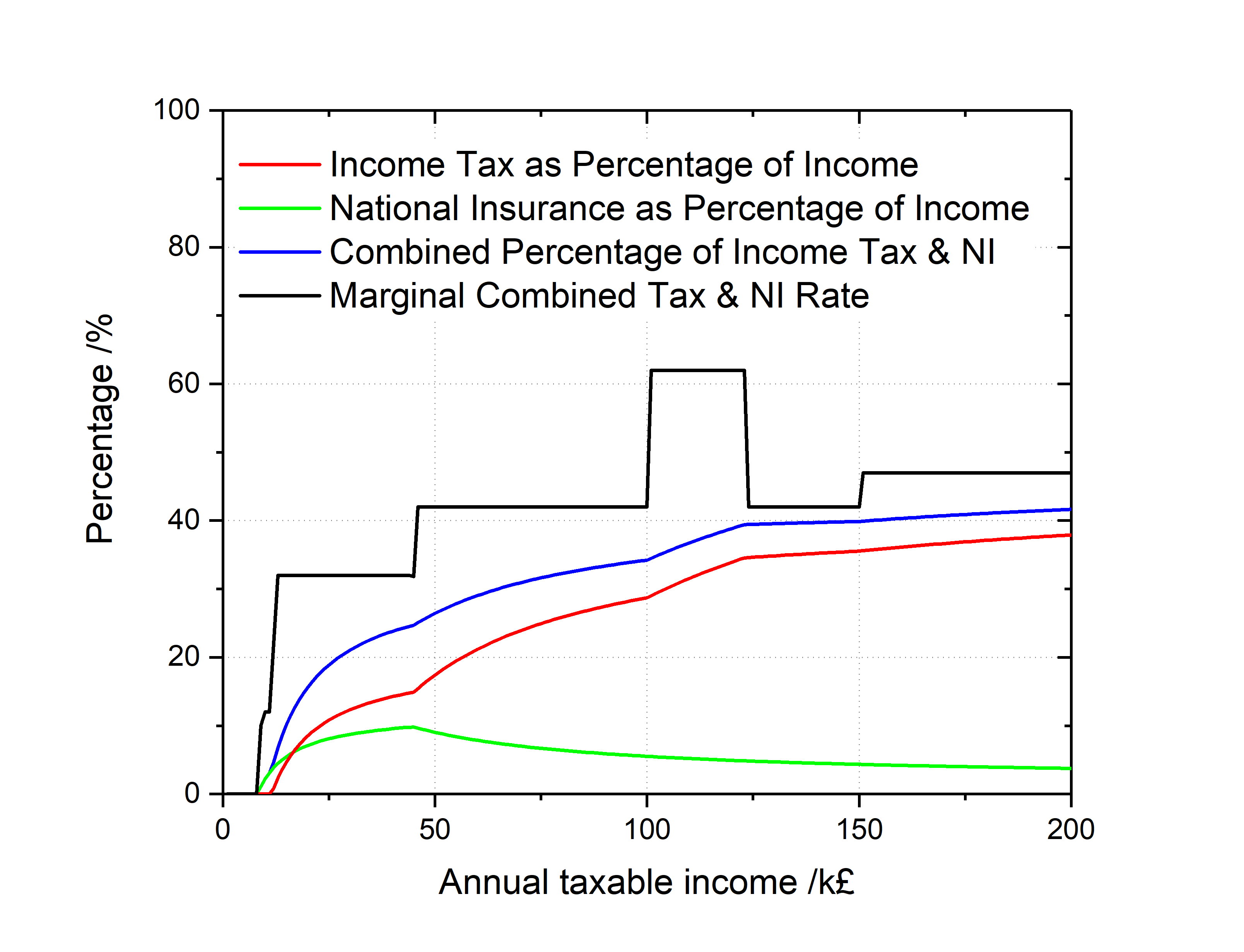

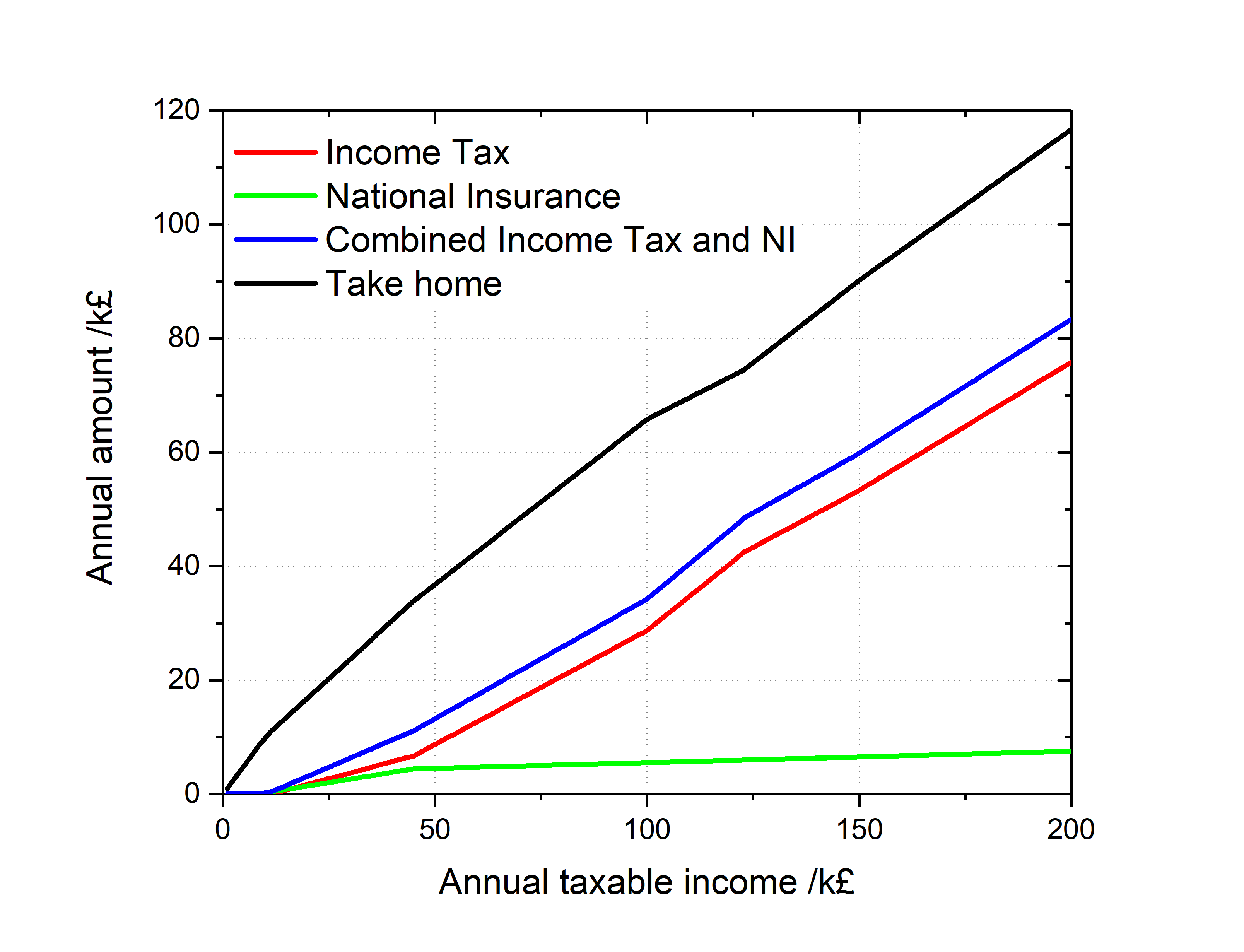

Every individual is entitled to a Personal Allowance — an amount deducted from total income before any Income Tax is charged on the remainder. For 2026/27, the Personal Allowance is £12,570. High earners lose it progressively: the allowance is reduced by £1 for every £2 that adjusted net income exceeds £100,000, tapering to nil once adjusted net income reaches £125,140. That taper effectively creates a stealth 60% marginal rate band between £100,000 and £125,140, worth flagging to a client who is deciding whether to draw more profit in a particular year.

The remaining income above the Personal Allowance is taxed through three bands for 2026/27:

| Band | 2026/27 income range | Rate |

|---|---|---|

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Above £125,140 | 45% |

Income Tax liability, in other words, is simply the Personal Allowance and these bands applied to the individual's total taxable income for the tax year — trading profits plus every other source of income (employment, property, savings, and so on) added together before the bands bite.

National Insurance: A Parallel, Separate Charge

National Insurance Contributions (NICs) are calculated and collected entirely separately from Income Tax, even though both run through the same Self Assessment machinery for the self-employed — a distinction examiners like to test because students conflate the two. The relevant charge on trading profits is Class 4 NICs, levied on profits between the lower profits limit and the upper profits limit. For 2026/27, Class 4 NICs are charged at 6% on trading profits between £12,570 and £50,270, and at 2% on profits above £50,270 — bands that track the Income Tax basic-rate threshold and higher-rate threshold almost exactly, which is not a coincidence but a deliberate alignment of the two systems.

Class 2 NICs work differently since reform: for 2026/27, the small profits threshold is £7,105. Above that threshold, a self-employed individual is simply treated as having paid Class 2 contributions — protecting their state pension record — without actually making a payment.

Partnership taxation layers a second step on top of everything above. Partnership trading profit is computed once, as if the partnership were a single continuing trader, applying all the same adjustment-of-profits rules already covered. Only after that single computation is complete is the profit allocated between the individual partners, according to whatever profit-sharing ratio (PSR) the partnership agreement specifies for the period in question. If the agreement is silent on shares, the default under the Partnership Act 1890 kicks in: partners share profits equally — a default that surprises clients who assumed unequal capital contributions would automatically translate into unequal profit shares.

Each partner is then taxed on their allocated share as if it were the profit of their own individual trade — with their own Personal Allowance, their own rate bands, their own Class 4 NICs. The partnership itself submits a partnership tax return showing the total trading profit and its allocation, but critically, the partnership is never itself assessed to Income Tax on that profit — the assessment lands entirely on the individual partners.

Trading losses are not simply absorbed and forgotten; the legislation gives a business several distinct ways to use a loss to reduce tax elsewhere, and choosing between them is a classic applied SQE1 scenario.

- Sideways loss relief lets a trading loss be set against the individual's general income — from any source — of the same tax year, the preceding tax year, or both.

- If a loss isn't otherwise relieved, it can simply be carried forward and set against future profits of the same trade.

- Early trade losses relief is aimed specifically at new businesses: a loss arising in the opening years of a new trade can be carried back and set against the individual's general income of the three tax years preceding the loss-making year — valuable for a start-up founder who was previously employed and paying tax at source.

- Terminal loss relief covers the opposite end of a business's life: on permanent cessation of a trade, a loss in the final 12 months of trading can be carried back against profits of the same trade in the three tax years preceding the final tax year.

The pattern worth internalising: sideways relief and early trade losses relief both reach into general income; carry-forward and terminal loss relief are both confined to profits of the same trade. Match the relief to the client's facts — new business versus established, ongoing versus ceasing — and the right answer usually falls out.

Becoming chargeable to Income Tax on trading income triggers an administrative obligation, not just a tax liability: the individual must notify HMRC by registering for Self Assessment, by 5 October following the end of the tax year in which the trade began. Miss that window, and penalties can follow even before a return is late.

The online Self Assessment return itself must be filed by 31 January following the end of the relevant tax year, and any balancing payment of tax due for that year is due on that same 31 January. HMRC issues an automatic fixed penalty for missing the filing deadline, regardless of whether any tax is actually owed.

For many self-employed taxpayers, 31 January is not the only payment date in the calendar. Where a taxpayer's Income Tax liability for the preceding tax year exceeded £1,000, and less than 80% of that liability was collected at source (as it typically is not, for the self-employed), the taxpayer is generally required to make payments on account (POA) toward the current year's liability. Each payment on account is normally set at half of the taxpayer's total Income Tax and Class 4 NIC liability for the preceding year, with the first instalment due on 31 January during the tax year itself and the second on 31 July following the end of that tax year. Once the year closes and the actual final liability is known, any shortfall between the two payments on account already made and the real liability is mopped up through a balancing payment, due — again — on 31 January following the end of that tax year.

Payment calendar for a typical self-employed client: 31 January (POA 1 for current year + balancing payment for prior year) → 31 July (POA 2 for current year) → 31 January the following year (balancing payment + next year's POA 1) — and the cycle repeats.

Seeing these dates as one continuous cycle, rather than a list of isolated deadlines, is what turns this topic from a memory exercise into something a trainee solicitor can actually advise a client on with confidence.