Intestacy and Property Outside the Estate

Picture an estate as a jug of water poured into channels cut by law. When a person dies leaving a valid will that empties the jug completely, the channels are irrelevant — the will decides where every drop goes. But the moment there is no will, or the will only empties part of the jug, section 46 of the Administration of Estates Act 1925 (AEA 1925) supplies the channels, and the water must flow down them mechanically, in a fixed statutory order, whatever the deceased would actually have wanted.

The section 46 rules apply whenever a person dies without a valid will disposing of the whole estate. That covers the obvious case — no will at all — but it also covers partial intestacy: a valid will exists, yet some asset or residue is left undisposed of (a lapsed gift, a failed residuary clause, an asset acquired after the will was made and not caught by its wording). Whatever residue escapes the will falls through to section 46 exactly as if there had been no will at all. The statutory order that follows is not a set of guidelines to be weighed against the facts — it is applied mechanically, regardless of estrangement, moral claims, or what everyone agrees the deceased "would have wanted."

The first question the statutory order asks is whether a spouse or civil partner survives, and if so, whether there is also surviving issue (children, grandchildren, and further descendants).

No surviving issue. A surviving spouse or civil partner takes the whole residuary estate absolutely. Nothing is shared with anyone further down the family tree.

Where there is surviving issue, the entitlement splits into three layers, and this is where the numbers matter for exam purposes:

| Layer | What the spouse/civil partner receives |

|---|---|

| 1 | The personal chattels, absolutely |

| 2 | A statutory legacy — a fixed net sum, currently £322,000 — plus interest |

| 3 | One half of anything left in the residue, absolutely |

The remaining half of the residue (after the statutory legacy) is held on the statutory trusts for the issue — not for the spouse.

The statutory legacy of £322,000 applies to deaths on or after 26 July 2023, set by the Administration of Estates Act 1925 (Fixed Net Sum) Order 2023. This figure is index-linked and periodically revised, so always check the sum in force at the date of death, not the exam-year figure by rote.

It is worth understanding why the spouse's share looks like this today, because it was not always so. Before 1 October 2014, the spouse or civil partner only had a life interest in half of what remained after the statutory legacy — the capital was locked up for the issue, and the spouse merely received the income from it during their lifetime. The Inheritance and Trustees' Powers Act 2014 abolished that life-interest trust and replaced it with an absolute half share, meaning the surviving spouse now owns their portion outright and can spend, invest, or give it away exactly as they please. That reform is a favourite exam trap: candidates sometimes describe a "life interest," which is now historically wrong for deaths after the 2014 changes.

One more numerical detail: the statutory legacy is not a static, interest-free sum sitting untouched until distribution. Interest accrues on it from the date of death, at the Bank of England base rate applicable at the end of that day, for deaths on or after 1 October 2014. A surviving spouse waiting through a slow administration is not penalised for the delay — the legacy grows to compensate.

The 28-day survivorship rule

Entitlement as a "surviving" spouse or civil partner is not automatic merely because they outlived the intestate by a matter of hours. Under section 46(2A) AEA 1925, inserted by the Law Reform (Succession) Act 1995, a spouse or civil partner is only treated as entitled if they survive the intestate by at least 28 days. This applies to deaths of the intestate occurring on or after 1 January 1996.

If the spouse or civil partner dies within 28 days of the intestate, the estate devolves as if that spouse or civil partner had predeceased the intestate — their entitlement simply evaporates, and the estate passes to the next class down the statutory order (or, if there is issue, straight to the issue under the statutory trusts).

This interacts subtly with an older rule you will also meet in this topic: the commorientes rule under section 184 of the Law of Property Act 1925. Where the order of two or more deaths is genuinely uncertain (a car crash, a house fire), section 184 deems the younger person to have survived the elder. For most purposes this presumption still operates — but for spousal intestate succession specifically, it is displaced by the 28-day rule in section 46(2A). A young spouse who cannot be shown to have survived by 28 clear days does not inherit under intestacy merely by being presumed the survivor under section 184; the specific statutory provision takes priority over the general presumption.

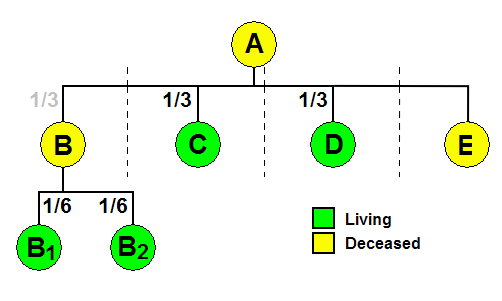

Where the intestate leaves issue but no surviving spouse or civil partner, there is no splitting of layers — the whole residuary estate is held on the statutory trusts for the issue, under section 47 AEA 1925.

The statutory trusts operate as follows:

- The estate is divided equally among the intestate's children who are living at the death.

- Each child's interest is contingent — it only vests once that child reaches 18, or marries, or forms a civil partnership under that age. A child who dies before satisfying the contingency takes nothing under that limb.

- If a child has predeceased the intestate but left their own issue, that child's share does not simply disappear or get redistributed among the surviving siblings — it passes per stirpes to that predeceased child's own children, in equal shares between them. Think of the estate as split into family "stirpes" (branches) rather than purely by headcount of living individuals.

- A child conceived before but born after the intestate's death (the "en ventre sa mère" principle) is treated as living at the date of death for these purposes — the law does not let the accident of timing of birth defeat an otherwise entitled child.

Who counts as a "child" for intestacy

Several statutory extensions widen — or narrow — who falls within "issue," and the exam frequently tests the edge cases:

- Under the Family Law Reform Act 1969, a child born outside marriage is treated identically to a child born within marriage.

- Under the Adoption and Children Act 2002, an adopted child is treated as the child of their adoptive parents only — the legal tie to the birth parents is severed for intestacy purposes, even though the biological relationship obviously still exists in fact.

- A stepchild who has not been legally adopted has no automatic entitlement as issue of the intestate under section 46, however close the relationship in life. Only a formal adoption (or, in narrower circumstances, a 1975 Act claim) can remedy this.

If there is no surviving spouse or civil partner and no issue, section 46 works down a fixed hierarchy of blood relatives. Learn this order as a ladder — you drop to the next rung only if the rung above is entirely empty:

- Parents — in equal shares if both survive, or to the sole surviving parent absolutely.

- Siblings of the whole blood (sharing both parents), on the statutory trusts.

- Siblings of the half blood (sharing one parent), on the statutory trusts.

- Grandparents, in equal shares.

- Uncles and aunts of the whole blood, on the statutory trusts.

- Uncles and aunts of the half blood, on the statutory trusts.

- Bona vacantia — if none of the above statutory classes survives, the estate passes to the Crown, the Duchy of Lancaster, or the Duke of Cornwall (depending on where in England the deceased was domiciled), as ownerless property.

Each rung uses the same statutory-trusts logic seen above where relevant: relatives share equally within their class, with per stirpes substitution for a predeceasing member's own issue.

The intestacy rules are famous for the categories of person they simply do not recognise, and exam scenarios love to plant one of these to test whether you spot the gap:

Cohabitants. A partner who is not married to, and not in a civil partnership with, the intestate has no automatic entitlement whatsoever under the intestacy rules — however long the relationship, however many years shared under one roof. Their only recourse is a claim under the Inheritance (Provision for Family and Dependants) Act 1975, and that is a discretionary claim for "reasonable financial provision," not an entitlement.

Divorced spouses. Once a decree absolute (or, under current terminology, a final order) has been made, a former spouse has no entitlement under intestacy — the marriage, for these purposes, is treated as if it never conferred rights.

Judicially separated spouses. Under section 18(2) of the Matrimonial Causes Act 1973, if a decree of judicial separation was in force and the separation continued until the death, the surviving spouse is treated as having predeceased the intestate. Note the distinction from divorce: judicial separation does not dissolve the marriage, but it does strip intestacy rights if it is still subsisting at death.

The statutory legacy layer above gives the spouse or civil partner the personal chattels absolutely, so the definition matters in practice, not just in theory. Section 55(1)(x) AEA 1925, as substituted by the Inheritance and Trustees' Powers Act 2014, defines personal chattels as tangible movable property other than money or securities for money.

Two carve-outs matter:

- Property used solely or mainly for business purposes at the death is excluded (so a sole trader's van or workshop tools do not pass as "chattels").

- Property held solely as an investment is excluded (a wine collection bought purely to appreciate in value, rather than to be drunk and enjoyed, would fall outside the definition).

Everything above assumes the asset actually forms part of the deceased's estate, waiting to be distributed by will or by section 46. But a significant amount of wealth in a typical client's life never reaches that stage — it passes automatically, by operation of some other legal mechanism, and neither the will nor the intestacy rules get a say. Advising an intestate estate without first checking for these assets is one of the most common and costly errors a trainee solicitor can make, because it changes both what the personal representatives actually administer and what creditors can reach.

A solicitor advising on any intestate (or partially intestate) estate must first establish what passes automatically outside the estate mechanism before applying the section 46 distribution rules to whatever remains.

Joint property and survivorship

Where two or more people hold property as beneficial joint tenants, on the death of one the property passes automatically to the survivor(s) by the right of survivorship — historically termed jus accrescendi. This operates outside the estate entirely and takes priority over anything the deceased's will (or the intestacy rules) might otherwise say. A joint tenant simply cannot leave "their share" of a jointly held house by will, because in equity there is no distinct share to leave — each joint tenant is treated as owning the whole, subject to the others' equal interest, until the last survivor takes it all.

This can be changed during the joint tenants' lifetimes by severance, which converts the beneficial joint tenancy into a tenancy in common. Once severed, each co-owner's distinct share does form part of their own estate on death and passes under their will or the intestacy rules like any other asset. The methods of severance are exam-critical:

- Written notice under section 36(2) of the Law of Property Act 1925 — a joint tenant may sever unilaterally simply by giving the other joint tenant(s) written notice of their desire to do so; no agreement from the others is needed.

- That notice must be served in accordance with section 196 of the Law of Property Act 1925 — valid methods include leaving it at the recipient's last known address, or sending it by registered post.

- Williams v Hensman recognises three further methods outside the statutory notice route: (1) one joint tenant acting on their own share (e.g. selling or mortgaging it), (2) mutual agreement between all the joint tenants, and (3) a course of dealing sufficient to show that the parties mutually treated their interests as a tenancy in common.

Severance requires an act inter vivos — while all parties are alive. A joint tenant cannot sever by a notice given, or purportedly given, after the death of the joint tenant who wished to sever. Once one joint tenant has died, survivorship has already operated and there is nothing left to sever.

By contrast, property held as tenants in common never carries survivorship: each tenant's distinct share forms part of their own estate on death and is dealt with under their will or the intestacy rules in the ordinary way.

Life policies written in trust

A life insurance policy written into trust pays its proceeds directly to the named beneficiaries, bypassing the deceased policyholder's estate entirely. Two routes achieve this, and the exam expects you to distinguish them:

- Under section 11 of the Married Women's Property Act 1882, a policy expressed to be for the benefit of a spouse, civil partner, or children creates a statutory trust in favour of those named beneficiaries. The proceeds do not form part of the insured's estate and are not available to the insured's creditors — a valuable protection, but a narrow one: a section 11 trust can only benefit the assured's spouse or civil partner and children, nobody else.

- An express trust over a life policy, by contrast, can name any beneficiary the policyholder chooses — a sibling, a friend, a charity — and is not restricted to the section 11 categories.

Either way, because the policy proceeds sit in trust from the outset, they were never the policyholder's own property to leave by will, and they are simply irrelevant to the section 46 exercise.

Pension death benefits

Registered pension scheme death benefits typically operate on a similar logic but through discretion rather than trust terms. Payment is usually decided by the scheme trustees or administrator, not fixed by the member's will. A member completes an expression of wishes (or nomination) form indicating who they would like to receive the benefits — but critically, that expression is not legally binding on the trustees, even though in practice trustees will normally take it into account when exercising their discretion.

Because the decision rests with the trustees rather than being fixed by the member, the benefit passes outside the deceased member's estate and is administered neither under the will nor under the intestacy rules.

Inheritance tax position, and a change on the horizon. Discretionary pension death benefits currently fall outside the deceased member's estate for inheritance tax purposes. That is changing: under the Finance Act 2026, most unused pension funds and pension death benefits are due to be brought within the deceased member's estate for inheritance tax purposes, for deaths occurring on or after 6 April 2027. Watch the date carefully in a problem question — a death before 6 April 2027 is assessed on the current outside-the-estate basis; a death on or after that date falls under the new regime. Death-in-service benefits are expected to remain outside the estate for inheritance tax purposes even after the 2026 changes take effect, so do not assume the reform sweeps in every pension-linked payment.

A related planning device worth knowing: a spousal bypass trust is a discretionary trust nominated to receive a member's pension death benefits, structured so that the funds avoid being swept into the surviving spouse's own estate later — protecting the money from a second round of inheritance tax (or means-testing) on the spouse's subsequent death.

Why "outside the estate" matters beyond distribution

The common thread across joint property, trust-based life policies, and discretionary pension death benefits is not merely that they bypass the will or intestacy rules — it is that they are not available to satisfy debts owed by the deceased's estate to ordinary creditors. An estate that looks hopelessly insolvent on paper may still leave the family financially secure, because the house passed by survivorship, the life policy paid the named beneficiaries directly, and the pension scheme exercised its discretion in the family's favour — none of it ever touching the pool of assets creditors can claim against.

This is precisely why the professional instinct matters more than the mechanical rule-following: before you can correctly apply section 46, or advise a client on what an intestate estate is actually worth, you must map what has already left the estate by another route. Get that mapping wrong, and every subsequent calculation — the statutory legacy, the half-share of residue, the statutory trusts for the issue — is built on the wrong base figure entirely.