WA Trust & Earnest-Money Accounts, Handling of Monies & Recordkeeping

At the heart of every real estate transaction lies a profound vulnerability: the moment a buyer or tenant hands over their money before they actually own the property or possess the lease. If a real estate brokerage goes bankrupt, what happens to that money? If it is sitting in the firm’s standard operating account, it becomes an asset of the firm, vulnerable to the firm's creditors. The buyer loses everything. To prevent this, the law requires a structural firewall. We call this firewall a trust account.

A trust account is a legal quarantine zone. The money inside it does not belong to the broker; it belongs to the public. As an aspiring Washington real estate broker, your ability to strictly adhere to the mechanics of this quarantine—how funds enter, how they are held, and how they exit—is the absolute foundation of your fiduciary duty.

Let us examine the precise architecture the Washington Department of Licensing (DOL) requires for handling other people’s money and the meticulous records you must keep to prove you have done so correctly.

Every drop of client money that flows through a brokerage must be completely isolated from the firm’s own money. To achieve this, Washington dictates exactly where and how a trust account is constructed.

The designated broker bears ultimate responsibility for the administration of all client trust funds and all brokerage trust bank accounts. They are the chief architect and the final guarantor of the firewall.

To ensure the funds are protected against institutional failure and accessible to Washington regulators, the trust account must meet strict criteria:

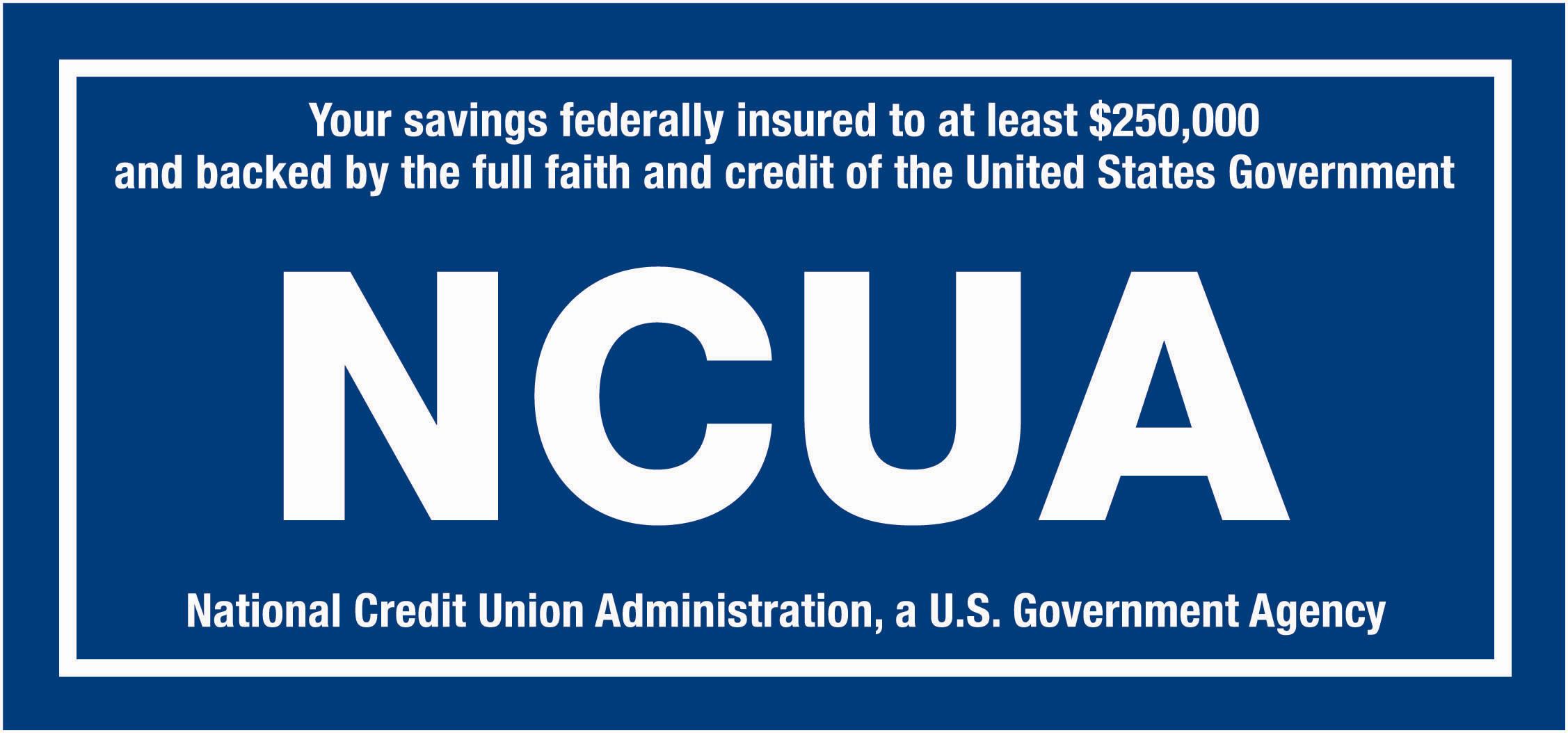

- Federal Protection: Washington trust funds must be held in an institution insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA).

- State Jurisdiction: The accounts must be maintained in a financial institution capable of accepting legal service in Washington state.

Furthermore, the bank must be told exactly what kind of account this is, and the public must be able to see it. Real estate trust bank accounts must be explicitly identified as trust accounts.

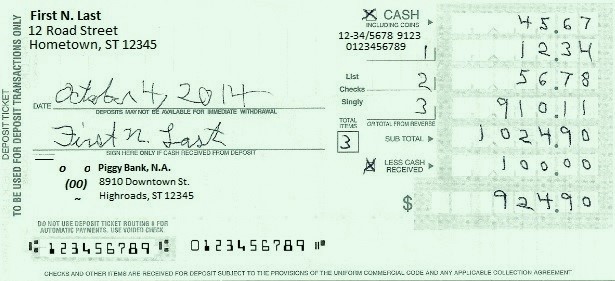

Crucial Identification Rule: The account cannot just say "Trust." Real estate trust bank accounts must include the exact licensed name of the real estate firm. This exact licensed name must also appear printed on all trust bank account deposit slips and all trust bank account checks.

When you, as a broker, are handed a check by a client, a biological clock starts ticking. The Washington administrative code has engineered these timelines to ensure money does not languish in the glovebox of your car.

The Broker's 2-Day Rule

Real estate brokers must deliver client funds to the designated broker (or to a delegated managing broker) within two business days of receipt. Similarly, real estate brokers must deliver transaction documents to the designated broker or a delegated managing broker within two business days of mutual acceptance.

The Firm's 1-Day Rule

Once the firm has the money, the quarantine must be established immediately. Trust funds must be deposited into the firm trust bank account no later than the first banking day following receipt.

Earnest Money Mechanics

Who is the check made out to? By default, earnest money checks must be made payable to the licensed real estate firm.

However, transactions are flexible if the parties agree. An earnest money deposit may be paid directly to an escrow agent or directly to the seller, but only if mutually agreed upon in writing by the parties. If the funds are directed to an alternative payee, the designated broker must retain a copy of that written agreement.

What if a buyer writes a check but asks you not to cash it yet? A check serving as earnest money may be held uncashed only under two strict conditions:

- The earnest money agreement explicitly requires holding the check for a specified time.

- The earnest money agreement explicitly requires holding the check until a specific event occurs.

When money sits in a bank, it generates interest. Who gets that interest? Washington has a specific mathematical rule designed to fund public goods using the temporary float of real estate transactions.

Earnest money deposits of $10,000 or less must be placed in a pooled interest-bearing trust account.

Because this is a pooled account containing funds from many different buyers, the interest is not sliced up and handed back to the individuals. Instead, the state harvests it:

- Seventy-five percent (75%) of the interest from a Washington pooled real estate trust account is remitted to the Washington state housing trust fund.

- Twenty-five percent (25%) of the interest is remitted to the Washington real estate education program account.

If a trust account is a quarantine zone, breaching the firewall is the most severe violation a broker can commit. This takes two forms.

1. Commingling (Cross-Contamination)

Commingling occurs when a real estate licensee mixes client funds with personal funds, or when they mix client funds with brokerage firm funds. If you accidentally deposit a client's earnest money into your business operating account, you have commingled.

The Single Exception to Commingling: Banks often require a minimum balance to open an account or charge fees if the balance drops too low. To facilitate the mechanics of banking without using client money, a designated broker is permitted to deposit a minimal amount of firm funds into a trust account to open the account or to prevent the account from being closed.

2. Conversion (Theft)

While commingling is mixing the funds, conversion is using them. Conversion occurs when a real estate licensee uses client trust funds for personal purposes, or when they use client trust funds for business purposes.

The Prohibition on Improper Disbursements

To prevent accidental conversion, Washington places strict boundaries on how money can exit a trust account.

- No disbursements from a Washington real estate trust account may be made to pay commissions owed to real estate licensees.

- No disbursements may be made to pay brokerage business expenses.

- No disbursements may be made to pay bank charges.

When it comes to earnest money, the release of funds is dictated strictly by contract. Disbursements of earnest money from a trust account must conform to the specific terms of the earnest money agreement. What if a deal falls apart and the buyer and seller agree to split the earnest money 50/50, which isn't in the original contract? Disbursements of earnest money outside the terms of the earnest money agreement require a written release from all parties.

Property management handles high volumes of recurring trust funds (rents, security deposits). Because of this operational difference, Washington law carves out specific rules for property managers.

- Clearing Accounts: A property manager processing hundreds of rent checks often uses a central account to process them before routing. A common clearing account used for property management transactions must be established as a formal trust account.

- Accounting Systems: The bookkeeping must be immaculate. Property management accounting systems must track all cash received and all cash disbursed through the trust accounts of the firm.

- Interest Exemptions: Property management trust accounts are exempt from the requirement to remit interest to the Washington state housing trust fund. Furthermore, a designated broker is not required to establish individual interest-bearing accounts for each property owner, provided that all owners assign the interest to the firm.

In physics, you cannot prove a phenomenon occurred unless you record the data. In real estate, you cannot prove you upheld your fiduciary duty unless you have the paper trail.

Washington real estate records must be retained for a minimum of three years.

A common trap for novice brokers is assuming you only keep records for deals that successfully close. This is false. The three-year record retention requirement applies to:

- Closed real estate transactions.

- Failed real estate transactions.

- Real estate offers that never reached mutual acceptance. (Even if a buyer wrote an offer and the seller rejected it outright, you keep that paperwork for three years).

The Anatomy of the Transaction Folder

At the firm level, the designated broker must have an overarching view of the business. A Washington real estate firm must maintain an accurate up-to-date log of all brokerage service agreements submitted by affiliated licensees.

For individual deals, a Washington real estate transaction folder must contain:

- All written agreements related to the transaction.

- All receipts related to the transaction.

- All closing statements related to the transaction.

- All material correspondence related to the transaction.

Storage: Electronic vs. Physical

Can you store these files digitally? Yes, electronic storage of Washington real estate records is permitted if document retrieval is immediate. However, you cannot just say "they are in the cloud." Electronically stored real estate records must be viewable and printable at the licensed office of the real estate firm.

If you maintain physical boxes of paper, your office will quickly run out of space. Washington provides a relief valve: Physical transaction records closed for at least one year may be moved to a single remote storage facility within Washington state.

If you use remote storage, you must maintain a list of all transactions stored at a remote facility at the licensed office of the real estate firm, and those remote records must be available upon demand of the Washington Department of Licensing.

Why go through all this trouble? Because you are subject to the oversight of the state.

The Director of the Washington Department of Licensing has the authority to inspect the records of a real estate firm. More importantly, regarding the financial quarantine zone we have discussed, the Director has the authority to audit a real estate trust account at any time.

They do not need a subpoena. They do not need to wait for a consumer complaint. The privilege of holding a real estate broker's license in Washington comes with the mandatory condition of total, continuous transparency to the state. Master these mechanics, respect the firewall, keep your records for three years, and you will navigate the legal plumbing of real estate seamlessly.