Debt Securities: Characteristics and Yields

Capital, like water, must flow where it is needed, but it demands a price for the journey. When an entity—be it a massive corporation, a local municipality, or a sovereign nation—needs capital, it generally has two choices: it can sell a piece of itself by issuing equity, or it can rent the capital by issuing debt. As a registered representative, your daily reality involves managing this rented capital. Your clients will constantly weigh the allure of higher yields against the relentless forces of time, inflation, and the ever-present risk that the borrower might simply fail to pay them back. To serve these clients effectively, you must understand not just the mechanics of debt securities, but the fundamental physics of how interest rates, time, and creditworthiness interact to dictate a bond's price and its yield.

When a corporation needs to make payroll on Friday but won't receive its receivables until next month, it doesn't issue a thirty-year bond. It turns to the money market. Money market instruments are debt securities with original maturities of one year or less. Because of this extremely short time horizon, money market instruments provide high liquidity and low principal risk. They are the financial system's parking lot for cash.

There are several distinct vehicles in this parking lot, each serving a specific mechanical function in the economy:

- Commercial Paper: This is essentially a corporate IOU. Commercial paper is a short-term, unsecured promissory note issued by corporations. To entice buyers, commercial paper is typically issued at a discount to par value and matures at par (the difference is the investor's return). Crucially, the maximum maturity for commercial paper to avoid SEC registration is 270 days. If a corporation issues debt for 271 days, the SEC considers it a longer-term security requiring a full, expensive registration process.

- Banker's Acceptances (BAs): Imagine a US importer buying goods from a manufacturer in Japan. The Japanese manufacturer wants a guarantee of payment before shipping. They use a Banker's Acceptance, which are short-term time drafts used primarily to finance international trade. Like commercial paper, the maximum maturity for a banker's acceptance is typically 270 days.

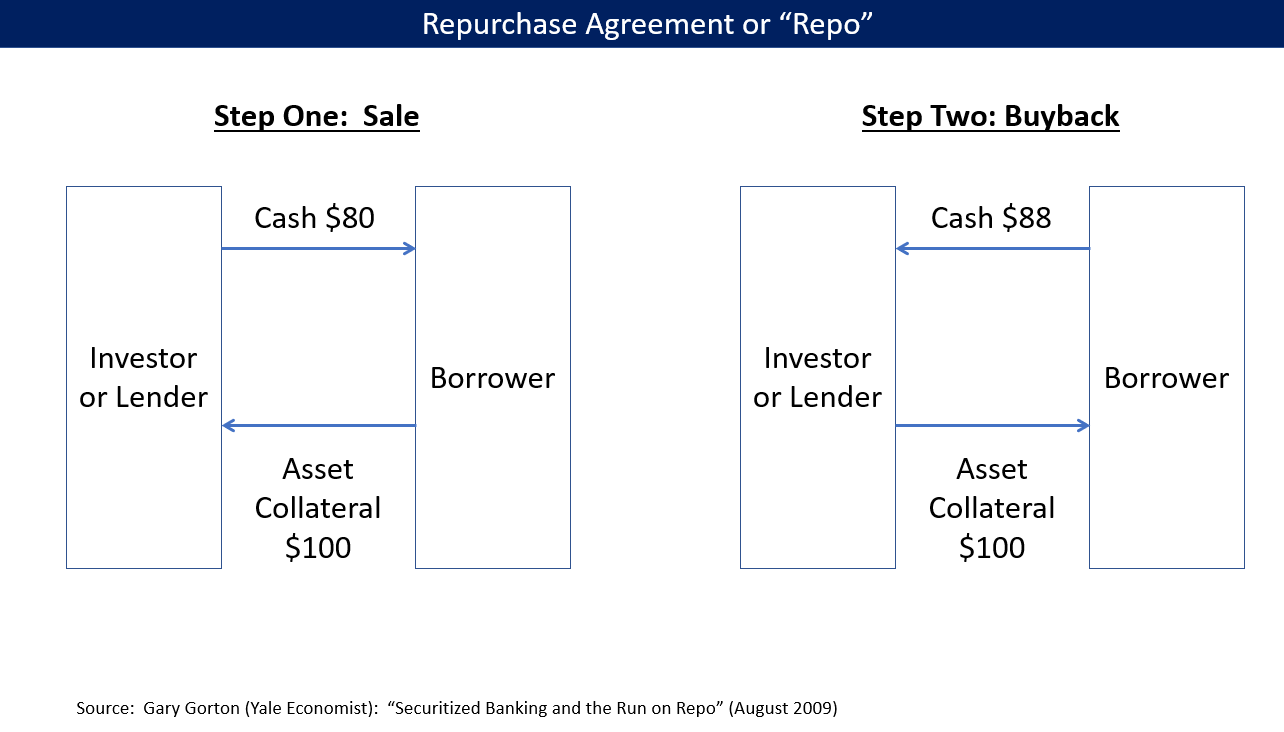

- Repurchase Agreements (Repos): Repos involve the sale of securities with a simultaneous commitment to buy the securities back at a higher price. It is effectively a short-term, collateralized loan used heavily by institutional players to manage overnight cash.

- Federal Funds: The Federal Reserve requires banks to hold a certain amount of cash in reserve. Federal funds are excess reserves that commercial banks deposit at regional Federal Reserve banks. When a bank falls short of its requirement at the end of the day, it borrows from a bank that has a surplus. Therefore, Federal funds are typically lent from one member bank to another on an overnight basis to meet reserve requirements.

Brokered Certificates of Deposit (CDs)

You will frequently encounter clients who want the safety of a bank CD but the convenience of keeping it in their brokerage account. Brokered certificates of deposit are interest-bearing deposits issued by banks and sold through broker-dealers.

However, you must explain a critical distinction to your clients. Unlike a traditional bank CD where you might just pay an early withdrawal penalty to the bank, brokered certificates of deposit can be traded in the secondary market prior to maturity. If interest rates have risen since the CD was issued, the value of that CD on the secondary market will fall. Thus, brokered certificates of deposit sold before maturity in the secondary market can experience a loss of principal due to interest rate fluctuations. Furthermore, clients must understand that brokered certificates of deposit provide FDIC insurance coverage up to standard limits only if the issuing bank is an FDIC member. The broker-dealer itself does not confer FDIC insurance.

When a client buys a bond, they are buying a stream of future cash flows. How we measure the return on that investment depends entirely on the price paid and how long the bond is held.

Let us isolate the four distinct ways we measure yield:

- Nominal Yield (Coupon): The nominal yield of a bond is the fixed annual interest rate printed on the bond certificate. It never changes. The nominal yield is calculated by dividing the annual interest payment by the par value of the bond. (e.g., A bond paying $50 a year on a $1,000 par value has a 5% nominal yield).

- Current Yield: This tells you what the bond is paying right now based on its market price. The current yield of a bond is calculated by dividing the annual interest payment by the current market price of the bond.

- Yield to Maturity (YTM): Yield to maturity calculates the annualized return of a bond assuming the bond is held until the maturity date. This is the most comprehensive measure because yield to maturity accounts for the difference between the purchase price and the par value received at maturity.

- Yield to Call (YTC): If a bond is callable, the issuer has the right to pay it off early (usually when interest rates drop). Yield to call calculates the annualized return of a bond assuming the bond is called by the issuer at the earliest possible call date.

The Yield Teeter-Totter

Interest rates and bond prices have an inverse relationship. If prevailing rates rise, the price of existing bonds must fall to make their fixed coupons competitive. When a bond's price moves away from par, its yields fan out mathematically.

The Physics of a Discount Bond If a client buys a bond for $900 (a discount), they get the annual coupon plus a $100 capital gain at maturity. Because of this baked-in gain, a bond trading at a discount has a yield to maturity greater than its current yield, and a current yield greater than its nominal yield. Because the call date arrives sooner than maturity, condensing the timeframe to earn that $100 gain, a bond trading at a discount has a yield to call greater than its yield to maturity. Discount Order: YTC > YTM > CY > NY

The Physics of a Premium Bond If a client buys a bond for $1,100 (a premium), they get the coupon, but they will lose $100 when the bond matures at $1,000. This baked-in loss drags down their total return. Therefore, a bond trading at a premium has a nominal yield greater than its current yield, and a current yield greater than its yield to maturity. If called early, that $100 loss is realized even faster. Thus, a bond trading at a premium has a yield to maturity greater than its yield to call. Premium Order: NY > CY > YTM > YTC

If a bond is trading exactly at par value, the teeter-totter is perfectly balanced. A bond trading at par value has a nominal yield, current yield, yield to maturity, and yield to call that are all equal.

Measuring Movement: Basis Points and Duration

When discussing yield changes with portfolio managers, you won't say "yields went up by zero point zero five percent." You will use basis points. Basis points measure changes in bond yields. Mathematically, one basis point is equal to one-hundredth of a percentage point or 0.01 percent. Therefore, a change from 5.00% to 5.05% is an increase of 5 basis points.

To measure how violently a bond's price will react to these yield changes, we use Duration. Duration measures a bond's price sensitivity to changes in interest rates. A bond with a high duration (typically a long-term bond with a low coupon) will see its price swing wildly when interest rates move, while a low-duration bond will remain relatively stable.

You cannot accurately price a bond without knowing the probability of getting your money back. Bond ratings assess the credit risk and default probability of a debt issuer. Two major agencies—Standard & Poor's (S&P) and Moody's—dominate this space.

The cutoff between "investment grade" (safe enough for most institutional and fiduciary portfolios) and "speculative grade" is the most important line in the fixed-income market.

| Rating Agency | Investment Grade | Speculative Grade (High-Yield / Junk) |

|---|---|---|

| Standard & Poor's | AAA down to BBB | Starts at BB and goes lower |

| Moody's | Aaa down to Baa | Starts at Ba and goes lower |

Be aware of the terminology: speculative-grade bonds are commonly referred to as high-yield bonds or junk bonds. They must offer a higher yield to compensate the investor for the elevated risk of default.

Sometimes, traditional bonds don't meet a client's specific market view. In these cases, Wall Street creates structured products. Structured products often combine a traditional debt instrument with a derivative component. This allows an investor to wager on the movement of other asset classes while technically holding a debt instrument.

- Equity-Linked Notes (ELNs): These are debt instruments where the final payout is based on the return of an underlying equity (like a specific stock or basket of stocks).

- Exchange-Traded Notes (ETNs): These frequently test candidates on the Series 7. Exchange-Traded Notes are unsecured debt securities issued by a financial institution. The return of an Exchange-Traded Note is linked to the performance of a specific market index.

You must heavily caution clients regarding ETNs. Unlike traditional bonds, Exchange-Traded Notes do not pay periodic interest. Unlike principal-protected structured notes, Exchange-Traded Notes do not offer principal protection. Most dangerously, because they are unsecured promises to pay, investors in Exchange-Traded Notes are subject to the credit risk of the issuing financial institution. If the underlying index performs brilliantly, but the bank that issued the ETN goes bankrupt (as happened to Lehman Brothers ETN holders in 2008), your client may lose everything.

Capital does not stop at national borders, but regulations and currency risks do. When governments borrow, they issue sovereign debt, which is a debt security issued by a national government (like U.S. Treasuries or UK Gilts). If a U.S. client buys a British Gilt paying out in Pounds Sterling, they face a unique hazard: sovereign debt issued in a foreign currency exposes a United States investor to exchange rate risk. Even if the bond yields 6%, if the Pound collapses against the Dollar, the U.S. investor loses purchasing power.

To circumvent currency risk, issuers utilize the international bond market, categorized by where the bond is issued and the currency in which it is denominated:

- Eurobonds: These are debt instruments issued and sold outside the country of the currency in which the bonds are denominated. (e.g., A bond denominated in Japanese Yen but sold in Switzerland).

- Eurodollar Bonds: This is a specific type of Eurobond. Eurodollar bonds are US dollar-denominated bonds issued by an overseas entity and sold outside the United States. Because they are sold entirely outside U.S. borders, Eurodollar bonds are not subject to registration with the Securities and Exchange Commission.

- Yankee Bonds: Conversely, foreign entities often want to tap directly into the deep pockets of U.S. investors. Yankee bonds are US dollar-denominated bonds issued by foreign entities and sold within the United States. Because they are being marketed and sold to investors on U.S. soil, Yankee bonds must be registered with the Securities and Exchange Commission.

Understanding these boundaries is paramount. The SEC's jurisdiction follows the investor's location, not just the currency. By mastering these dynamics—from the overnight fed funds rate to the registration requirements of foreign debt—you bridge the gap between theoretical finance and the tangible wealth preservation of your clients.