Options: Profit, Loss, and Taxes

An options contract is fundamentally a machine designed to transfer kinetic financial energy—risk—from one party to another. When a client buys an option, they are purchasing the right to bend time and price in their favor, creating asymmetrical payoffs where the risk is strictly defined but the upside can stretch into infinity. When they sell an option, they act as an insurance company, collecting a premium up front in exchange for taking on the mathematical burden of another investor’s uncertainty. To operate successfully as a registered representative, you cannot merely memorize formulas. You must understand the internal architecture of these contracts. You must see exactly where the money flows when the underlying stock moves, how time and volatility alter the pricing physics, and precisely how the Internal Revenue Service will demand its share when the dust settles.

Before we calculate where an investor makes or loses money, we must understand what they are actually buying. An option's premium is not an arbitrary number; it is composed of two distinct physical properties: intrinsic value and time value.

Intrinsic Value is the undeniable, current mathematical reality of the option.

- The intrinsic value of a call option equals the current underlying stock price minus the option strike price.

- The intrinsic value of a put option equals the option strike price minus the current underlying stock price.

If a contract is "out-of-the-money," its premium consists entirely of time value. By definition, the intrinsic value of any option contract can never fall below zero.

Time Value is the speculative hope built into the price. It equals the total option premium minus the option's intrinsic value.

Time value is a decaying asset. As an option contract approaches the expiration date, time decay accelerates. The closer you get to the deadline, the faster the hope evaporates.

Beyond time, implied volatility acts as the pressure gauge of the market. Because higher volatility means a higher probability of the stock making a wild swing into the money, an increase in implied volatility generally increases the premium of both call options and put options. Conversely, a decrease in implied volatility generally decreases the premium of both calls and puts.

Finally, do not ignore macroeconomic gravity: interest rates. The cost of capital matters. Rising interest rates typically increase call option premiums and decrease put option premiums. Why? Because buying a call is a leveraged substitute for buying stock; higher interest rates make tying up capital in actual stock more expensive, driving up the demand—and price—for calls.

Every complex strategy in the derivatives market is built from four basic atomic structures. Let’s look at the pure economics of single-leg positions.

The Long and Short Call

When an investor buys a call, they are paying for the right to buy the stock.

- The break-even point for a long call option equals the strike price plus the premium paid.

- The maximum loss for a long call option equals the total premium paid. If the stock tanks, they simply walk away.

- The maximum profit for a long call option is theoretically unlimited. There is no ceiling on a stock price.

When a client writes (sells) a call, they are taking the opposite side of that trade. If assigned, the assignment of a short call requires the option writer to sell the underlying stock at the option strike price.

- The break-even point for a short call option equals the strike price plus the premium received.

- The maximum profit for a short call option equals the total premium received. That is their absolute ceiling.

- The maximum loss for a short call option is theoretically unlimited. If the stock rockets to the moon, the naked call writer is dragged along behind it, bleeding cash the entire way.

The Long and Short Put

When an investor buys a put, they are paying for downside insurance.

- The break-even point for a long put option equals the strike price minus the premium paid.

- The maximum loss for a long put option equals the total premium paid.

- The maximum profit for a long put option equals the strike price minus the premium paid. (A stock can only fall to zero, capping the absolute profit).

When a client sells a put, they are acting as a floor underneath the market. If the floor collapses, the assignment of a short put requires the option writer to purchase the underlying stock at the option strike price.

- The break-even point for a short put option equals the strike price minus the premium received.

- The maximum profit for a short put option equals the total premium received.

- The maximum loss for a short put option equals the strike price minus the premium received. (If the company goes bankrupt, they must still buy worthless stock at the strike price).

Seldom do investors trade options in a vacuum. Usually, they are attempting to manipulate the risk profile of stock they already own.

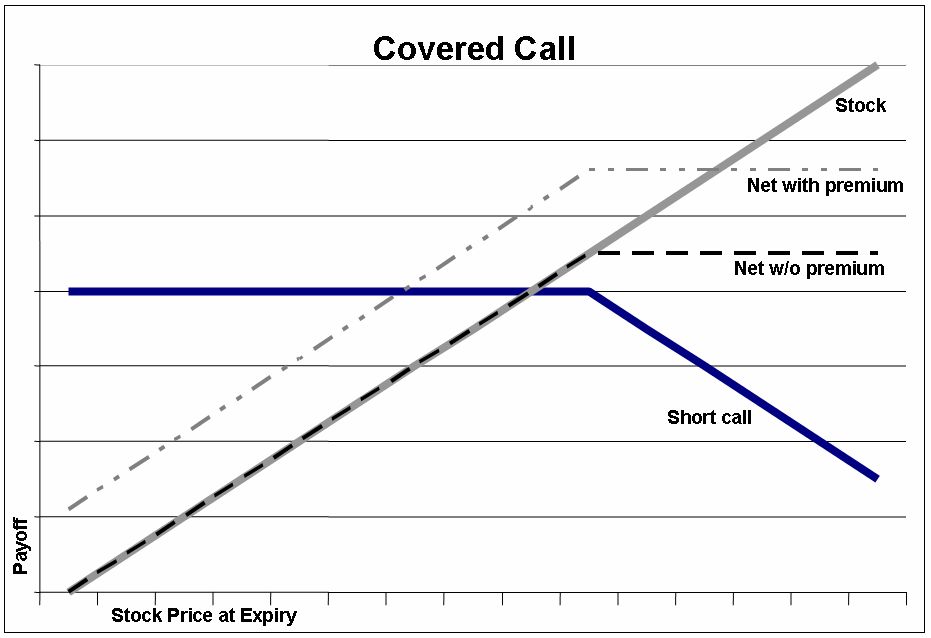

The Covered Call

Selling a call against a long stock position generates income but caps upside. You are selling away your lottery ticket.

- Break-even: Equals the underlying stock purchase price minus the call premium received.

- Maximum profit: Equals the call strike price minus the underlying stock purchase price plus the call premium received.

- Maximum loss: Equals the underlying stock purchase price minus the call premium received. (If the stock goes to zero, the premium only softens the blow).

The Protective Put

Buying a put on existing stock acts as an insurance policy. You pay a premium to lock in a floor.

- Break-even: Equals the underlying stock purchase price plus the put premium paid.

- Maximum loss: Equals the underlying stock purchase price minus the put strike price plus the put premium paid.

The Collar

When a client wants downside protection but doesn't want to pay out of pocket for the put, we construct a collar. A collar is an options strategy involving the purchase of a protective put and the sale of a covered call on an existing long stock position. The premium received from the short call funds the long put.

- Break-even: Equals the underlying stock price plus the net premium paid or minus the net premium received.

- Maximum profit: Is limited to the strike price of the short call minus the underlying stock purchase price plus or minus the net option premium.

- Maximum loss: Is limited to the underlying stock purchase price minus the strike price of the long put plus or minus the net option premium.

The Danger of the Ratio Write

What happens if greed takes over? Suppose a client owns 100 shares but sells two calls against it to double their premium. This is a ratio write. A ratio write involves selling more call options than the number of underlying shares owned by the investor. Because one of those calls is completely naked, a ratio write exposes the investor to unlimited maximum loss.

Spreads involve buying and selling options of the same class on the same underlying asset. By simultaneously buying and selling, you cap both your risk and your reward. Whenever you close one side of these trades early, be aware: closing an individual leg of an option spread triggers an immediate capital gain or loss for that specific leg.

Vertical Spreads (Debit and Credit)

A vertical spread uses different strike prices with the same expiration.

- The break-even point for any call spread equals the lower strike price plus the net option premium. (Memorize "Call Add Lower" or CAL).

- The break-even point for any put spread equals the higher strike price minus the net option premium. (Memorize "Put Subtract Higher" or PSH).

Debit Spreads (You pay to enter):

- Maximum loss: Equals the net premium paid.

- Maximum profit: Equals the difference between the strike prices minus the net premium paid.

Credit Spreads (You receive cash to enter):

- Maximum profit: Equals the net premium received.

- Maximum loss: Equals the difference between the strike prices minus the net premium received.

Calendar and Diagonal Spreads

- A calendar spread involves buying and selling options of the same class and strike price with different expiration dates. You are trading the difference in time decay. The maximum loss for a debit calendar spread is limited to the net premium paid.

- A diagonal spread involves buying and selling options of the same class with different strike prices and different expiration dates. It operates on both a vertical and horizontal axis.

Complex Geometries: Butterflies and Iron Condors

- A long call butterfly spread involves buying one lower strike call, selling two middle strike calls, and buying one higher strike call. You are betting the stock pins exactly at the middle strike. The maximum risk for a long butterfly spread is limited to the initial net premium paid.

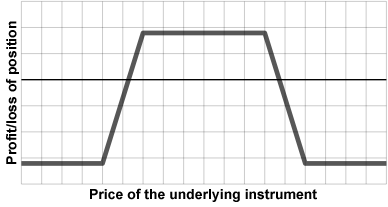

- An iron condor is a four-legged option strategy consisting of a bear call spread and a bull put spread. You are building a cage around the stock price, betting it won't move much. The maximum profit for an iron condor equals the total net premium received from the sold spreads.

Sometimes a client doesn't care which direction a stock moves, only that it moves violently.

The Straddle: A straddle involves purchasing or selling both a call and a put with the identical strike price and the identical expiration date.

- Upside break-even: Equals the strike price plus the total option premium.

- Downside break-even: Equals the strike price minus the total option premium.

- Maximum loss for a long straddle: Equals the total combined premium paid for the call and the put. (This happens if the stock flatlines at the strike).

- Maximum profit for a short straddle: Equals the total combined premium received for the call and the put.

The Strangle: A strangle involves buying or selling a call and a put on the same underlying asset with different strike prices and the identical expiration date. It is cheaper to buy than a straddle, but requires a wider stock movement to become profitable.

- Upside break-even: Equals the call strike price plus the total premium paid or received.

- Downside break-even: Equals the put strike price minus the total premium paid or received.

The market enforces strict boundaries to prevent manipulation and account for corporate alterations to the underlying stock.

Position and Exercise Limits

- Position limits restrict the maximum number of option contracts an investor can hold on the same side of the market for a specific underlying security. (Bulls: Long Calls + Short Puts. Bears: Long Puts + Short Calls).

- Exercise limits restrict the maximum number of option contracts an investor can exercise on the same side of the market within a five-business-day period.

Stock Splits and Dividends

When a company changes its capital structure, the Options Clearing Corporation (OCC) must alter existing contracts to ensure no one is unfairly enriched or harmed.

- Dividends: Standard equity option contracts are not adjusted for regular cash dividends. However, the Options Clearing Corporation adjusts standard equity option strike prices for special cash dividends.

- Even Splits (e.g., 2:1, 3:1): An even stock split increases the total number of option contracts held by the investor. It proportionally reduces the strike price of the affected option contracts. Most importantly, following an even stock split, each adjusted option contract continues to represent one hundred shares of the underlying stock.

- Odd Splits (e.g., 3:2, 5:4): An odd stock split does not change the total number of option contracts held by the investor. Instead, it increases the number of shares represented by a single existing option contract, while it proportionally reduces the strike price of the affected option contract.

- Reverse Splits (e.g., 1:10): A reverse stock split reduces the number of shares represented by a single existing option contract, and proportionally increases the strike price of the affected option contract.

Not all options are tied to shares of a corporation. Some derive their value from entirely different asset classes.

Index Options

These trade on the macroeconomic performance of the market. Crucially, you cannot deliver an entire index. Therefore, index options settle in cash instead of requiring the delivery of the underlying index securities.

- The standard multiplier for broad-based index options is one hundred dollars.

- The cash settlement amount of an index option equals the difference between the strike price and the index closing value multiplied by the index multiplier.

Yield-Based Options

These allow investors to speculate on the movement of interest rates (yields), not bond prices.

- Yield-based options are European-style contracts that settle in cash on the expiration date.

- The cash settlement value of a yield-based option is determined by the difference between the strike price and the underlying yield multiplier.

Foreign Currency (FX) Options

These allow hedging against global exchange rate fluctuations.

- Foreign currency options are European-style contracts that settle in United States dollars.

- The strike price of a foreign currency option represents the exchange rate in United States currency per unit of the foreign currency.

Taxes are where the brilliant options trader is separated from the bankrupt one. The IRS views derivative profits with intense scrutiny, applying completely different rules depending on exactly how you close the trade and what underlying asset you traded.

The Basic Expiration and Liquidation Rules

- The expiration of a standard equity option contract creates a short-term capital gain or loss for the investor.

- Likewise, closing a standard equity option position in the secondary market generates a short-term capital gain or loss.

- Do not try to game the clock on the short side: The short sale of any option always generates a short-term capital gain or loss upon expiration or closing.

- However, if you buy long-term time value: Closing a long Long-term Equity Anticipation Securities (LEAPS) option held for more than twelve months generates a long-term capital gain or loss.

The Exercise Rules (Cost Basis Adjustments)

If an option is exercised, the premium becomes part of the underlying stock's tax geometry. There is no immediate capital gain or loss on the option itself; the math transfers to the stock.

- The exercise of a call option adds the call premium to the buyer's cost basis of the newly acquired stock.

- The exercise of a call option adds the call premium to the seller's sales proceeds for the underlying stock.

- The exercise of a put option reduces the buyer's sales proceeds for the underlying stock by the put premium amount.

- The exercise of a put option reduces the seller's cost basis of the newly acquired stock by the put premium amount.

Holding Periods and Anti-Gaming Rules

The IRS hates when investors use options to artificially stretch short-term gains into lower-taxed long-term gains.

- Buying a put option on a stock held for less than one year resets the holding period of the underlying stock to zero. The clock stops instantly. Furthermore, the holding period of an underlying stock reset by a put purchase begins anew only after the purchased put option is disposed of or expires.

- The Exception: The Married Put. A married put occurs when an investor purchases a stock and a put option on that identical stock on the exact same day. Because they were bought together as a single packaged risk, purchasing a married put does not reset the holding period of the underlying stock. If the stock rises and the protection is unneeded, if a married put expires worthless, the entire put premium is added to the cost basis of the underlying stock.

- Covered Calls: Selling an out-of-the-money covered call does not affect the holding period of the underlying stock. But if you sell a call so deep in the money that it practically guarantees exercise, the IRS views that as a constructive sale. Thus, selling a deep in-the-money covered call suspends the holding period of the underlying stock.

- The Wash Sale Rule: You cannot sell a stock at a loss for a tax deduction and immediately buy it back synthetically. The wash sale rule triggers if an investor sells a stock at a loss and purchases a call option on that identical stock within thirty days. It also triggers if an investor sells a stock at a loss and sells a deep in-the-money put option on that identical stock within thirty days (because selling a deep ITM put heavily obligates you to buy the stock back).

Section 1256 Contracts: The Macro Rule

The IRS treats broad macroeconomic derivatives differently than single-stock picking. Broad-based index options, exchange-traded foreign currency options, and yield-based options are classified as Section 1256 contracts by the Internal Revenue Service.

What does this mean for the taxpayer? A massive advantage, paired with strict annual accounting.

- The Section 1256 tax rule designates sixty percent of the total gain or loss as a long-term capital gain or loss, and forty percent of the total gain or loss as a short-term capital gain or loss.

- Crucially, the sixty/forty tax treatment applies to Section 1256 option contracts regardless of the actual holding period of the position. Even if you held the position for 45 minutes, 60% of your profit is taxed at the favorable long-term rate.

- The catch: Section 1256 option contracts are marked-to-market at the end of every calendar year. The mark-to-market accounting rule treats unrealized gains and losses on Section 1256 contracts as closed positions on the last trading day of the year. You owe taxes on your paper profits on December 31st.

- Caveat: Narrow-based index options do not qualify as Section 1256 contracts. Because they behave like industry sectors rather than the whole economy, narrow-based index options are taxed under the same rules as standard equity options.

Netting It All Out

When the trading year ends and the math is tallied, what happens if an options trader simply loses money? The standard capital loss rules apply. Net capital losses generated from option transactions can offset up to $3,000 of ordinary income per year. If their losses exceed this limit, unused net capital losses from option transactions can be carried forward into subsequent tax years indefinitely.

In the world of options, the math is absolute, the risk is architectural, and the taxes are inevitable. Master the mechanics of these rules, and you will not only pass your exam—you will be an invaluable fiduciary to your clients in the field.