Options: Basic and Advanced Strategies

When a client holds a traditional equity position, they are exposed to blunt, absolute directional risk. The options market exists not merely as an avenue for speculation, but as a sophisticated financial laboratory where a practitioner can surgically dissect, transfer, and price this risk. For a General Securities Representative, mastering basic and advanced option strategies means acquiring the tools to reshape a client's financial reality. You are no longer just buying and selling; you are manipulating time, volatility, and probability to build mathematical floors under a lifetime of accumulated wealth, or to turn a stagnant portfolio into a dynamic, income-generating engine.

To pass the FINRA Series 7 exam and to serve your clients effectively, you must understand the architecture of these strategies. We will begin with foundational hedging and yield generation, step into the perilous realm of uncovered writing, construct precision boundaries using spreads, and finally, capture pure volatility through straddles and combinations.

Before we construct complex mechanisms, we must understand the primary building blocks used by institutional and retail investors to manage existing stock positions.

The Covered Call Strategy

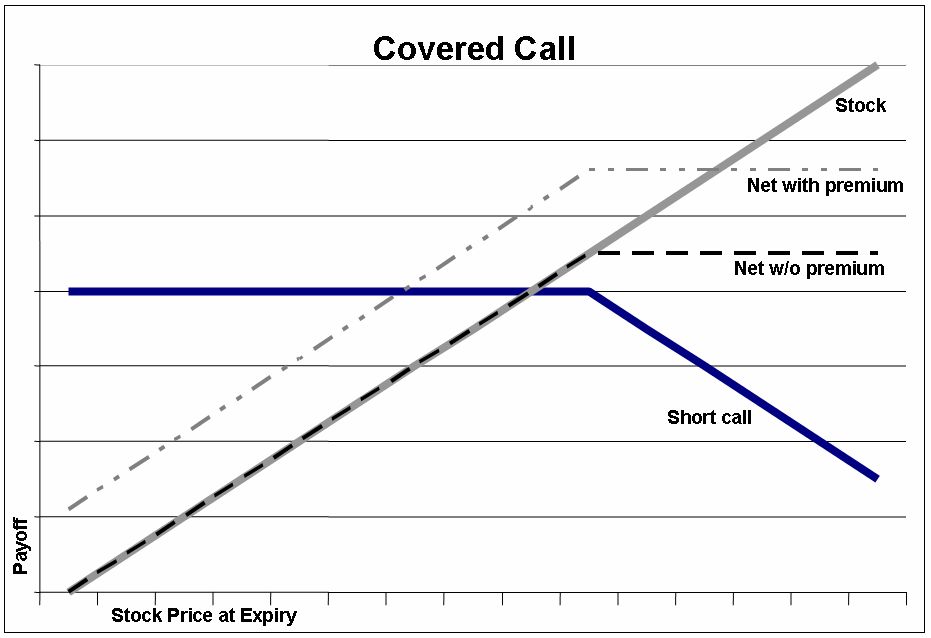

The most common strategy you will deploy for a client seeking yield is the covered call. A covered call strategy involves holding a long position in a stock and writing a call option on that exact same stock.

Why do this? The primary objective of writing a covered call is to generate additional income from the option premium. Imagine a client who owns 100 shares of a blue-chip stock that has been trading sideways for months. By selling a call option, they act as the "house," collecting a premium from a speculator. Consequently, a covered call writer exhibits a neutral to slightly bullish market sentiment; they are happy to hold the stock, but they do not expect it to skyrocket.

Because the investor owns the underlying asset, they are "covered" if the option is exercised and they are forced to deliver the shares.

- Protection: Writing a covered call provides limited downside protection on the stock position equal to the premium received. If the stock drops, the premium softens the blow.

- Maximum Gain: The maximum gain for a covered call equals the strike price minus the stock purchase price plus the premium received. You capture the stock's appreciation up to the strike price, plus the cash you were paid.

- Maximum Loss: The maximum loss for a covered call equals the stock purchase price minus the premium received. If the company goes bankrupt and the stock goes to zero, you lose your investment, but you keep the premium.

- Breakeven Point: The breakeven point for a covered call equals the stock purchase price minus the premium received.

The Protective Put Strategy

If the covered call is a strategy for yield, the protective put is a strategy for insurance. A protective put strategy involves buying a stock and buying a put option on that exact same stock. Investors use a protective put to limit downside risk on an existing stock position.

Imagine an executive who has accumulated massive wealth in their company's stock but fears an upcoming earnings report. By purchasing a put, they establish a guaranteed floor. If the stock collapses, they have the right to sell it at the strike price.

- Upside: The beauty of this insurance is that a protective put strategy maintains theoretically unlimited upside profit potential for the investor. If the stock soars, the put expires worthless, but the stock's gains run free.

- Maximum Loss: The maximum loss for a protective put equals the stock purchase price minus the put strike price plus the premium paid.

- Maximum Gain: The maximum gain for a protective put is theoretically unlimited.

- Breakeven Point: Insurance isn't free. The breakeven point for a protective put equals the stock purchase price plus the premium paid. The stock must appreciate enough to cover the cost of the option before the client sees a true net profit.

The Collar Strategy

What if your client wants the insurance of a protective put, but refuses to pay the out-of-pocket premium? We construct a collar. A collar strategy involves holding a long stock position while simultaneously buying a protective put and writing a covered call.

Investors use a collar strategy to protect a long stock position against downside risk without draining their cash reserves. In a collar strategy, the premium received from writing the call directly offsets the cost of buying the protective put. You are capping your upside potential to fund the protection of your downside.

Ratio Writing: The Hybrid Danger

There are times when an investor attempts to accelerate their income by writing more option contracts than the investor holds equivalent shares in the underlying stock. This is known as ratio writing.

For example, a client holding 100 shares of stock writes two call options against it. This is critically important for the Series 7: a ratio write strategy contains both covered and uncovered option positions simultaneously. One contract is covered by the 100 shares; the second is dangerously exposed. Therefore, ratio writing exposes the investor to unlimited risk due to the uncovered portion of the strategy.

When an investor writes (sells) an option without owning the underlying asset or having the cash to cover the obligation, they enter the realm of uncovered writing. This is pure, unhedged risk transfer. Because of this, uncovered option writing strictly requires the investor to meet high margin requirements due to substantial risk.

Uncovered Calls

Uncovered call writing involves selling a call option without owning the underlying stock. The investor collects a premium and hopes the stock stays below the strike price so the option expires worthless.

- Maximum Gain: The maximum gain for an uncovered call equals the premium received. That is all you can ever make.

- Maximum Loss: The maximum loss for an uncovered call is theoretically unlimited. If the stock rallies to infinity, the writer is obligated to buy the stock at an infinitely high price in the open market just to sell it to the buyer at the lower strike price.

Uncovered Puts

Uncovered put writing involves selling a put option without holding sufficient cash to purchase the underlying stock. The investor is betting the stock will stay flat or rise.

- The Obligation: An uncovered put writer is obligated to buy the stock at the strike price upon option exercise.

- Maximum Loss: The maximum loss for an uncovered put equals the strike price minus the premium received. If the stock falls to absolute zero, the writer is still forced to buy worthless shares at the strike price, cushioned only by the initial premium.

If absolute direction is a blunt instrument, and naked writing is a dangerous gamble, spreads are the precision scalpel of the options market. A spread involves buying and selling two options of the exact same class (both calls or both puts) on the exact same underlying security. By combining a long and a short position, you cap your maximum risk—and necessarily cap your maximum reward.

Classifying Spreads

Spreads are categorized by how the two legs differ:

- Price Spread: A price spread involves buying and selling two options with different strike prices. The options in a price spread share the exact same expiration date. Due to the way strike prices are listed vertically on option chains, a price spread is formally known in the securities industry as a vertical spread.

- Time Spread: A time spread involves buying and selling two options with the exact same strike price, but the options in a time spread have completely different expiration dates. Because time marches forward horizontally on a calendar, a time spread is formally known in the securities industry as a horizontal spread or calendar spread.

- Diagonal Spread: A diagonal spread involves buying and selling two options with different strike prices and different expiration dates.

The Engine of Spreads: Debits vs. Credits

To understand spreads mechanically, you must look at the cash flowing into and out of the client's account.

Debit Spreads A debit spread occurs when the premium paid for the long option exceeds the premium received for the short option. You are paying money out of pocket to establish the position.

- Because you are a net buyer, investors want debit spreads to widen in value to achieve maximum profitability. You buy an asset, you want it to get bigger so you can sell it for more.

- Maximum Risk: The maximum risk for a debit spread equals the net debit paid to establish the position.

- Maximum Gain: The maximum gain for a debit spread equals the difference between the strike prices minus the net debit paid.

Credit Spreads A credit spread occurs when the premium received for the short option exceeds the premium paid for the long option. You are collecting cash upfront.

- Because you are a net seller, investors want credit spreads to narrow in value so the options expire worthless, allowing the investor to keep the initial credit.

- Maximum Reward: The maximum reward for a credit spread equals the net credit received when establishing the position.

- Maximum Loss: The maximum loss for a credit spread equals the difference between the strike prices minus the net credit received.

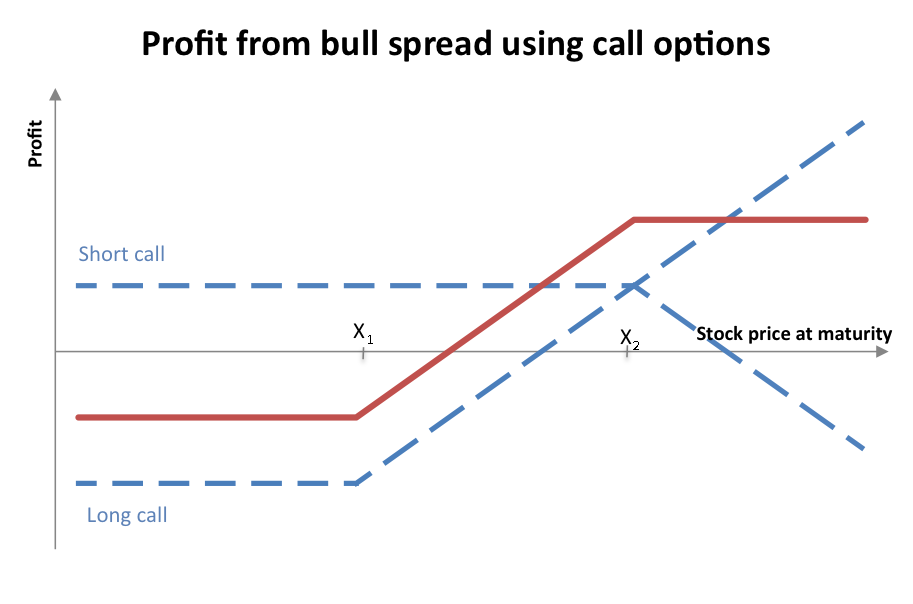

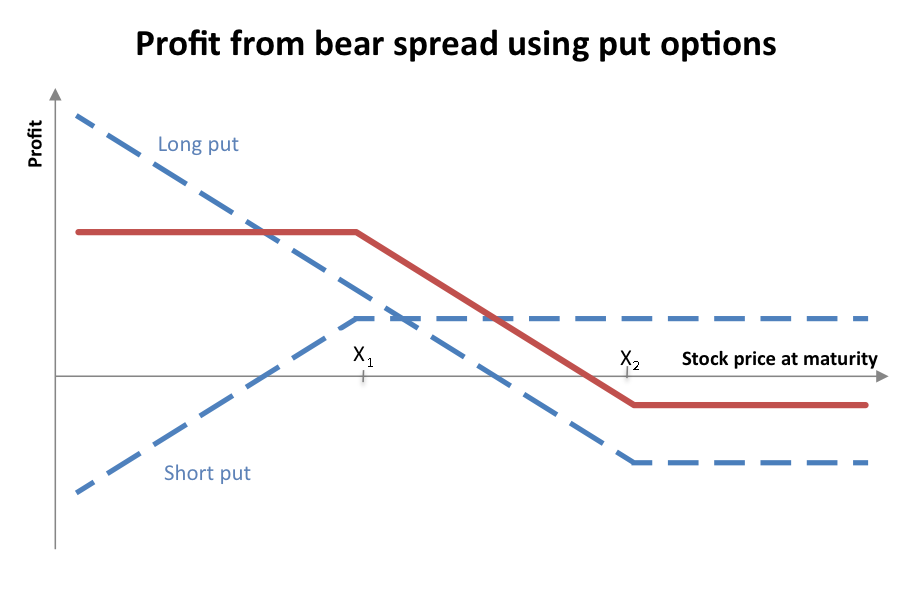

Directional Spreads: Bulls and Bears

How do you know if a spread is bullish or bearish? The dominant leg of an option spread determines the overall bullish or bearish market sentiment. The option contract with the higher premium represents the dominant leg in an option spread. If you buy the more expensive call, you are bullish. If you sell the more expensive call, you are bearish.

- A bull spread involves buying an option with a lower strike price and selling an option with a higher strike price. (Remember: call options with lower strikes are more expensive; put options with higher strikes are more expensive).

- A bear spread involves buying an option with a higher strike price and selling an option with a lower strike price.

Let's matrix these rules together for the Series 7:

- A bull call spread functions strictly as a debit spread. (You buy the lower, more expensive call).

- A bear call spread functions strictly as a credit spread. (You sell the lower, more expensive call).

- A bear put spread functions strictly as a debit spread. (You buy the higher, more expensive put).

- A bull put spread functions strictly as a credit spread. (You sell the higher, more expensive put).

Calculating Spread Breakevens

For the exam, you must instantly calculate the point at which a spread breaks even. We rely on two standard acronyms based entirely on whether the spread uses Calls or Puts.

CAL: Call Add Lower The acronym CAL stands for Call Add Lower to help remember the call spread breakeven calculation. The breakeven point for any call spread is calculated by adding the net premium to the lower strike price.

PSH: Put Subtract Higher The acronym PSH stands for Put Subtract Higher to help remember the put spread breakeven calculation. The breakeven point for any put spread is calculated by subtracting the net premium from the higher strike price.

What happens when a client knows a major event is imminent—such as a pharmaceutical FDA trial result or a critical earnings report—but they have absolutely no idea whether the stock will gap up or gap down? They must strip away directional risk and trade pure volatility.

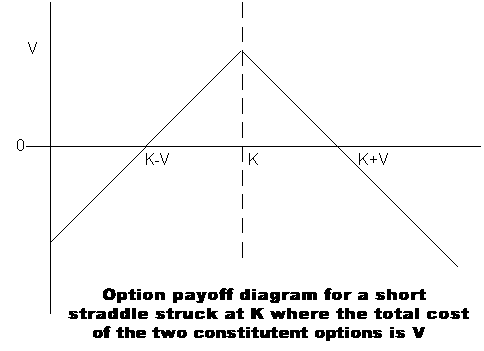

The Mechanics of Straddles

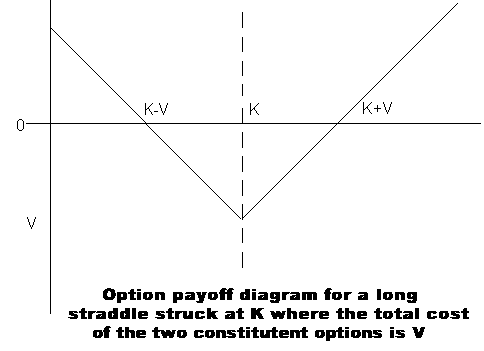

A straddle involves buying or selling both a call and a put option with the exact same strike price and expiration date. Because you are playing both sides of the market, a straddle always features two distinct breakeven points.

- The upside breakeven point for a straddle equals the strike price plus the total premium.

- The downside breakeven point for a straddle equals the strike price minus the total premium.

Long Straddles A long straddle investor expects significant price volatility in the underlying stock. They buy the call and buy the put.

- The Advantage: A long straddle investor does not need to predict the direction of the underlying stock's price movement to profit. As long as it moves violently past one of the breakeven points, they win.

- Maximum Loss: The maximum loss for a long straddle equals the total premium paid for both options (this happens if the stock sits perfectly dead at the strike price).

- Maximum Gain: The maximum gain for a long straddle is theoretically unlimited if the underlying stock price rises. Conversely, a long straddle can achieve substantial gains if the underlying stock price falls completely to zero.

Short Straddles On the other side of the trade sits the short straddle. A short straddle investor expects the underlying stock's price to remain relatively stable. They sell the call and sell the put, collecting a massive double premium.

- Maximum Gain: The maximum gain for a short straddle equals the total premium received from selling both options.

- Maximum Loss: Because they are exposed to a naked call on the upside and a naked put on the downside, the maximum loss for a short straddle is theoretically unlimited. This strategy is reserved for sophisticated institutions.

Combinations and Strangles

Finally, we have combinations. While a straddle uses the exact same strike and expiration, an option combination consists of a call and a put on the same underlying stock with different strike prices. Alternatively, an option combination can also consist of a call and a put on the same underlying stock with different expiration dates.

Like the long straddle, a long combination investor profits from extreme price volatility in either market direction.

A highly testable subset of the combination is the strangle. A strangle is a specific type of combination involving out-of-the-money call and put options. By buying out-of-the-money strikes instead of at-the-money strikes, the investor dramatically lowers the premium cost of establishing the position. The trade-off? The stock must move significantly further in one direction to overcome the wider breakeven points.

As a Series 7 practitioner, your mastery of these formulas and definitions is merely the baseline. Your true professional value lies in diagnosing a client's specific market anxiety—fear of a crash, need for yield, anticipation of a breakout—and prescribing the exact mathematical architecture required to solve it. Know the limits of the risk, recognize the dominant legs, and respect the mechanics of the premium.