Packaged Products: Mutual Funds and ETFs

Imagine trying to build a perfectly diversified portfolio by buying single shares of five hundred different companies. The transaction costs alone would obliterate your capital, and the administrative burden of tracking the dividends and corporate actions would require a full-time staff. Retail investors face an inherent scale problem: they need the safety of massive diversification but lack the capital to achieve it efficiently. The solution to this structural market problem is the packaged product—a pooled investment vehicle where thousands of investors aggregate their capital to buy a massive, professionally managed slice of the global economy. As a securities representative, understanding the mechanics, pricing, and taxation of these vehicles is not just a regulatory requirement; it is the fundamental architecture of how you will help clients build wealth over their lifetimes.

The blueprint for modern pooled investments was established by the Investment Company Act of 1940. This legislation was designed to protect the public from the opaque and often catastrophic pooling schemes of the 1920s. To bring order to the market, the Act classifies investment companies into three distinct types: face-amount certificate companies, unit investment trusts, and management companies.

Face-amount certificate companies are essentially financial dinosaurs—largely extinct debt certificates that promise to pay a fixed face amount at maturity. The two classifications that dominate your day-to-day reality in the securities industry are Unit Investment Trusts (UITs) and Management Companies.

Unit Investment Trusts (UITs)

Think of a Unit Investment Trust like a museum exhibit: once the curator selects the pieces, they are locked behind glass. UITs hold a fixed, unmanaged portfolio of securities. Because the portfolio is static, UITs do not employ an investment adviser for active portfolio management. There is no trading, no rebalancing to chase market trends, and no management fee. Furthermore, UITs are structurally finite; they have a specified termination date. When that date arrives, the trust is dissolved, the underlying securities are liquidated, and the proceeds are distributed to the investors.

Management Companies: Open-End vs. Closed-End

Unlike static UITs, management companies actively buy and sell securities within their portfolios to achieve a specific objective. The 1940 Act dictates that management investment companies are categorized as either open-end companies or closed-end companies.

Understanding the structural divergence between these two is vital. The difference lies entirely in how they are capitalized and how investors buy and sell their shares.

Open-end management investment companies are commonly referred to as mutual funds. They are designed to be vast, elastic pools of capital that grow and shrink dynamically with investor demand.

Because they are "open," open-end management investment companies continuously issue new shares to investors in the primary market. There is no fixed number of shares. Due to this continuous primary issuance, open-end investment companies are only permitted to issue common stock. They cannot complicate their capital structure with preferred stock or bonds.

Furthermore, mutual fund shares are non-negotiable and do not trade in the secondary market. You cannot sell your mutual fund shares to another investor on the New York Stock Exchange. Instead, mutual fund shares must be redeemed by the issuing open-end management company. The fund acts as the ultimate buyer and seller.

Pricing Mutual Funds: NAV and Forward Pricing

Because mutual funds do not trade on an exchange, their pricing cannot be dictated by intraday supply and demand. Instead, open-end funds must calculate their Net Asset Value (NAV) at least once per business day, typically at the 4:00 PM Eastern market close.

Net Asset Value per Share = Total Net Assets of the Fund ÷ Number of Outstanding Shares

When an investor wishes to sell (redeem) their shares, mutual fund redemptions are executed at the current Net Asset Value. But what happens when an investor places an order at noon? Do they get yesterday's closing price? No.

To prevent arbitrageurs from exploiting known prices, the industry uses forward pricing. Forward pricing requires mutual fund orders to be executed at the next calculated Net Asset Value after the order is received. If a client submits a redemption order at 1:00 PM on Tuesday, their execution price is the NAV calculated at 4:00 PM that afternoon. They trade blind, ensuring fair pricing for all participants in the pool.

When buying, mutual fund shares are purchased at the Public Offering Price (POP).

Public Offering Price (POP) = Net Asset Value (NAV) + Sales Charge

By regulatory statute, FINRA rules cap the maximum permitted sales charge on a mutual fund at 8.5 percent of the Public Offering Price.

Because mutual funds are continuous primary offerings that must be fully paid for, mutual fund shares cannot be purchased on margin. Consequently, because they are not traded in the secondary market and cannot be borrowed, mutual fund shares cannot be sold short.

In contrast to the elastic nature of mutual funds, closed-end management investment companies issue a fixed number of shares through an initial public offering (IPO). Once the IPO is complete, the doors to the primary market close. Because their capital structure is fixed and stable, closed-end investment companies are permitted to issue common stock, preferred stock, and bonds to leverage their portfolios.

Once issued, closed-end fund shares trade in the secondary market on stock exchanges or over-the-counter. Because they trade between investors rather than being redeemed by the issuer, closed-end fund shares are priced based on secondary market supply and demand—not strictly by their NAV.

This leads to a fascinating market phenomenon: closed-end fund shares can trade at a premium to their Net Asset Value if investor demand is high, or they can trade at a discount to their Net Asset Value if the fund falls out of favor.

Furthermore, because these shares trade on exchanges, transactions in closed-end fund shares incur standard brokerage commissions rather than mutual fund sales charges.

Exchange-Traded Funds (ETFs) were engineered to offer the diversification of a mutual fund with the trading flexibility of a closed-end fund. From a regulatory standpoint under the 1940 Act, Exchange-Traded Funds are legally classified as open-end funds or unit investment trusts. However, their mechanism of action is entirely different.

Exchange-Traded Funds trade on exchanges continuously throughout the trading day. Because they act like standard secondary market equities, Exchange-Traded Funds can be purchased on margin and can be sold short. This makes them highly attractive for sophisticated traders, institutional hedges, and retail investors who desire intraday liquidity rather than waiting for a mutual fund's end-of-day forward pricing.

Mutual funds charge investors for the cost of distribution and marketing through distinct share classes. Each class represents ownership in the exact same underlying portfolio, but applies a different fee structure.

Class A Shares and Breakpoints

Class A mutual fund shares charge a front-end sales load assessed at the time of purchase. The deduction is taken immediately, meaning less of the investor's initial capital goes into the market. However, Class A mutual fund shares offer breakpoints to reduce the sales charge for large investments. A mutual fund breakpoint is a specific dollar level of investment that qualifies the investor for a reduced sales charge percentage.

To determine the sales charge mathematics:

Mutual Fund Sales Charge % = Sales Charge Dollar Amount ÷ Public Offering Price

Public Offering Price = Net Asset Value ÷ (100% - Sales Charge %)

To help investors reach these cost-saving thresholds, funds offer two major mechanisms:

- Letter of Intent (LOI): A Letter of Intent allows an investor to qualify for a breakpoint discount by committing to invest a specified amount over a 13-month period. To provide immediate utility, a mutual fund Letter of Intent can be backdated up to 90 days to include prior purchases in the total commitment. What if the client breaks their promise? If an investor fails to complete a Letter of Intent within 13 months, the mutual fund liquidates escrowed shares to pay the higher sales charge they should have been assessed from the beginning.

- Rights of Accumulation (ROA): Rights of Accumulation allow an investor to combine existing mutual fund holdings with new purchases to qualify for breakpoint discounts. Notably, under Rights of Accumulation, existing mutual fund holdings are usually valued at the current Net Asset Value to determine breakpoint eligibility. This means market appreciation of their existing shares can push them over a breakpoint threshold without additional cash outlay.

Regulatory Warning: As a registered representative, you must be hyper-vigilant regarding breakpoint sales. A breakpoint sale is the strictly prohibited practice of inducing a mutual fund purchase just below a breakpoint level to earn a higher commission. If a breakpoint is at $50,000, letting a client invest $49,500 without disclosing that another $500 would substantially lower their fees is an immediate compliance violation.

Class B and Class C Shares

Class B mutual fund shares charge a contingent deferred sales charge (CDSC) assessed at the time of redemption. The investor pays no front-end load, allowing 100% of their capital to enter the market immediately. The CDSC drops incrementally over time (e.g., 5% if sold in year 1, 4% in year 2). Eventually, the CDSC reaches zero, at which point Class B mutual fund shares automatically convert to Class A shares after a specified holding period, granting the investor the lower ongoing operating expenses associated with Class A.

Class C mutual fund shares assess a level load typically composed of an ongoing annual 12b-1 fee. Crucially, Class C mutual fund shares do not offer breakpoint discounts. They are generally suitable only for short-to-intermediate time horizons where paying a front-end or deferred load would be mathematically inferior.

The 12b-1 Fee

The 12b-1 fee is an annual fee levied against a mutual fund's assets to cover marketing and distribution costs. It pays for advertising, printing prospectuses, and compensating representatives.

FINRA rules limit the maximum 12b-1 fee for marketing and distribution to 0.75 percent of average net assets. Some funds market themselves as "no-load" funds, meaning they assess no front-end or back-end sales charges. However, a mutual fund must not charge a 12b-1 fee exceeding 0.25 percent to describe itself as a no-load fund.

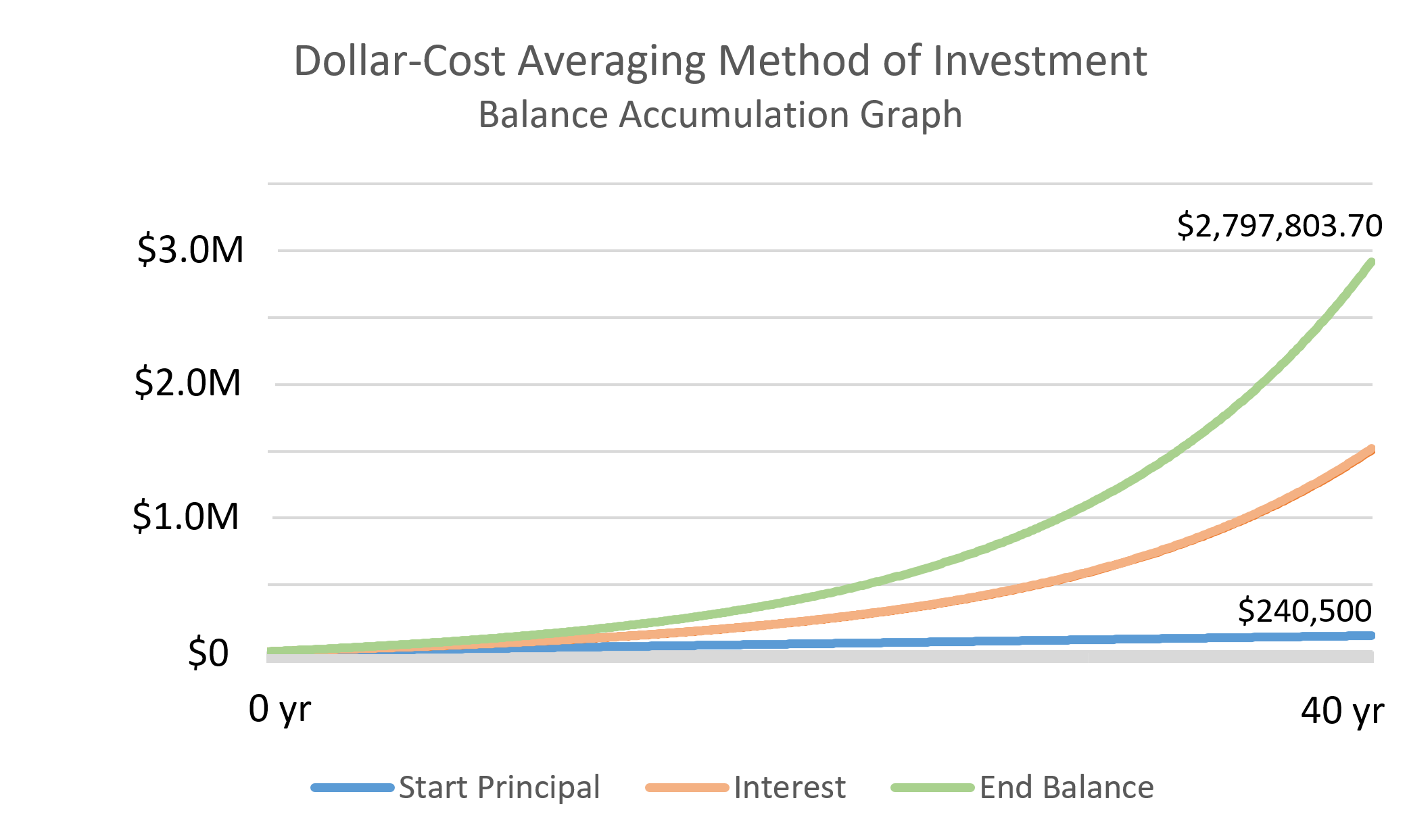

Clients often ask if they should try to "time the market." The answer is usually no. Instead, professionals utilize dollar-cost averaging (DCA).

Dollar-cost averaging involves investing a fixed dollar amount into a specific security at regular time intervals (e.g., investing $500 on the 1st of every month). The mathematical beauty of this strategy is that dollar-cost averaging results in purchasing more shares when the market price is low and fewer shares when the market price is high.

If a fund's shares are $10, $500 buys 50 shares. If the market crashes and shares fall to $5, that same $500 buys 100 shares. Over time, a successful dollar-cost averaging strategy results in an average cost per share that is lower than the average price per share over the investment period.

However, DCA is an accumulation strategy, not a magic shield. You must disclose that dollar-cost averaging does not guarantee a profit or protect against a loss in a declining market. If the underlying asset permanently goes to zero, the investor still loses their money.

When a corporation earns a profit, it pays corporate income tax. If it distributes dividends to shareholders, those shareholders pay tax on the dividends. This is double taxation. If a mutual fund faced this same fate, the compounded drag of double taxation would destroy the viability of pooled investments.

To solve this, Subchapter M of the Internal Revenue Code establishes the conduit theory for regulated investment companies (RICs). Think of the fund not as a taxable entity, but as a hollow pipe (a conduit) funneling money directly to the investor. A mutual fund qualifies as a regulated investment company by passing taxes on distributed income through to the shareholders.

To qualify under Subchapter M, an investment company must distribute at least 90 percent of its net investment income to shareholders. If it does, the fund itself pays zero taxes on the distributed amount.

Net Investment Income (NII) = Total Dividends + Interest Received - Fund Operating Expenses

Distributions and Shareholder Taxes

Funds distribute two primary forms of cash flow: dividends and capital gains.

When a mutual fund pays a dividend out of its net investment income, a mechanical adjustment occurs: the Net Asset Value per share drops by the exact amount of the dividend on the ex-dividend date. The value didn't vanish; it simply left the portfolio and entered the investor's pocket.

Mutual fund capital gains distributions are derived from the fund's realized long-term capital gains. Because these distributions rely on the fund's realization schedule, mutual funds may only distribute long-term capital gains to shareholders once per year.

Critical Tax Rule: Mutual fund shareholders report capital gains distributions as long-term capital gains regardless of how long the shareholder has owned the fund shares. If the fund held a stock for three years, sold it for a profit, and distributed the gain, an investor who bought the mutual fund just yesterday still claims it as a long-term capital gain. The holding period of the fund dictates the tax treatment, not the holding period of the investor.

Reinvestment and Exchanges

Investors routinely elect to reinvest their distributions to harness compound growth. However, reinvested mutual fund dividends and capital gains are fully taxable to the shareholder in the year they are distributed. The IRS taxes the economic benefit, regardless of whether the investor touched the cash.

Because the investor has already paid taxes on these reinvested amounts, reinvesting mutual fund distributions increases the investor's cost basis in the mutual fund. This prevents the investor from being taxed twice on the same money when they eventually sell their shares. Fortunately, as a benefit to the investor, reinvesting mutual fund distributions at the Net Asset Value avoids the application of a new sales charge.

Finally, clients frequently alter their asset allocation, perhaps shifting from an aggressive growth fund to a conservative bond fund. Exchanging shares between different mutual funds within the same fund family typically avoids the assessment of a new sales charge, granting the investor mobility without friction. However, do not confuse a waiver of sales charges with a waiver of taxes. An exchange of shares between different mutual funds within the same fund family is considered a taxable event. The IRS views it strictly as a sale of the old fund (triggering a capital gain or loss) followed by a purchase of the new fund.