REITs and Direct Participation Programs (DPPs)

When a standard C-corporation earns a dollar of profit, the Internal Revenue Service extracts a portion before that profit ever reaches the shareholder. When the remaining fraction is distributed as a dividend, the shareholder is taxed again. This double taxation creates massive friction in capital markets. Real Estate Investment Trusts (REITs) and Direct Participation Programs (DPPs) exist as structural solutions to this friction. They act as economic conduits, allowing the cash flows and tax consequences of massive, capital-intensive projects—like skyscrapers and oil fields—to pass directly to the individual investor.

As a Series 7 candidate, you must understand not just the definitions of these vehicles, but their mechanics. You are learning to construct portfolios for clients who want access to heavy industry and real estate, but who are acutely sensitive to tax liabilities, liquidity constraints, and liability exposure.

A Real Estate Investment Trust manages a portfolio of real estate investments to earn profits for shareholders. Instead of an investor buying a single apartment complex, they buy shares in a REIT, which pools capital to purchase dozens of complexes.

The Three Architectures of REITs

REITs are classified by the nature of the assets they hold.

| REIT Type | Primary Source of Income | Market Behavior |

|---|---|---|

| Equity REITs | Generate income primarily through rent collected on owned commercial or residential properties. | Behaves somewhat like a traditional equity, offering potential capital appreciation of the underlying properties. |

| Mortgage REITs | Generate income primarily from the interest earned on mortgage loans and mortgage-backed securities. | Behaves more like a fixed-income investment, highly sensitive to interest rate fluctuations. |

| Hybrid REITs | Hold both physical real estate properties and real estate mortgages. | Blends the rental income of Equity REITs with the interest income of Mortgage REITs. |

The Tax Compromise: Subchapter M

A Real Estate Investment Trust avoids corporate taxation on distributed income under Subchapter M of the Internal Revenue Code. However, the IRS does not grant this benefit without strict conditions. To qualify for this conduit taxation, a REIT must strictly adhere to three numerical rules:

- The 75 Percent Asset Rule: Real Estate Investment Trusts must hold at least 75 percent of total assets in real estate, cash, or US Government securities.

- The 75 Percent Income Rule: Real Estate Investment Trusts must derive at least 75 percent of gross income from real estate-related activities.

- The 90 Percent Distribution Rule: A Real Estate Investment Trust must distribute at least 90 percent of taxable income to shareholders to avoid corporate taxation on the distributed portion.

If a REIT meets these conditions, the entity pays no tax on the money it distributes. However, the tax burden does not disappear; it merely shifts to the investor. Dividends paid by Real Estate Investment Trusts are generally taxed as ordinary income to the investor. Because these dividends avoid taxation at the corporate level, dividends paid by Real Estate Investment Trusts do not qualify for the lower corporate dividend tax rate.

Crucial Distinction for the Series 7: Real Estate Investment Trusts pass through income to shareholders. However, Real Estate Investment Trusts do not pass through losses to shareholders. If the REIT operates at a loss, that loss stays trapped at the corporate level.

Unlike traditional partnerships, exchange-traded Real Estate Investment Trusts offer high liquidity for investors. An investor can buy or sell shares of a publicly traded REIT on an exchange with the click of a button, providing an exit valve that direct real estate ownership lacks.

Direct Participation Programs are pooled investments providing exposure to the cash flow and tax benefits of an underlying business. If a REIT is a specialized real estate mutual fund, a DPP is a literal partnership in a specific venture.

Direct Participation Programs function as flow-through tax entities. Because of this, Direct Participation Programs do not pay income taxes at the entity level. Instead, Direct Participation Programs pass income, gains, losses, deductions, and credits directly to individual investors.

The Nature of Passive Income and Losses

Because the investors in a DPP are not actively managing the oil well or apartment building, the IRS tightly regulates how they can use the losses the business generates.

Losses generated by Direct Participation Programs are classified as passive losses by the Internal Revenue Service.

- Passive losses from Direct Participation Programs can only be used to offset passive income.

- Passive losses from Direct Participation Programs cannot be used to offset ordinary earned income (like your client's salary) or portfolio investment income (like dividends from stock).

If a client has \10,000inpassivelossesfromaDPP,theycanonlydeductthatagainst$10,000$ of passive income from another partnership.

Almost all DPPs are structured as limited partnerships. A limited partnership requires at least one general partner (GP) and at least one limited partner (LP).

The General Partner: The Operator

The general partner manages the day-to-day operations of the limited partnership. Because they hold the steering wheel, the law demands they carry the ultimate financial burden: the general partner has unlimited personal liability for the debts of the limited partnership. If the partnership goes bankrupt, creditors can seize the GP's personal assets.

To protect the vulnerable limited partners, the law dictates that the general partner owes a fiduciary duty to the limited partners. To enforce this duty, strict boundaries exist:

- The general partner is prohibited from borrowing money from the limited partnership.

- The general partner is prohibited from commingling personal assets with partnership assets.

The Limited Partner: The Funder

Limited partners provide capital to the business as passive investors without taking a management role. Because they have no operational control, they are shielded legally: limited partners have financial liability restricted to the amount of invested capital plus any assumed debt.

While they cannot interfere in management (doing so strips them of their liability protection), they are not entirely powerless. Limited partners possess the right to inspect the partnership books and records. Furthermore, limited partners possess the right to sue the general partner for breaching fiduciary duties.

When you analyze a DPP for a client, the primary consideration when evaluating a Direct Participation Program must be the economic soundness of the investment. A common mistake investors make is buying a bad business simply because it offers heavy tax write-offs. Economic soundness means the Direct Participation Program has a reasonable expectation of generating a profit independent of any tax benefits.

Once economic soundness is established, investors must evaluate the general partner's track record and expertise in managing similar ventures before investing in a Direct Participation Program. A brilliantly conceived pipeline project will fail if the GP has never built one.

Costs and Liquidity

Setting up a partnership is expensive. High start-up costs and syndication fees reduce the amount of capital available for actual investment in a Direct Participation Program. To prevent abuse, FINRA mandates that organization and offering expenses for a Direct Participation Program are legally limited to a maximum of 10 percent of the gross proceeds of the offering.

Unlike REITs, Direct Participation Programs are generally highly illiquid investments lacking an active secondary market. Clients must be prepared to lock up their capital for years.

The Subscription Agreement

To enter this illiquid structure, investors purchasing units in a Direct Participation Program must sign a subscription agreement, acknowledging their suitability and awareness of the risks. The contract is not executed upon the investor's signature alone; the general partner must sign the subscription agreement to formally accept the limited partner into the partnership.

Blind Pool vs. Specified Programs

DPPs take capital in two distinct ways:

- In a specified Direct Participation Program, the specific properties or assets to be acquired are identified before the offering. The investor knows exactly what they are buying.

- In a blind pool Direct Participation Program, less than 75 percent of the assets to be acquired are specified in the offering. The investor is heavily relying on the GP's expertise to find good assets after the money is raised.

An investor's tax basis dictates how much they can write off in losses. As an investor, you can only deduct losses up to your basis (your "skin in the game"). How does debt affect basis?

If an investor agrees to be legally responsible for a loan, it is called recourse debt. Because the investor is genuinely on the hook, assuming recourse debt increases a limited partner's tax basis in a Direct Participation Program.

If the debt is secured only by the asset itself (like a mortgage) and the lender cannot come after the investor's personal assets, it is non-recourse debt. Under general IRS rules, assuming non-recourse debt generally does not increase a limited partner's tax basis.

The Exception: Assuming non-recourse debt increases a limited partner's tax basis only in real estate Direct Participation Programs. Because mortgages are standard in real estate, the IRS allows non-recourse real estate loans to increase an investor's basis, amplifying their ability to take deductions.

Real estate DPPs are tailored to different investment objectives, from high-risk capital appreciation to low-risk tax abatement.

| Program Type | Investment Objective & Characteristics | Tax Implications |

|---|---|---|

| Raw Land | Seek long-term capital appreciation rather than current income. | Because land does not wear out, raw land real estate programs do not allow for depreciation deductions. |

| New Construction | Seeks appreciation and eventual income. | Carries the heavy risk of cost overruns and building delays. |

| Existing Property | Aim to generate immediate rental income streams with moderate risk. | Allows for predictable depreciation deductions. |

| Government-Assisted Housing | Constructed to meet municipal housing mandates. | Provide investors with tax credits rather than significant capital appreciation. |

To understand the immense value of government-assisted housing, you must understand the difference between deductions and credits.

- Tax deductions reduce the amount of taxable income subject to taxation. If you have a \10,000deductionanda30$3,000$ in taxes.

- Tax credits provide a dollar-for-dollar reduction in a taxpayer's actual tax liability. If you have a \10,000taxcredit,yourfinaltaxbillisreducedbyexactly$10,000$.

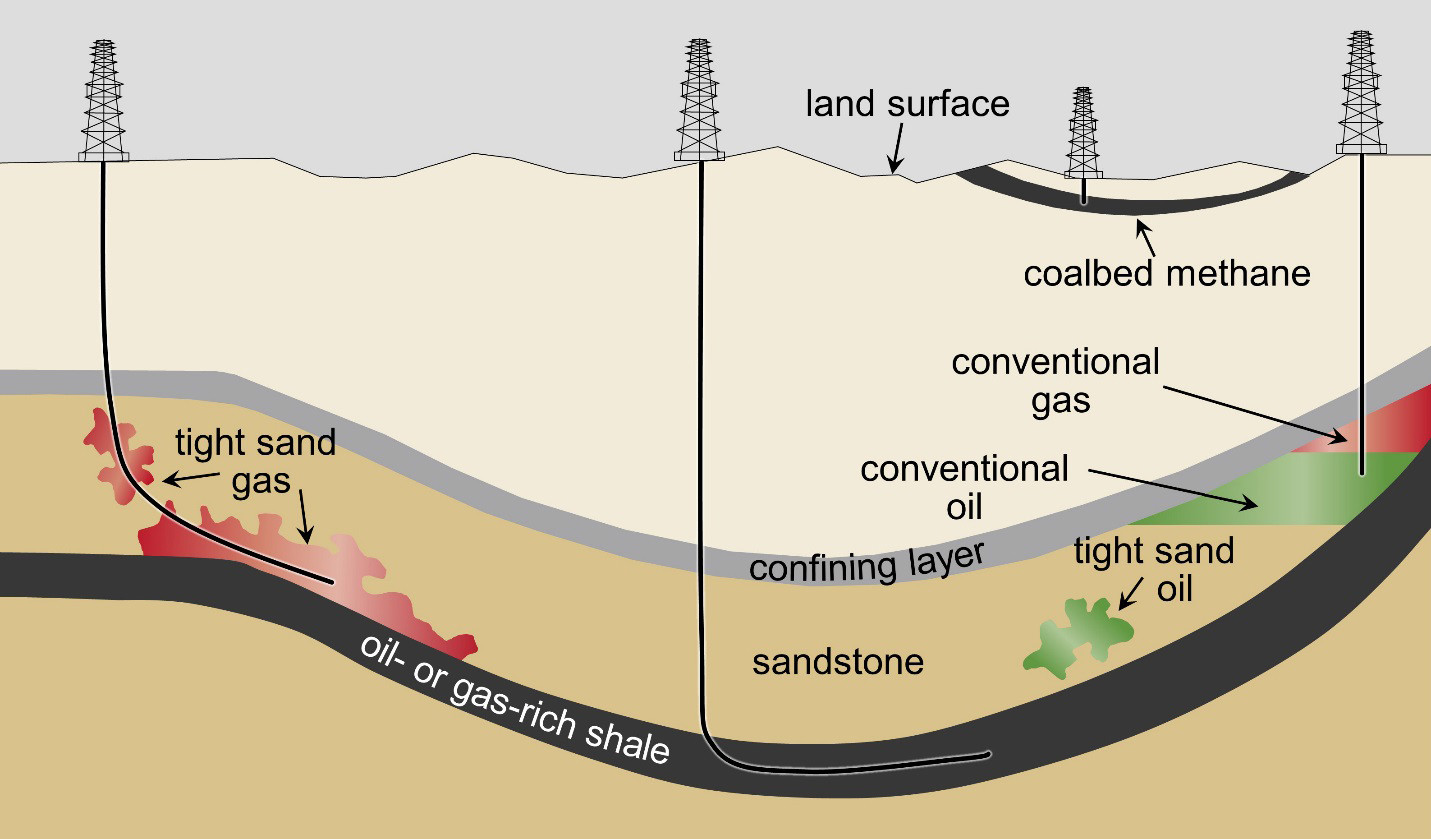

Oil and Gas DPPs operate on a spectrum of geological risk.

- Exploratory Programs (Wildcatting): Involve drilling in areas without proven energy reserves. Because the operators are blindly searching for new reservoirs, exploratory oil and gas programs carry the highest level of risk among all oil and gas programs.

- Developmental Programs: Reduce risk by drilling near existing producing wells. The oil is known to be in the region; the operator is simply tapping an adjacent node.

- Income Programs: Generate revenue by purchasing already producing wells. There is no drilling risk; the primary risk is the fluctuating market price of the extracted commodity.

The Tax Benefits of Drilling

The US government aggressively incentivizes domestic energy production through unique tax benefits.

The first major benefit involves the costs of digging the hole. Intangible drilling costs (IDCs) include non-salvageable expenses such as labor, fuel, and geological surveys. If you dig a dry hole, you cannot sell the fuel you burned or un-pay the laborers. Because these costs hold no residual value, intangible drilling costs are fully deductible in the tax year the costs are incurred. This provides massive, immediate tax relief to the investor in the first year of the program.

The second major benefit involves the extraction of the oil itself. As oil is pumped out of the ground, the reserve permanently shrinks. Depletion allowances provide a tax deduction to compensate for the gradual exhaustion of a natural resource. Just as an apartment building depreciates over time, an oil well depletes over time, and the IRS allows the investor to shield a portion of their income to reflect that loss of underlying asset volume.

By mastering the conduit mechanics of REITs and DPPs, you bridge the gap between heavy, illiquid physical assets and the nuanced tax and income needs of the individual investor. The Series 7 demands you view these structures not merely as investments, but as precise tools for navigating liability, taxation, and risk.