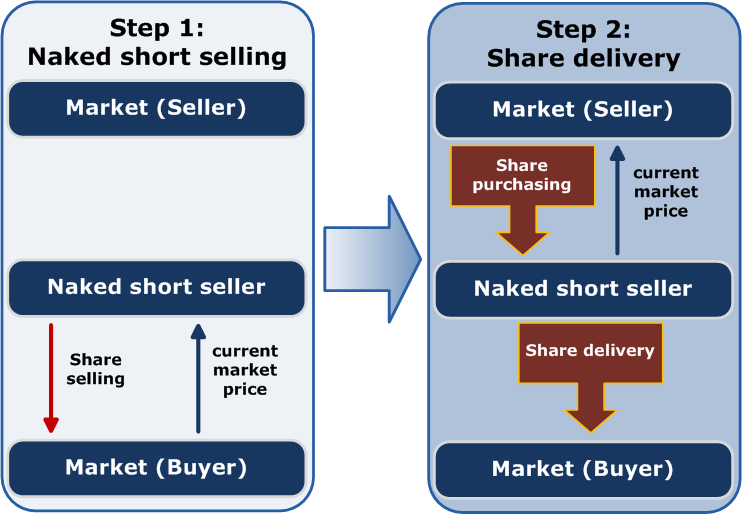

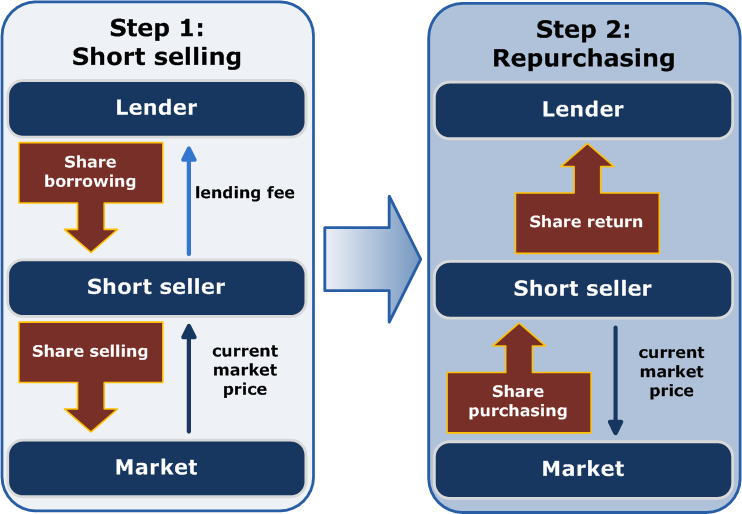

Short Sales and Securities Lending

Imagine you have a neighbor who owns a rare vintage watch. You notice the market for this specific watch is driven by a speculative frenzy, and you are mathematically certain the bubble is about to burst. You ask to borrow the watch, promising to return it next month. You immediately walk down the street and sell it to a stranger for $20,000. Three weeks later, the market collapses as you predicted. You buy the exact same model watch on the open market for $12,000, return it to your neighbor, and pocket an $8,000 profit.

This is the mechanical essence of a short sale: a transaction in which an investor sells borrowed securities in anticipation of a price decline. But what happens if you are wrong? What if the watch becomes an overnight sensation and the price spikes to $100,000? You still owe your neighbor a watch.

Because a stock's price can theoretically rise to infinity, the maximum potential loss for a short sale transaction is unlimited. This asymmetry of risk—where your maximum gain is capped (a stock can only fall to zero) but your maximum loss has no ceiling—is why regulators treat short selling with intense scrutiny. If market participants were allowed to sell shares they did not own without strict controls, the financial system would quickly fill with "phantom" shares, leading to catastrophic settlement failures.

As a Series 7 candidate, you are stepping into the role of a gatekeeper. Your daily reality will involve navigating the precise, heavily regulated mechanics of how we locate, borrow, mark, and deliver these borrowed securities.