Trade Processing and Settlement

The architecture of the global securities market relies entirely on the precise, verifiable execution of promises. When a registered representative presses a key to buy or sell a security, they do not physically move capital or certificates in that instant; they initiate a cascading sequence of legal, financial, and administrative obligations. If this machinery breaks down, the market ceases to function. For the securities professional, understanding trade processing, regulatory reporting, and settlement is not merely an exercise in compliance—it is the engineering diagram of the capital markets. Without absolute fidelity in how orders are captured, executed, and settled, liquidity dissolves into chaos.

Every transaction begins with a record of intent. The order ticket is the genesis block of a trade, providing an exact, auditable map of what was requested and by whom. Regulators do not care what a representative meant to do; they care what the order ticket explicitly dictates.

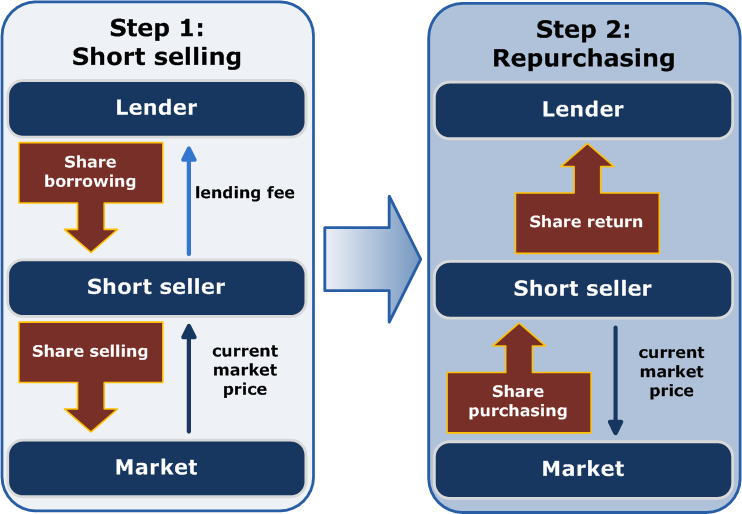

To be valid, an order ticket must specify the exact quantity of securities to be bought or sold, define the order type (e.g., market, limit), and include any time-in-force instructions (such as Day or Good-Til-Canceled). It must include the specific security symbol, though the ticket may include a security description in place of a security symbol. For equities, an order ticket for a stock sale must designate if the sale is a long sale or a short sale.

Equally critical is the documentation of human involvement. The ticket must include the customer account number, though it may use the customer account name in place of an account number. It must definitively state whether the registered representative exercised discretionary authority in placing the order, and whether the trade was solicited by the registered representative or unsolicited by the customer. Furthermore, the record must identify the registered representative associated with the account and identify the specific person who accepted the order from the customer.

To maintain temporal precision, an order ticket is subjected to a rigorous timestamping regime. An order ticket must bear a time stamp for the time of order receipt, the time of order entry, the time of order execution, and, if applicable, the time of order cancellation.

Interestingly, there are limits to what this document must capture. An order ticket does not require the customer's current address to be valid, nor does it require the current market price of the security at the time of order entry.

Correcting the Record Because the order ticket is a binding legal record, any change to an executed order ticket requires the approval of a principal. For example, if a representative transposes digits in a client's profile, an error in a customer account number on an order ticket can only be corrected with principal authorization using a cancel and rebill record.

Once the order ticket is stamped, the order routes to the market. Here, the concept of a quote is paramount.

A firm quote is a market maker's definitive commitment to either buy a stated quantity of securities at the quoted bid price or sell a stated quantity of securities at the quoted ask price. If a market maker quote lacks a specified size, it is generally assumed to be firm for 100 shares. Failing to honor this published firm quote is a severe regulatory violation known as backing away.

Not all quotes represent an immediate willingness to trade. A subject quote is a tentative price indication provided by a dealer requiring confirmation before trade execution. Meanwhile, a workout quote provides an estimated price range for a block trade to be executed over time, preventing massive institutional orders from instantly crashing the market.

When multiple market makers publish firm quotes, we look to the inside market, which includes the highest bid price currently available and the lowest ask price currently available across all competing market makers. To ensure clients receive optimal pricing, the National Best Bid and Offer (NBBO) system aggregates market maker quotes to display the most favorable prices available for an equity security.

Modern execution rarely relies on humans shouting across trading floors. Automated execution systems route customer orders directly to market centers for immediate electronic matching. For massive institutional orders, market participants utilize dark pools—private alternative trading systems allowing institutional investors to execute large block trades anonymously. Crucially, dark pools do not reveal pre-trade quotes to the public market, preventing predatory front-running. However, transparency is preserved post-trade: trades executed in dark pools must be reported to the consolidated tape after execution.

Once an execution occurs, a stopwatch begins ticking. Regulators rely on real-time data to monitor market integrity, utilizing specific systems for different asset classes.

Equity and Option Reporting

- The Consolidated Audit Trail (CAT): This massive database tracks orders, order modifications, order cancellations, and trade executions for all US exchange-listed equities and options. As an evolution in market surveillance, the Consolidated Audit Trail completely replaced the older Order Audit Trail System (OATS) for tracking US equity and option orders.

- Trade Reporting Facility (TRF): The TRF is an automated electronic system used to report over-the-counter transactions in equity securities listed on national exchanges. It is vital to understand that the Trade Reporting Facility processes trade data for exchange-listed equities traded off-exchange, but the TRF does not execute equity trades. It is purely a reporting mechanism.

Debt Security Reporting

- Trade Reporting and Compliance Engine (TRACE): This is the FINRA system used to report over-the-counter transactions in eligible fixed-income securities, which include corporate bonds and agency debt securities. Broker-dealers must report corporate bond trades to TRACE as soon as practicable, with a maximum allowable time to report of 15 minutes after execution.

- Real-Time Transaction Reporting System (RTRS): Operated by the Municipal Securities Rulemaking Board (MSRB), this system is used to collect municipal bond trade data. Like TRACE, broker-dealers must report municipal bond transactions to the RTRS within 15 minutes of execution.

- Electronic Municipal Market Access (EMMA): While RTRS handles the raw trade data plumbing, EMMA serves the public. The EMMA system is the official source for municipal securities data and disclosure documents. It provides retail investors with free access to official statements for municipal bonds and real-time trade price data.

With the trade executed and reported, the broker-dealer must formally notify the client. A trade confirmation must be sent to a customer at or before the completion of a transaction, which is defined legally as the settlement date of the trade.

This document is highly prescriptive. A trade confirmation must disclose the trade date and the settlement date of the transaction. It must identify the security name, the unique security CUSIP number, whether the customer bought or sold, the exact quantity of securities traded, and the execution price.

Furthermore, it must illuminate the broker-dealer's role. A trade confirmation must disclose the capacity in which the broker-dealer acted—specifically, if the broker-dealer acted as an agent for the customer (matching buyers and sellers) or as a principal for the broker-dealer's own account (selling from or buying into their own inventory).

Compensation must be strictly transparent:

- A trade confirmation for an agency trade must explicitly disclose the commission charged to the customer.

- A trade confirmation for a principal trade in a corporate bond with a retail customer must disclose the dealer mark-up or mark-down.

Fixed-income confirmations carry additional mathematical burdens. A trade confirmation for a debt security must disclose the bond yield to maturity. If it is a callable debt security traded at a premium, it must disclose the yield to call. Because regulators demand conservative representations of returns, a trade confirmation must disclose the lower yield between the yield to maturity and the yield to call for a callable bond.

Execution is merely an agreement; settlement is the actual exchange of assets for capital.

The industry standard for timing is regular way settlement, which occurs one business day after the trade date (T+1) for:

- US equity transactions

- Corporate bond transactions

- Municipal bond transactions

- US government securities

- Equity option trades

If a client needs immediate closure, they can utilize cash settlement, which occurs on the same day as the trade date. Cash settlement demands velocity: it requires the delivery of securities before the close of business on the trade date, and the payment of funds before the close of business on the trade date.

Funding the Purchase: Regulation T

Settlement defines when the broker-dealers must exchange capital and securities. Regulation T, dictated by the Federal Reserve, defines when the customer must pay the broker-dealer.

Under the T+1 settlement cycle, Regulation T requires customers to pay for securities purchases no later than two business days after regular way settlement. Mathematically, a customer must pay for a securities purchase under Regulation T by the third business day following the trade date (T+3).

If a customer fails to pay by this Regulation T deadline, the broker-dealer has options, but they are severe. A broker-dealer may request a time extension from a designated examining authority (such as FINRA). If no extension is granted for a missed Regulation T payment, the firm must take two immediate actions:

- A broker-dealer must sell out the unpaid position.

- A broker-dealer must freeze the customer account for 90 days.

During this 90-day freeze, the customer loses the privilege of delayed payment. To execute a transaction, a customer must have the full purchase price in cash available in the account before entering any buy orders in a frozen account.

Good Delivery Mechanics

When transferring physical or electronic certificates, the industry abides by good delivery rules, which establish both the physical requirements and the administrative requirements for transferring securities ownership between parties.

For physical certificates to constitute good delivery, a physical stock certificate must be properly endorsed by the registered owner with a signature. Alternatively, a power of substitution form allows a physical security to be transferred when signed by the owner in place of endorsing the actual certificate. To prevent fraud, a Medallion Signature Guarantee is required to verify the authenticity of a registered owner's signature on a physical security certificate.

Physical delivery rules are highly specific to denominations:

- Equities: To constitute good delivery, equity certificates must be delivered in multiples of 100 shares. Equity certificates delivered in denominations smaller than 100 shares are considered good delivery only if the certificates can be assembled into units of exactly 100 shares. Odd-lot equity certificates constitute good delivery if the certificates total the exact number of shares traded.

- Bearer Bonds: For physical bearer bonds, a $1,000 denomination or a $5,000 denomination constitutes good delivery. Furthermore, a bond with missing unpaid interest coupons is not considered good delivery.

- Registered Physical Bonds: Denominations for good delivery must be in multiples of $1,000 up to a maximum of $100,000 per certificate.

If physical certificates are damaged, mutilated security certificates are not considered good delivery unless formally authenticated by the issuer or the transfer agent.

Mercifully, modern markets bypass much of this paperwork via the Depository Trust Company. Securities held in street name (registered in the name of the broker-dealer on behalf of the client) do not require physical endorsement for transfer, nor do they require a medallion signature guarantee for transfer.

The Due Bill: Managing Settlement Interruptions

Finally, timing discrepancies around dividend record dates are resolved using a due bill.

A due bill is a printed statement showing the transfer of a security title or rights when a transaction settles after the record date. If a buyer purchases a stock before the ex-dividend date, they are legally entitled to the upcoming dividend. However, if that trade happens to settle after the record date (meaning the seller is still technically on the issuer's books when the dividend is calculated), the seller will mistakenly receive the payout. A due bill is required when a dividend-paying stock trade settles after the record date for a purchase made prior to the ex-dividend date. It guarantees the buyer receives a pending dividend by legally forcing the seller to remit the funds to the rightful owner.