Supervisory Approvals and Maintenance

Imagine an active trading floor not as a marketplace, but as a nuclear reactor. The kinetic energy of capital flows—buying, selling, leveraging, and transferring—is immense and highly productive, but without an intricate system of control rods, containment vessels, and constant monitoring, a catastrophic failure is inevitable. In the securities industry, a broker-dealer's supervisory procedures act as these critical safeguards. A registered representative does not operate in a vacuum; every new account opened, every dollar deposited, and every trade executed sits within a rigid framework of principal approvals, physical segregation of assets, and strict regulatory restrictions. Understanding this framework is not merely a matter of compliance—it is the fundamental architecture that prevents systemic failure, protects the investing public from exploitation or insolvency, and ensures the structural integrity of the capital markets.

As a registered representative, your job is to build the business, but the firm itself bears the ultimate liability for the activity within its walls. Therefore, a designated principal must act as the final gatekeeper for account establishment and maintenance.

For standard cash accounts, the rule provides slight operational flexibility but unwavering ultimate authority: a principal must formally approve every new customer account. Mechanically, a principal must approve a new customer account promptly after the completion of the initial transaction, though they are certainly permitted to approve a new customer account prior to the completion of the initial transaction. Regardless of the exact sequence, the broker-dealer must document the exact date a new customer account is officially opened.

However, when we introduce risk or discretion, the sequence of approval becomes rigid.

- Options Accounts: Options inherently carry complex risks. Therefore, a Registered Options Principal (ROP) must formally approve a new options account, and they must do so before the customer enters the initial options trade.

- Discretionary Accounts: When you are given the authority to trade on a client's behalf without consulting them first, the potential for abuse increases. A principal must formally approve a discretionary account before the first trade is executed in the discretionary account. Once open, a principal must frequently review trading activity in a discretionary account to guard against churning (excessive trading to generate commissions).

- Margin Accounts: Lending a customer money to buy securities requires a formal contract. A principal must sign a margin agreement to formally approve a customer's margin account. Without this signature, an unapproved margin agreement restricts a customer from executing trades on margin.

The Flow of Information and Account Maintenance

A customer account is not a static document; it is a living reflection of an investor's life. When a client gets a promotion, inherits wealth, or suffers a setback, their financial profile shifts. A registered representative must update a customer account profile within 30 days of discovering a material change in the customer's financial situation.

If this material change leads to an update in how the account will be managed, a principal must formally approve any updates to a customer's investment objectives. To ensure the customer and the firm are on the same page, the broker-dealer must send a copy of the updated account record to a customer within 30 days of receiving notice of a change in investment objectives.

Furthermore, a principal's oversight extends to almost every administrative shift or external communication:

- A principal must approve any change of the designated registered representative assigned to a customer account.

- A principal must review and approve all retail communications related to a customer account.

Recordkeeping Reality Check: These files are not kept forever, but they outlast the client relationship. A broker-dealer must retain customer account records for six years following the closure of the customer account.

When a customer hands over money or shares, they are trusting the broker-dealer not to lose it, steal it, or use it to pay the firm's own light bills.

As a registered representative, your boundaries are absolute. A registered representative is strictly prohibited from personally holding customer funds or customer securities. You are an agent, not a vault. Customer checks remitted for investments must be made payable to the broker-dealer—they must never be made payable to the registered representative. If a client mistakenly hands you a check, a registered representative must immediately forward any received customer checks to the broker-dealer.

Once the firm has the assets, the SEC Customer Protection Rule dictates how they must be handled. The governing principle here is isolation. A broker-dealer must strictly segregate fully paid customer securities from the broker-dealer's own proprietary inventory. If the broker-dealer goes bankrupt, customer assets must not be tangled up with the firm’s debts.

To achieve this, the SEC Customer Protection Rule requires a broker-dealer to maintain physical possession or control of:

- All fully paid customer securities.

- All excess margin securities belonging to customers (securities whose value exceeds 140% of the customer's debit balance).

Vaults, Street Names, and the Special Reserve

How do we actually hold these securities? In the past, this meant mountains of paper. Today, a broker-dealer must physically secure all physical stock certificates held in vault storage. To ensure nothing has gone missing, a broker-dealer must conduct a quarterly physical count of all securities held in the broker-dealer's possession.

Most securities today, however, are not physical certificates. A broker-dealer holds securities in street name to facilitate the physical safeguarding and transfer of the securities. This means securities held in street name are registered in the name of the broker-dealer rather than the underlying customer, making it vastly easier to execute trades and transfer ownership without chasing down a client for a physical signature.

For cash, the protections are equally mathematical. A broker-dealer must calculate daily the amount of customer funds required to be deposited in a Special Reserve Bank Account. The Special Reserve Bank Account ensures customer funds are not used to finance a broker-dealer's proprietary trading activities.

To keep the customer informed of where their money is, a broker-dealer must issue account statements to customers at least quarterly, but must issue a monthly account statement for any customer account containing active trading during a given month.

Not all business is good business, and broker-dealers are private institutions. A broker-dealer possesses the absolute right to refuse to open an account for any prospective customer, and possesses the absolute right to refuse to execute a specific transaction for a customer.

When things go wrong, the firm must restrict or freeze accounts to mitigate risk.

| Circumstance | Action Required by the Broker-Dealer |

|---|---|

| Regulation T Payment Failure | If a customer fails to pay for a trade within the Reg T payment deadline (T+4), the firm will freeze a customer account for 90 days. A customer with a 90-day frozen account must deposit sufficient cash into the account before placing any new buy orders. |

| Undeliverable Mail | A broker-dealer can restrict an account by halting all trading if a customer's mail is repeatedly returned as undeliverable. |

| Relocation to Unregistered State | A broker-dealer must restrict a customer account to liquidating transactions only if the customer relocates to a state where the broker-dealer is not registered. |

| Missing Options Agreement | An options customer must return a signed options agreement within 15 days of the options account approval. If they fail to do so, the firm will restrict an options account to closing transactions only. |

| Pattern Day Trader Margin Call | A broker-dealer will restrict a pattern day trader's account to cash-available trading if the account equity falls below $25,000. |

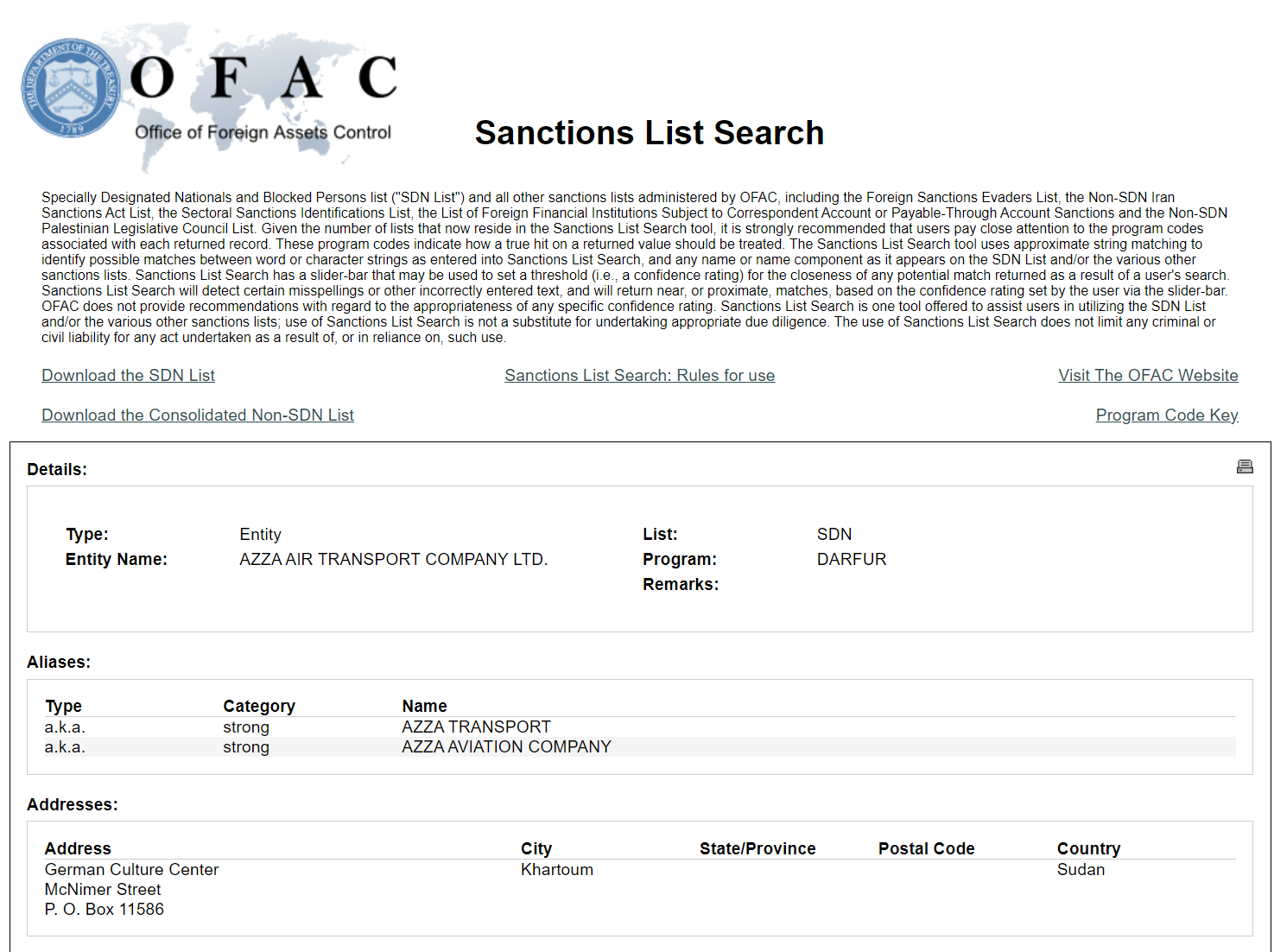

| OFAC / Sanctions | A broker-dealer must block all transactions for a customer account if the customer is identified on the federal Specially Designated Nationals (SDN) list. |

The Finality of Death

When a client passes away, the legal authority governing the account vanishes instantly. A broker-dealer must freeze a customer account immediately upon receiving formal notification of the customer's death. Furthermore, the firm must cancel all open orders in a customer account immediately upon receiving this notification. Crucially, a customer's death immediately revokes any power of attorney (POA) previously granted on the deceased customer's account. The account can only be unfrozen once the proper legal estate documents are provided.

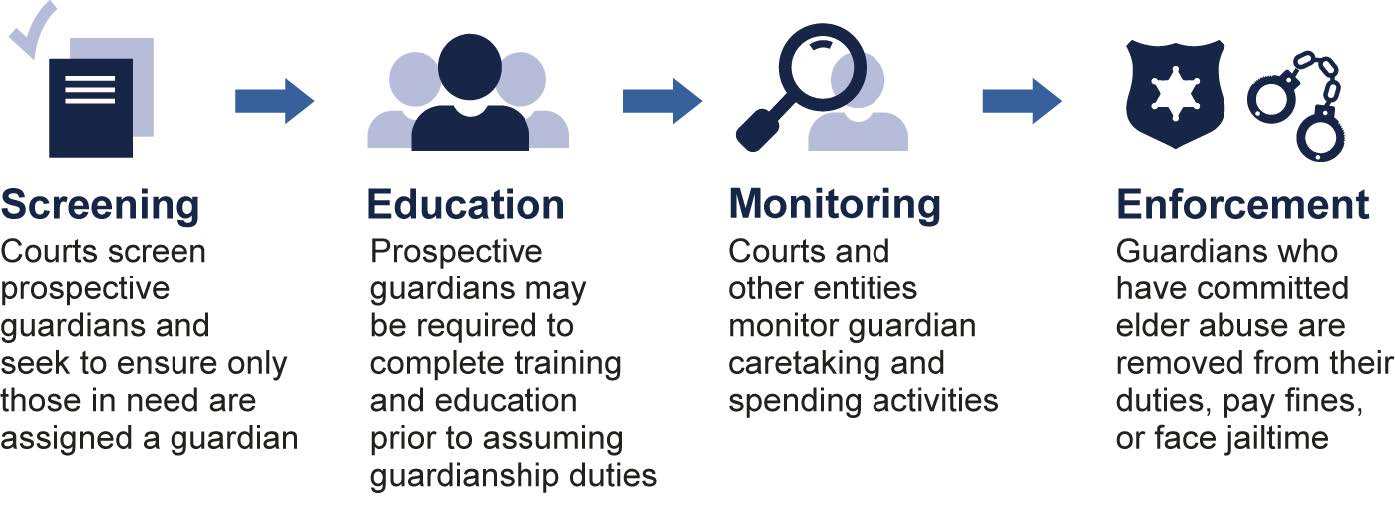

Protecting the Vulnerable: FINRA Rule 2165

Financial exploitation of the elderly and vulnerable is a severe threat. FINRA Rule 2165 gives broker-dealers a powerful tool to halt suspected theft. This rule requires a reasonable belief of financial exploitation of a specified adult (generally those 65 and older, or 18 and older with physical/mental impairments).

If a firm suspects exploitation, FINRA Rule 2165 permits a broker-dealer to place a temporary hold on a disbursement of funds, a disbursement of securities, or on securities transactions within the account of a specified adult.

The timeline for this hold is highly structured to allow for an investigation:

- An initial temporary hold due to suspected financial exploitation lasts for a maximum of 15 business days.

- A broker-dealer can extend an initial temporary hold by an additional 10 business days following an internal review.

- A broker-dealer can extend a temporary hold by an additional 30 business days if the firm reports the suspected financial exploitation to a state regulator.

- Alternatively, the firm can extend a temporary hold by an additional 30 business days if the firm reports the suspected financial exploitation to a court of law.

The Mechanics of Exit: ACATS and Account Closure

When a customer decides to leave a firm and move their assets elsewhere, the industry uses the Automated Customer Account Transfer Service (ACATS). The timeline is tight to prevent firms from holding a client's assets hostage:

- A carrying broker-dealer has one business day to validate transfer instructions under the Automated Customer Account Transfer Service.

- A carrying broker-dealer has three business days to complete an account transfer after validating the instructions.

Finally, what happens when a client simply wants to close their account entirely? A broker-dealer must close a customer account upon receiving explicit written instructions from the customer. As their representative, you may want to save the relationship, but you have no authority to block the exit. A registered representative cannot prevent a broker-dealer from closing a customer account upon the customer's request.

By mastering these rules, you do more than pass a regulatory exam. You become a reliable operator within the complex machinery of the financial system, ensuring that capital is preserved, risk is managed, and the integrity of the market remains intact.