Customer Account Types and Characteristics

A brokerage account is not merely a digital vault; it is the structural framework that dictates the exact physical laws governing an investor’s capital. Just as the rules of aerodynamics determine what an aircraft can and cannot do in the sky, the type of account an investor opens determines their access to leverage, their exposure to risk, and their tax liabilities. As a future registered representative, you are the navigator. You must understand how these accounts function, not just as abstract regulatory constructs, but as the daily mechanical tools you will use to execute trades, protect your clients, and safeguard the financial system.

When a client wants to buy a security, the most fundamental question is: whose money are they using? The answer to that question divides the brokerage world into two primary camps.

The Cash Account

A cash account is the simplest form of brokerage relationship. The rule here is absolute: a cash account requires the customer to pay in full for all purchased securities. Customers cannot purchase securities using borrowed funds in a cash account.

Because the risk is strictly limited to the customer's own capital, regulators mandate this account type for specific, vulnerable, or tax-advantaged situations. Individual retirement accounts (IRAs) must be opened as cash accounts. Similarly, because minors cannot legally enter into binding credit contracts, a cash account is the only brokerage account type approved for minors.

The Margin Account

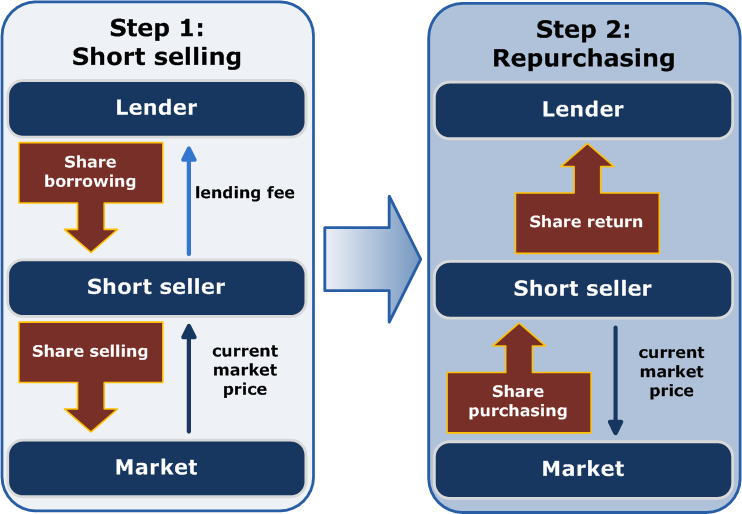

If a cash account is like buying a house in cash, a margin account is like taking out a mortgage. A margin account allows a customer to borrow money from a broker-dealer to purchase securities. Naturally, the broker-dealer is not handing out free money. Securities purchased in a margin account serve as collateral for the loan from the broker-dealer.

Because margin amplifies both gains and losses, regulators and broker-dealers tightly control it. For instance, broker-dealers require customers to use a margin account to execute short sales, because selling something you do not own carries mathematically infinite risk.

Before a customer can borrow a single cent, a margin account requires the customer to sign a margin agreement. This document has three distinct parts:

- The Credit Agreement: This details the mathematical reality of the loan, explicitly stating the terms of the loan and interest rates.

- The Hypothecation Agreement: This is a mandatory mechanism allowing the broker-dealer to pledge customer securities as collateral for a bank loan. The broker-dealer borrows from a bank to lend to the client; hypothecation is the legal chain linking the client's stock to the bank's money.

- The Loan Consent Form: This is an optional agreement allowing the broker-dealer to lend the customer's securities to other investors (often those looking to short the stock).

The Mathematics of Margin

The rules of margin are governed by two distinct regulatory layers: the initial purchase and the ongoing maintenance.

Federal Reserve Board Regulation T: This establishes an initial margin requirement of 50 percent for purchasing most equity securities. If a client wants to buy $10,000 of stock on margin, Regulation T dictates they must deposit at least $5,000 of their own money.

FINRA Maintenance Rules: Once the stock is purchased, the market will fluctuate. The Financial Industry Regulatory Authority requires a minimum maintenance margin of 25 percent of the long market value in a margin account.

If the value of the securities drops so severely that the client's equity falls below that 25 percent threshold, the system triggers a margin call. A margin call occurs when the equity in a margin account falls below the required maintenance margin level, forcing the client to deposit more cash or securities immediately.

Options are derivative contracts. They are incredibly powerful, allowing investors to hedge portfolios or speculatively leverage capital. Because options can expire completely worthless, the regulatory framework treats them like financial fire.

You cannot simply wake up and trade options in a standard account. An options account requires specific approval from a Registered Options Principal (ROP) before trading can begin. The ROP acts as the gatekeeper, verifying that the client has the financial wherewithal and investment knowledge to handle derivative risks.

The Paperwork Sequence

The timeline for opening an options account is highly testable and strictly enforced:

- Disclosure: A broker-dealer must provide the customer with an Options Disclosure Document (ODD) at or before the approval of an options account. This booklet explains the sheer physics of options trading and its risks.

- Approval: The ROP approves the account.

- The 15-Day Clock: The customer can begin trading, but they must sign and return an options agreement within 15 days of the options account approval. The options agreement verifies that the customer has read the Options Disclosure Document.

- The Penalty: Failing to return the signed options agreement within 15 days restricts the customer to closing existing options positions. They cannot open any new positions until the paperwork is secured.

Account Constraints on Options

The strategy dictates the account type. Customers can execute basic options strategies like covered calls in a cash account, because the risk is "covered" by the stock they already own fully. However, writing "naked" (uncovered) options exposes the investor to massive potential losses. Therefore, customers must utilize a margin account to execute naked options writing strategies.

As a registered representative, your relationship with your client's capital hinges on who is making the decisions.

Non-Discretionary Accounts

In a standard non-discretionary account, the client is the pilot; you are the navigator. The customer must approve the specific transaction action (buy or sell) before trade execution. The customer must approve the specific security (e.g., Apple vs. Microsoft) before trade execution. The customer must approve the specific quantity of shares (e.g., 100 shares) before trade execution.

If you are missing any of those three elements—Action, Asset, or Amount—you cannot execute the trade.

There is one important exception: Time and Price Discretion. A registered representative can choose the time of execution in a non-discretionary account without formal discretionary authority. Similarly, a registered representative can choose the price of execution. However, time and price discretion granted by a customer is only valid until the end of the trading day on which the customer granted the discretion. If the sun sets and the market closes, your authority evaporates.

Discretionary Accounts

A discretionary account shifts the locus of control. It allows a registered representative to make investment decisions for a customer without prior consultation.

Discretionary authority permits a registered representative to determine whether to buy or sell a security, choose the specific security to trade, and determine the number of shares to trade.

Because handing over the keys to one's life savings is an enormous leap of faith, FINRA requires a heavy trail of authorization:

- A discretionary account requires the customer to provide written authorization through a power of attorney (POA).

- A principal of the broker-dealer must approve a discretionary account in writing prior to the first discretionary trade.

- To prevent abuse (such as churning an account just to generate commissions), a principal must frequently review all trading activity in a discretionary account.

How you charge your clients fundamentally changes the nature of the brokerage relationship and must align with the client's actual behavior.

| Account Type | How It Works | Target Investor |

|---|---|---|

| Commission-Based | Charges the customer a specific fee for each executed transaction. | Generally suitable for buy-and-hold investors who execute few transactions. |

| Fee-Based | Charges the customer a set fee or a percentage of assets under management. It does not charge the customer per-transaction trading commissions. | Generally suitable for investors who engage in frequent trading activity. |

| Wrap Account | Bundles investment advice, brokerage services, and administrative costs into a single fee. | Investors seeking holistic wealth management without transaction friction. |

Why this matters: Regulators strictly enforce the concept of appropriateness. Broker-dealers must ensure that a fee-based account is appropriate for the customer based on the anticipated trading volume of the customer. Putting a buy-and-hold investor in a fee-based account is a regulatory violation known as "reverse churning"—you are charging them a perpetual fee when a single commission would have been vastly cheaper.

Finally, we look at specialized accounts designed for a very specific real-world problem: the exponential cost of education. The industry utilizes two primary tax-advantaged vehicles, each with precise constraints.

The 529 College Savings Plan

A 529 College Savings Plan is uniquely categorized as a state-sponsored municipal fund security designed to save for future education costs.

- Funding: Contributions to a 529 College Savings Plan are made with after-tax dollars.

- Benefits: The capital grows tax-deferred, and withdrawals from a 529 College Savings Plan are tax-free at the federal level if used for qualified education expenses.

- Flexibility: Section 529 plans allow up to $10,000 per year to be withdrawn tax-free for K-12 tuition expenses. Furthermore, if the original child decides not to go to college, the capital is not trapped. Section 529 plans allow funds to be transferred to an eligible family member of the original beneficiary without tax penalties.

The Coverdell Education Savings Account (ESA)

The Coverdell ESA is an alternative with much stricter caps but broader investment choices. Like the 529, a Coverdell Education Savings Account allows after-tax contributions to fund qualified education expenses, meaning contributions to a Coverdell Education Savings Account are not tax-deductible. And just like the 529, withdrawals from a Coverdell Education Savings Account are tax-free if used for qualified education expenses.

However, the Coverdell ESA imposes rigid constraints that you must memorize:

- Contribution Limits: The maximum annual contribution to a Coverdell Education Savings Account is strictly limited to $2,000 per beneficiary.

- Age Limits: Coverdell Education Savings Account contributions must cease when the beneficiary reaches age 18. Furthermore, Coverdell Education Savings Account funds must be used or rolled over by the time the beneficiary reaches age 30.

Understanding these accounts transforms you from an order-taker into a true professional. Every time a client sits across your desk, you are leveraging these mechanical rules—margin rules, discretionary power, tax advantages—to bend the physics of the financial world to their benefit. Know these rules cold.