Economic Factors and the Federal Reserve

Imagine a massive, continuously running engine powering the financial well-being of hundreds of millions of people. This engine is the United States economy, and it does not operate in a vacuum. It requires constant tuning to prevent it from running too hot and destroying its internal components through hyperinflation, or running too cold and stalling out entirely. In the financial markets, as a registered representative, your daily reality—from the prices of the bonds you trade, to the margin rates your clients pay, to the performance of the equity portfolios you oversee—is dictated by the mechanics of this engine. Understanding these mechanics is not merely an academic exercise; it is the absolute foundation of market literacy. The tuning of this economic engine is accomplished through two distinct but deeply interconnected control systems: the allocation of government capital and the manipulation of the money supply.

When we want to change the speed or direction of the economy, we pull one of two major levers. These levers operate on entirely different principles and are controlled by entirely different groups of people.

Fiscal Policy

Fiscal policy involves government spending and taxation policies designed to influence the economy. When the government builds a highway, awards a defense contract, or cuts income taxes, it is executing fiscal policy. Because it involves the national budget, fiscal policy is determined jointly by the President of the United States and the United States Congress.

This approach is the cornerstone of Keynesian economic theory. Named after economist John Maynard Keynes, this theory advocates for active government intervention through fiscal policy to stimulate demand. If the private sector is not spending enough to keep the economy moving, the Keynesian view argues that the government must step in—acting as the spender of last resort—to prime the pump.

Monetary Policy

If fiscal policy is about how much money the government is spending, monetary policy is about the fundamental availability and cost of the money itself. Monetary policy consists of actions taken by the Federal Reserve Board to influence the money supply. Unlike fiscal policy, which is tangled in partisan politics, monetary policy is determined exclusively by the Federal Reserve Board (the Fed).

The reliance on central bank control is the foundation of Monetarist economic theory. Monetarists argue that the money supply is the primary determinant of price levels and economic activity. From this perspective, the amount of cash circulating in the system is the ultimate driver of whether businesses expand or contract.

To execute monetary policy, the Federal Reserve acts as the ultimate plumber of the financial system, managing the flow of capital through several powerful tools.

Open Market Operations (The Primary Tool)

The most frequently used tool is open market operations, which refer to the Federal Reserve buying and selling United States government securities in the secondary market. The Federal Open Market Committee (FOMC) directs open market operations for the Federal Reserve.

To understand how this works, imagine the banking system as a sponge.

- Expansionary Monetary Policy: When the Federal Reserve buys securities in the open market from banks, it takes those paper securities and hands the banks cold, hard cash in return. The Federal Reserve injects money into the banking system. An injection of money into the banking system increases the money supply. Supply and demand dictates that when something is abundant, its price drops. Because interest rates are simply the "price" of borrowing money, an increase in the money supply generally leads to lower interest rates. Increasing the money supply through the purchase of securities is an expansionary monetary policy, designed to stimulate economic growth.

- Contractionary Monetary Policy: Conversely, when the Federal Reserve sells securities in the open market to banks, it hands them paper securities and takes their cash. The Federal Reserve withdraws money from the banking system, which decreases the money supply. A decrease in the money supply makes cash scarce, which generally leads to higher interest rates. Decreasing the money supply through the sale of securities is a contractionary monetary policy, typically used to combat inflation.

Memory Aid: Buying securities makes the money supply Bigger. Selling securities makes the money supply Smaller.

The Reserve Requirement

Banks do not keep all of their customers' deposits in the vault; they lend them out to generate interest. However, they are bound by the reserve requirement, which is the percentage of customer deposits that banks must hold in cash or on deposit with the Federal Reserve.

- Lowering the reserve requirement increases the amount of money banks are permitted to lend out, flooding the market with credit.

- Raising the reserve requirement decreases the amount of money banks are permitted to lend out, tightening the credit market.

Because banks lend money to people who then deposit it in other banks—which then lend a portion of that money out again—we see a multiplier effect. The multiplier effect causes small changes in the reserve requirement to have a magnified impact on the overall money supply. Because of this drastic ripple effect, the Fed rarely changes the reserve requirement.

Margin Lending Rules

The Fed also controls the flow of credit directly into the stock market. Regulation T is a Federal Reserve Board rule governing the initial margin requirement for securities purchases (currently set at 50%). If the Fed wants to cool down speculative market trading, it can raise the Regulation T requirement.

When you alter the money supply, you alter interest rates. But "interest rates" is a plural term. There is a very specific hierarchy of rates in the financial system, flowing from the central bank down to the retail consumer.

| Interest Rate | Definition | Characteristics |

|---|---|---|

| Federal Funds Rate | The interest rate that commercial banks charge each other for overnight loans. | The federal funds rate is considered the most volatile of all short-term interest rates. The Federal Reserve sets a target range for it, but the actual federal funds rate is determined by market forces rather than direct Federal Reserve mandates. It is typically the lowest of the four major interest rates. |

| Discount Rate | The interest rate charged by the Federal Reserve to commercial banks for short-term loans. | The discount rate is the only major interest rate directly set by the Federal Reserve. It serves as a safety valve for banks that cannot borrow from each other. |

| Broker Call Loan Rate | The interest rate that banks charge broker-dealers for money borrowed to fund customer margin accounts. | Directly impacts you and your clients. When clients buy stock under Regulation T on margin, the broker-dealer borrows the funds from a bank at this rate, then charges the client a slightly higher rate. |

| Prime Rate | The interest rate that commercial banks charge their most creditworthy corporate customers. | This serves as the baseline for consumer credit, such as credit cards and adjustable-rate mortgages. The prime rate is typically the highest of the four major interest rates. |

The economy does not grow in a straight upward line; it breathes in and out. This breathing is known as the business cycle, which consists of four distinct phases: expansion, peak, contraction, and trough.

- Expansion: An economic expansion is a period of generally increasing economic activity. It is characterized by rising gross domestic product (GDP)—the total value of goods and services produced in the country. During this phase, employment is high and consumers are spending. Because demand is strong, mild inflation is typically associated with periods of economic expansion.

- Peak: The absolute top of the expansion, where the economy maxes out its capacity before turning downward.

- Contraction: An economic contraction is a period of generally declining economic activity. It is characterized by falling gross domestic product.

- Trough: The bottom of the cycle, where the contraction halts before a new expansion begins.

Severe Contractions: Recessions and Depressions

While contractions are normal, severe ones have specific definitions:

- A recession is officially defined as two consecutive calendar quarters (six months) of declining gross domestic product.

- A depression is officially defined as six consecutive calendar quarters (18 months) of declining gross domestic product.

To know where we are in the business cycle, economists rely on specific data points called indicators. Think of them as the dashboard of the economic engine.

Economic Indicators

- Leading economic indicators predict future trends in the overall economy. They turn before the broader economy turns. The stock market index (like the S&P 500) is an example of a leading economic indicator, as investors price in future expectations. New housing starts are also an example of a leading economic indicator, because builders only pour concrete if they anticipate future demand.

- Coincident economic indicators reflect the current state of the overall economy. They change at the exact same time the economy changes. Gross domestic product is an example of a coincident economic indicator, as are industrial production levels.

- Lagging economic indicators confirm long-term trends after an economic shift has already occurred. Corporate profits are an example of a lagging economic indicator (they are reported after the quarter ends). The average duration of unemployment is another lagging economic indicator; companies hesitate to hire even after an expansion has begun, waiting to ensure the recovery is real.

Measuring the Money Supply

When we talk about the "money supply," we must be precise about what kind of money we mean. Economists divide money into tiers based on liquidity:

- M1 money supply is the most liquid. It includes physical currency in circulation and demand deposits (standard checking accounts).

- M2 money supply includes all components of M1 plus savings accounts and non-institutional money market funds. It is slightly less liquid.

- M3 money supply includes all components of M2 plus large time deposits (jumbo CDs) and institutional money market funds. This is the broadest measure.

Inflation and Deflation

The supply of money dictates the value of the currency.

- Inflation is a general increase in the prices of goods and services over time. It means your dollar buys less tomorrow than it did today. The Consumer Price Index (CPI) is the primary metric used to measure inflation in the United States economy. It tracks the cost of a "basket" of standard consumer goods.

- Deflation is a general decrease in the prices of goods and services over time. While falling prices sound great to consumers, deflation is highly destructive to an economy, as consumers stop spending in anticipation of even lower prices tomorrow, which causes businesses to fail.

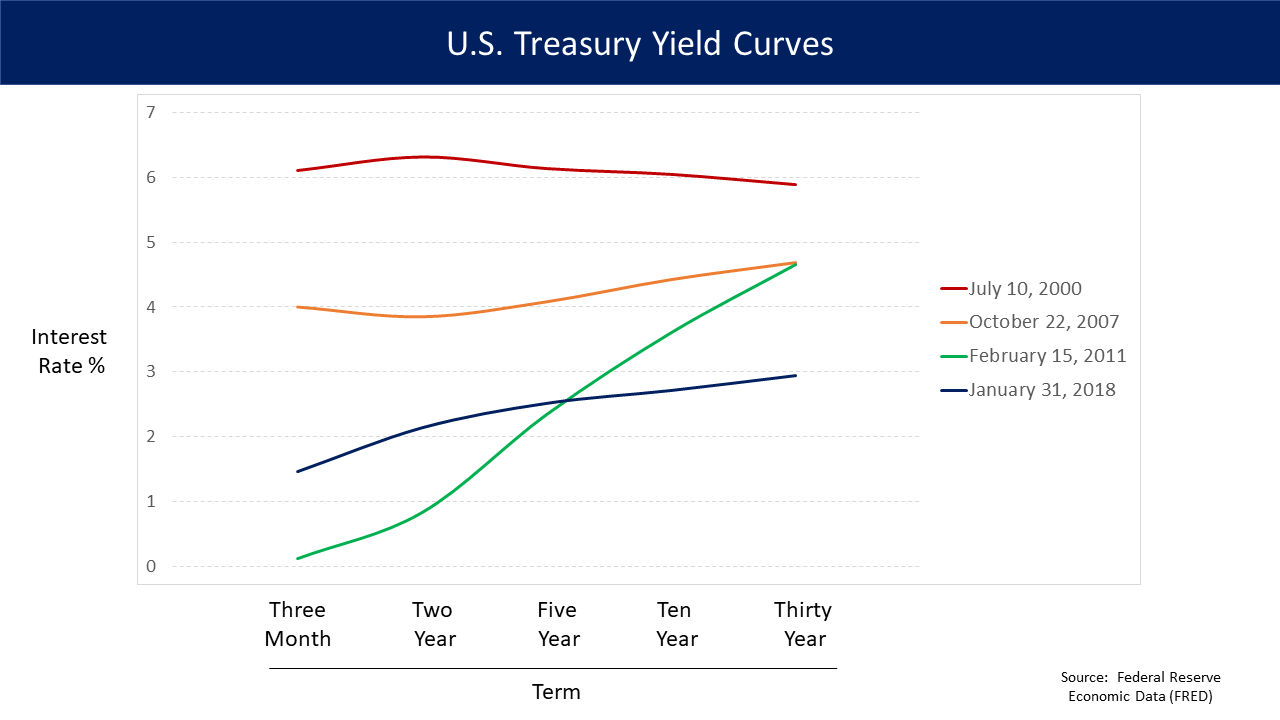

One of the most reliable predictors of the economic future is found not in stocks, but in bonds. The yield curve plots the interest rates of similar bonds (like U.S. Treasuries) across different maturity dates.

- Normal yield curve: A normal yield curve occurs when long-term debt instruments have higher yields than short-term debt instruments. This makes intuitive sense: if you lock your money up for 30 years, you demand a higher return for that risk than if you lock it up for 3 months.

- Inverted yield curve: An inverted yield curve occurs when short-term debt instruments have higher yields than long-term debt instruments. This is highly unnatural. It happens when investors rush to buy long-term bonds (driving yields down) because they expect central banks to cut rates aggressively in the near future. Therefore, an inverted yield curve is widely interpreted as an indicator of an impending economic recession.

- Flat yield curve: A flat yield curve occurs when short-term and long-term debt instruments offer approximately the same yields. This usually represents a transition phase between a normal and an inverted curve.

Finally, the U.S. economic engine connects to the rest of the world through the exchange rate of the U.S. dollar. The relative value of the dollar drastically alters the profitability of multinational corporations, which in turn impacts the stock market.

- Strong Dollar: A strong United States dollar makes imported goods cheaper for domestic consumers (your dollars buy more European wine or Japanese electronics). However, it hurts U.S. manufacturers, because a strong United States dollar makes exported goods more expensive for foreign buyers.

- Weak Dollar: Conversely, a weak United States dollar makes imported goods more expensive for domestic consumers. But it is a massive advantage for U.S. manufacturers, as a weak United States dollar makes exported goods cheaper for foreign buyers, driving up global sales of U.S. products.