Hedge Funds and ETPs

Imagine the financial markets as a vast transportation network. Traditional mutual funds are the reliable, heavily regulated public transit system, carrying millions of retail passengers along predetermined, highly transparent routes. But what if an investor wants a private jet, capable of aggressive maneuvers and unconstrained by standard flight paths? Or perhaps they want a highly efficient, self-driving car that they can hop in and out of at any second of the day? These alternatives exist, but they operate under completely different engineering principles and safety regulations. To advise clients effectively—and to pass the FINRA SIE—you must look under the hood of these specialized vehicles.

We are going to dissect two distinct corners of the market: hedge funds, which offer private, unconstrained strategies for the wealthy, and Exchange-Traded Products (ETPs), which democratize market access by allowing both broad indexes and niche asset classes to be traded dynamically throughout the day.

If a portfolio manager wants the freedom to trade anything, anytime, and use aggressive tactics to generate massive returns, they cannot register their fund under the strict rules of the Investment Company Act of 1940. The 1940 Act severely restricts how much debt a mutual fund can take on and how it can trade.

To escape these constraints, hedge funds are purposefully constructed to be exempt from registration under the Investment Company Act of 1940. By giving up the regulatory "seal of approval," the fund buys its freedom. But federal law demands a trade-off: if you are going to operate an unregulated, high-risk fund, you cannot sell it to the general public.

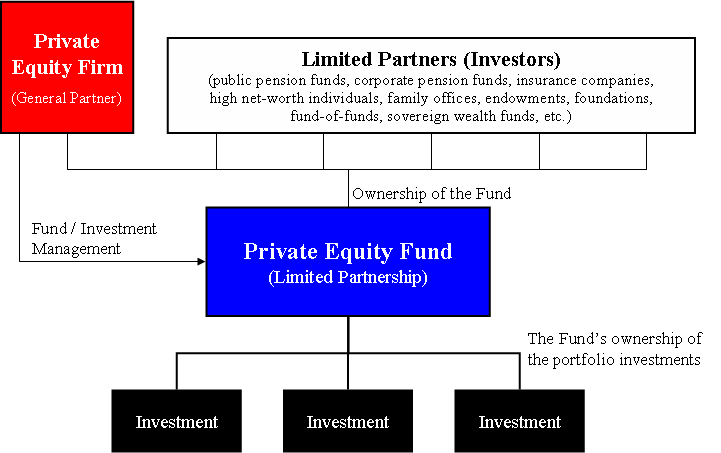

Structure and Private Equity Nature

Because they cannot be offered to the public, hedge funds issue securities through private placements under Regulation D. They operate as private pools of capital, sharing much of the same legal DNA as private equity funds.

To optimize tax efficiency and limit liability, hedge funds are typically structured as limited partnerships.

- The hedge fund manager serves as the general partner of the limited partnership. They make all the trading decisions and take on the legal liability of running the fund.

- Investors in a hedge fund serve as the limited partners. They simply provide the capital. Their liability is limited to exactly what they invest.

Who Gets to Invest?

Because these private placements lack the regulatory protections of traditional mutual funds, they are typically restricted to accredited investors or qualified purchasers.

Accredited Investor Definition (FINRA Crucial) Under SEC rules, an individual qualifies as an accredited investor if they meet either of these financial tests:

- An annual income exceeding $200,000 in each of the two most recent years (or $300,000 jointly with a spouse), with a reasonable expectation of reaching the same income level in the current year.

- A net worth exceeding $1 million, excluding the primary residence.

Furthermore, to ensure they only attract serious, well-capitalized participants, hedge funds require significantly higher minimum initial investments compared to retail mutual funds. While a mutual fund might let you start with $500, a hedge fund might require a minimum check of $500,000 or $1 million.

Aggressive Strategies and Premium Fees

Once a hedge fund has secured this private capital, what do they do with it? Without the constraints of the 1940 Act, hedge funds frequently employ aggressive strategies to hunt for high returns:

- They frequently employ leverage (borrowed money) to magnify returns.

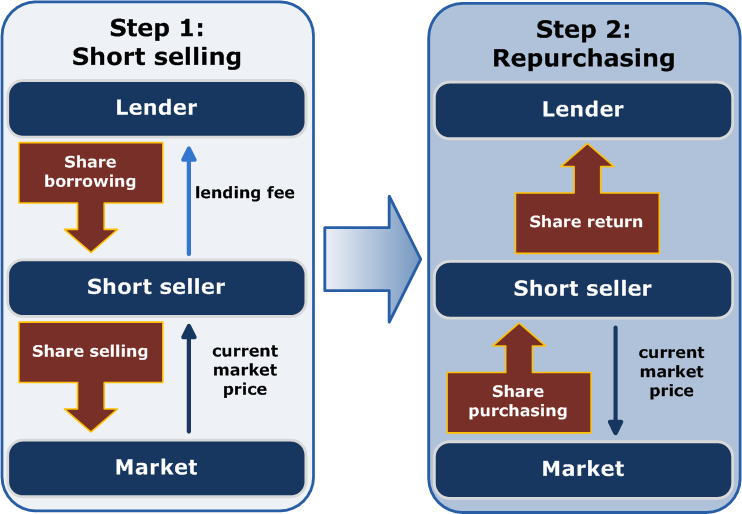

- They engage in short selling to profit from declining asset prices.

- They frequently trade derivatives (like options and futures) to speculate on market movements or precisely hedge their risks.

To manage this complex machinery, hedge fund managers demand a premium. They typically utilize a "two and twenty" fee structure:

- They commonly charge a two percent (2%) annual management fee based on the total assets under management, just for keeping the lights on.

- They commonly charge a twenty percent (20%) performance fee based on generated profits, incentivizing the manager (the general partner) to achieve aggressive growth.

The Cost of Freedom: Extreme Illiquidity

There is a major catch for the investor (the limited partner). If you invest in a hedge fund, your money is effectively trapped.

Hedge funds are highly illiquid investments. Because they are private placements under Reg D, hedge fund shares do not trade on public secondary markets. You cannot simply open a brokerage app and sell your hedge fund shares to someone else.

To ensure the manager has time to execute their complex, long-term strategies without worrying about a "run on the bank," hedge funds typically impose lock-up periods.

Lock-Up Period A lock-up period prohibits investors from withdrawing capital for a specified duration after the initial investment.

Even after the lock-up period expires, investors typically cannot withdraw funds on demand; they usually must provide advance notice (e.g., 30 to 90 days) and can only withdraw capital during specific "windows" (like at the end of a quarter).

Now, let's step out of the private, illiquid world of the ultra-wealthy and look at an innovation built for the public secondary market: Exchange-Traded Products (ETPs).

Exchange-Traded Products are securities that track an underlying security, index, or financial instrument. Think of ETP as the umbrella term for a family of financial vehicles. The unifying feature of all ETPs is right in the name: Exchange-Traded Products trade on national securities exchanges.

Unlike traditional mutual funds—which only calculate their Net Asset Value (NAV) once a day at the 4:00 PM market close—ETPs act like individual stocks. Because they trade on an exchange, investors typically pay brokerage commissions when buying Exchange-Traded Product shares, and similarly, investors typically pay brokerage commissions when selling Exchange-Traded Product shares.

Under this ETP umbrella, there are two distinct siblings you must know for the SIE exam: ETFs and ETNs. They sound similar, but they are engineered completely differently.

Exchange-Traded Funds (ETFs): The Liquid Portfolio

An Exchange-Traded Fund (ETF) is a portfolio of actual assets. Unlike a hedge fund, Exchange-Traded Funds are legally classified under the Investment Company Act of 1940.

Structurally, an Exchange-Traded Fund can be structured as an open-end management investment company, or, less commonly today, an Exchange-Traded Fund can be structured as a unit investment trust (UIT).

Trading Mechanics

The magic of the ETF is its liquidity. Exchange-Traded Funds issue shares that trade continuously in the secondary market throughout the trading day. This means investors can buy and sell Exchange-Traded Fund shares at fluctuating market prices intraday. If news breaks at 11:00 AM, you can sell your ETF at 11:01 AM. You don't have to wait for the end-of-day mutual fund pricing.

Because they trade exactly like stocks, they possess the same aggressive trading capabilities:

- Exchange-Traded Fund shares can be purchased on margin (using borrowed money from a broker).

- Investors can short sell Exchange-Traded Fund shares if they believe the tracked index or sector will decline.

Management: Passive vs. Active

When you buy an ETF, who decides what goes inside the portfolio?

Most Exchange-Traded Funds are passively managed. What does that mean? Passively managed Exchange-Traded Funds attempt to replicate the performance of a specific index (like the S&P 500 or the Nasdaq 100). There is no high-paid manager trying to guess which stock will go up; a computer simply buys the exact stocks in the index.

However, there is a growing subset of the market that operates differently: Actively managed Exchange-Traded Funds employ portfolio managers to select securities to outperform a benchmark.

When comparing the two, fees are the critical differentiator:

- Because passive funds don't require expensive human analysts, passively managed Exchange-Traded Funds generally have lower expense ratios than actively managed funds.

- Furthermore, because ETF shares are traded between investors on the secondary market rather than being redeemed directly with the fund company, Exchange-Traded Funds generally have lower operating costs compared to traditional mutual funds.

Risk Profile

When you own an ETF, you own a proportional slice of the underlying basket of stocks or bonds. Therefore, Exchange-Traded Funds expose investors primarily to the market risk of the underlying portfolio. If the underlying stocks drop in value, your ETF drops in value.

Exchange-Traded Notes (ETNs): The Unsecured Promise

Now we turn to the ETF's strange cousin: the Exchange-Traded Note (ETN).

Imagine you want to track a highly obscure index—perhaps the price of a specific foreign currency combined with an exotic commodity. An investment bank looks at this and says, "It is too difficult and expensive for us to actually buy and store those underlying assets to create an ETF. Instead, we will just promise to pay you whatever that index returns."

That is an ETN. Exchange-Traded Notes do not own a portfolio of underlying assets.

Instead, Exchange-Traded Notes are unsecured debt obligations issued by financial institutions (like a major commercial bank). Exchange-Traded Notes promise to pay a return linked to the performance of a specific market index. Because it is fundamentally a debt instrument, Exchange-Traded Notes have a stated maturity date (often 10 to 30 years out), at which point the issuer calculates the final value of the index and pays the investor.

Trading and Risks

Just like ETFs, Exchange-Traded Notes trade on stock exchanges throughout the day, making them highly liquid.

However, the risk profile of an ETN is uniquely dangerous. With an ETN, you face two distinct types of risk:

- Exchange-Traded Notes expose investors to market risk. Just like an ETF, if the index it tracks goes down, the value of your ETN goes down.

- Exchange-Traded Notes expose investors to the credit risk of the issuing financial institution.

This second point is heavily tested on the SIE. Because an ETN is essentially an IOU from a bank, its value depends entirely on the bank's ability to pay. If the issuer of an Exchange-Traded Note defaults, the investor might lose the entire principal, even if the underlying index it was tracking actually went up! There are no underlying assets to liquidate and give back to you. You are simply an unsecured creditor of a bankrupt institution.

To solidify your baseline knowledge for the exam, use this master table to keep these three unique products distinct in your mind:

| Feature | Hedge Funds | ETFs | ETNs |

|---|---|---|---|

| Regulation | Exempt from Investment Company Act of 1940 (Reg D Private Placements). | Classified under Investment Company Act of 1940. | Registered under the Securities Act of 1933 (Debt instruments). |

| Structure | Limited Partnership (Manager = GP; Investors = LPs). | Open-end management company or Unit Investment Trust (UIT). | Unsecured debt obligation of a financial institution. |

| Underlying Assets | Yes, holds a highly aggressive, actively traded portfolio. | Yes, holds a portfolio of securities (mostly passively managed). | No. Does not own an underlying portfolio; simply promises a return. |

| Liquidity | Highly illiquid. No secondary market. Lock-up periods apply. | Highly liquid. Trades continuously intraday on secondary markets. | Highly liquid. Trades continuously intraday on secondary markets. |

| Access | Restricted to Accredited Investors / Qualified Purchasers. High minimums. | Open to the public. Can buy a single share. | Open to the public. Can buy a single share. |

| Primary Risks | Severe market risk, illiquidity risk, leverage/derivative risk. | Market risk of the underlying portfolio. | Market risk PLUS Credit risk of the issuing bank. |

| Fees / Costs | High: 2% management fee + 20% performance fee. | Low: Lower operating costs than mutual funds. Brokerage commissions apply. | Low: Expense ratios apply. Brokerage commissions apply. |

By understanding why hedge funds trade liquidity for regulatory freedom, and why an ETN carries credit risk while an ETF does not, you shift from memorizing facts to mastering market mechanics. Keep these structural differences in focus, and you will navigate these FINRA SIE concepts with absolute precision.