Options Strategies and Settlement

Imagine purchasing a million-dollar commercial property with a fraction of its total cost, yet reaping the full financial benefit if its market value doubles. Alternatively, imagine buying a specialized insurance policy that guarantees you can sell your current home at today’s exact appraisal price, even if the local real estate market completely collapses tomorrow. This is the structural power of the options market. For a securities professional, options are not merely theoretical abstractions or casino chips; they are the fundamental mechanics of risk transfer. They allow investors to manipulate market exposure, amplify returns, and build impenetrable firewalls around their capital. Mastering these derivatives is not just about passing an exam—it is essential for anyone responsible for safeguarding client assets, executing complex market strategies, and understanding the true physics of financial markets.

Every participant in the options market is fundamentally doing one of two things: attempting to shed risk, or attempting to take it on for a profit.

Hedging is the practice of using options to protect an existing investment position from adverse price movements. Think of it as buying insurance. If a client owns thousands of shares of a technology company, a sudden earnings miss could wipe out years of gains. Hedging acts as a shock absorber.

Conversely, speculation is the practice of using options to bet on the directional price movement of an underlying asset. Speculators provide the liquidity that hedgers need. Rather than tying up massive amounts of capital buying stock directly, options provide speculative leverage by allowing an investor to control one hundred shares of an underlying stock with a single contract. A speculator might pay a $500 premium to control $15,000 worth of stock, amplifying their potential percentage returns—and their potential losses.

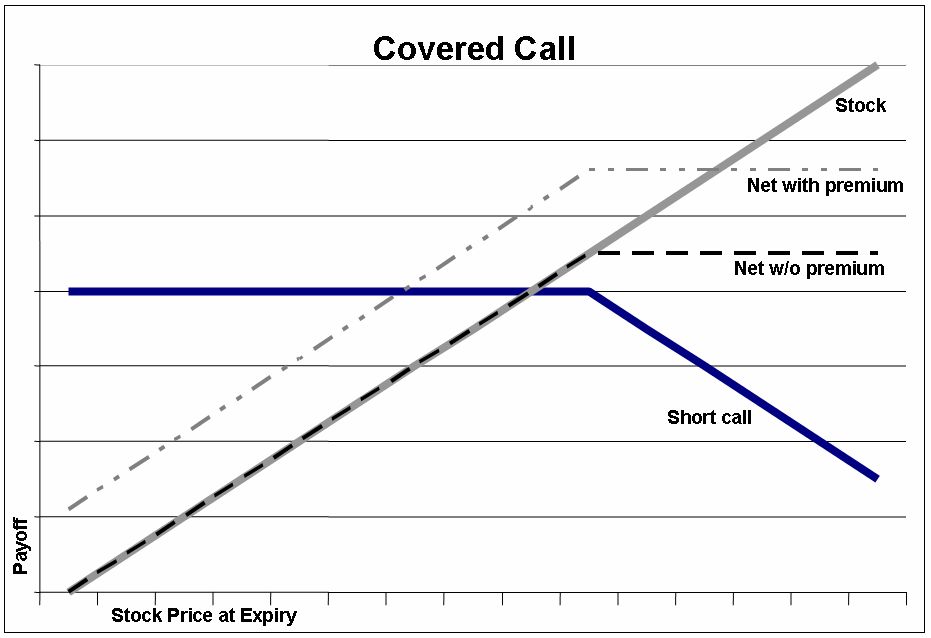

Strategic Applications: Covered and Uncovered Positions

To understand how professionals deploy these tools, we must look at the relationship between the option contract and the underlying asset.

When an investor owns the underlying asset and uses options to protect it, they are engaging in a protective put. A protective put is a hedging strategy involving the purchase of a put option while owning the underlying stock. Just as a homeowner buys fire insurance, a protective put protects a long stock position against a decline in market value. If the stock crashes, the investor simply exercises the put to sell the stock at the guaranteed strike price.

But what if a client wants to generate additional yield on a stagnant portfolio? They might use a covered call. A covered call is an income-generating strategy involving the sale of a call option while simultaneously owning the underlying stock. By selling the call, the investor collects a premium upfront. However, there is a trade-off: a covered call caps the maximum upside profit potential of the underlying stock. If the stock skyrockets, the shares will be called away at the strike price, and the investor forfeits any gains beyond that point. Similarly, on the bearish side, a covered put strategy involves writing a put option while maintaining a short position in the underlying stock.

When an investor writes (sells) an option without owning the protective asset, they step into much riskier territory.

Uncovered Strategy: An uncovered option strategy involves writing an option contract without owning the underlying asset. Because the writer is exposed to the open market if forced to fulfill the contract, an uncovered option writer must deposit margin to initiate the position.

The risks here are asymmetric. For instance, writing an uncovered call option carries unlimited maximum risk. Why? Because there is no mathematical ceiling on how high a stock's price can go. If a stock surges from $50 to $5,000, the uncovered call writer is legally obligated to buy shares at $5,000 in the open market and deliver them at the $50 strike price.

A slightly different dynamic exists for puts. A cash-secured put requires the writer to hold enough cash in the brokerage account to purchase the underlying stock upon assignment. While not "covered" by a short stock position, it is secured by liquid capital, ensuring the writer can instantly fulfill their obligation if the put buyer decides to exercise.

To determine whether an option has immediate, tangible value, we measure its "moneyness"—the relationship between the current market price of the underlying asset and the contract's strike price.

An option only possesses actual, built-in value—known as intrinsic value—when the option is in-the-money. Time value may fluctuate, but intrinsic value is pure mathematical reality.

| Moneyness Status | Call Option (Right to Buy) | Put Option (Right to Sell) | Intrinsic Value? |

|---|---|---|---|

| In-the-Money (ITM) | Market Price > Strike Price | Market Price < Strike Price | Yes. |

| Out-of-the-Money (OTM) | Market Price < Strike Price | Market Price > Strike Price | Zero. |

| At-the-Money (ATM) | Market Price = Strike Price | Market Price = Strike Price | Zero. |

A call option is in-the-money when the market price of the underlying asset is higher than the strike price (you can buy below market value). A put option is in-the-money when the market price is lower than the strike price (you can sell above market value).

Conversely, a call option is out-of-the-money when the market price of the underlying asset is below the strike price, and a put option is out-of-the-money when the market price is above the strike price. Both out-of-the-money options have zero intrinsic value, as exercising them would result in an immediate financial loss compared to just trading in the open market.

Finally, an option is at-the-money when the market price of the underlying asset exactly equals the strike price. Like OTM options, at-the-money options have zero intrinsic value.

When an option buyer decides to use their contractual right, they initiate an exercise. Exercise is the action taken by the option buyer to invoke the rights of the option contract.

When a buyer exercises, someone on the other side of the trade must fulfill the obligation. This is called assignment. Assignment is the process where an option writer is selected to fulfill the obligations of the option contract.

Because there are millions of contracts, this process must be rigorously fair:

- First, the Options Clearing Corporation (OCC) assigns exercise notices to clearing member firms on a random basis.

- Next, those broker-dealers assign option exercise notices to their customers using a random basis or a First-In-First-Out (FIFO) method.

Exercise Styles: American vs. European

Not all options can be exercised at the buyer's whim. The "style" of the option dictates the timeline.

- American-style options can be exercised by the buyer at any time prior to the expiration date. In the financial markets, almost all equity options traded in the United States are American-style options. If you own a call on Apple or Tesla, you can exercise it on a random Tuesday a month before it expires if it suits your strategy.

- European-style options can only be exercised by the buyer on the expiration date itself. Broad-based index options traded in the United States are typically European-style options.

Settlement Procedures: Physical vs. Cash

When an option is exercised, how does the transaction actually settle? The method depends entirely on what the option represents.

Physical settlement requires the actual delivery of the underlying asset upon option exercise. If you exercise a call on a stock, you must receive actual shares of that stock in your account. Standard equity options use physical settlement upon exercise. For a financial professional, the critical timeline to remember is that settlement for the exercise of standard equity options occurs one business day after the exercise date (T+1).

But think about a broad-based index like the S&P 500. If you exercise an index option, it is practically impossible for the seller to deliver exact fractional shares of 500 different companies to your account. Therefore, we use cash.

Cash settlement requires the delivery of cash equivalent to the intrinsic value of the option upon exercise. Consequently, index options use cash settlement instead of physical delivery. Just like equities, settlement for the exercise of index options occurs one business day after the exercise date.

Because options carry unique risks—particularly the unlimited loss potential of uncovered calls—regulators strictly govern how broker-dealers permit customers to trade them. The cornerstone of this regulation is the Options Disclosure Document (ODD).

The ODD: Issued by the Options Clearing Corporation (OCC), the Options Disclosure Document is the official manual that outlines the risks and characteristics of trading options.

Firms cannot simply let clients start trading options because they signed a standard margin agreement. There is a precise, mandated chronological sequence for opening an options account:

- Delivery of the ODD: A broker-dealer must deliver the Options Disclosure Document to a customer at or prior to the time the customer account is approved for options trading. The client must have the rulebook before they are allowed onto the playing field.

- The 15-Day Rule: Once the account is approved and trading begins, the clock starts ticking. A customer must return a signed options agreement to the broker-dealer within fifteen days of the account approval. By signing this, the client acknowledges they have read the ODD, understand the risks, and agree to abide by OCC and broker-dealer rules.

- The Penalty: If the paperwork is delayed, the firm must halt the client's speculative activities. A customer cannot open new options positions if the signed options agreement is not returned within fifteen days of account approval. They are strictly limited to closing transactions to wind down existing risk until the signature is on file.

Options are incredible tools of financial engineering. They allow us to mold risk to our exact specifications. By understanding the distinction between hedging and speculating, mastering moneyness and exercise mechanics, and strictly adhering to OCC disclosure rules, you transition from a mere observer of the markets to a capable operator within them.