Orders and Strategies

Imagine standing on the floor of a global exchange, tasked with executing a massive equity trade for a portfolio. You face an immediate and fundamental dilemma: do you value certainty of execution, or do you value certainty of price? You cannot mathematically guarantee both at the same time. The structural rules of the securities market force you to prioritize one over the other. The language you use to communicate this priority to the market—the specific type of order you place—dictates exactly how, when, and if your trade will occur. Every subsequent concept in market mechanics, from the spread captured by market makers to the regulatory disclosures required on a trade ticket, cascades from this initial set of instructions.

When an investor decides to enter the market, they must translate their intent into a precise instruction. The market does not understand vague desires; it only understands specific order types.

The Market Order

If you demand absolute certainty that your trade will happen right now, you use a market order. A market order executes immediately at the best available current market price.

Because it demands immediate action, a market order guarantees execution of the trade. However, you pay a profound cost for this speed: a market order does not guarantee a specific execution price. In a fast-moving or thinly traded market, the price you ultimately receive may be vastly different from the price you saw on your screen when you hit "Buy."

The Limit Order

If you demand absolute certainty regarding the price you will accept, you use a limit order. A limit order sets a maximum purchase price or a minimum selling price for a trade.

- A buy limit order executes only at the specified limit price or lower (you want a bargain).

- A sell limit order executes only at the specified limit price or higher (you want a premium).

Unlike the market order, a limit order guarantees a specific execution price or better. But the tradeoff reverses: a limit order does not guarantee execution of the trade. If the stock never reaches your specified limit price, your order simply sits there, unfilled.

The Stop Order

While limit orders are about capturing favorable prices, stop orders are reactive mechanisms designed to trigger when a stock crosses a specific threshold. A stop order becomes a market order when a security trades at or past a specified stop price. It acts as a tripwire.

How you use this tripwire depends on your position in the market:

- A sell stop order is placed at a price below the current market price. Why? Investors use sell stop orders to protect profits on long positions, or conversely, investors use sell stop orders to limit losses on long positions. If the market suddenly plummets, the sell stop triggers, automatically dumping the stock to stop the bleeding.

- A buy stop order is placed at a price above the current market price. This might seem counterintuitive—why buy higher?—until you realize that investors use buy stop orders to limit losses on short positions (where a rising stock price represents an escalating loss).

Nuance: If an investor wants the tripwire of a stop order but is terrified of the unpredictable price of the resulting market order, they can use a stop-limit order. A stop-limit order becomes a limit order when a security trades at or past a specified stop price. It trips the wire, but instead of demanding immediate execution at any cost, it demands execution only within a specific price boundary.

An order without a deadline is a liability. Investors use "Time-in-Force" instructions to dictate exactly how long an order should live before the market discards it.

- A day order is the default setting. It automatically cancels at the end of the trading day if unexecuted.

- A Good-Til-Canceled (GTC) order ignores the daily closing bell. A Good-Til-Canceled order remains active in the market until the investor cancels the order, or conversely, a Good-Til-Canceled order remains active in the market until the broker executes the order.

- An Immediate-or-Cancel (IOC) order is impatient. An Immediate-or-Cancel order executes any available portion of the order immediately, and it automatically cancels any unexecuted portion of the order. If you want 1,000 shares and only 400 are available right now, you take the 400 and the remaining 600 vanish.

- A Fill-or-Kill (FOK) order is uncompromising. A Fill-or-Kill order requires the broker to execute the entire order quantity immediately. If it cannot be done instantly, a Fill-or-Kill order cancels entirely if the full quantity cannot be executed immediately.

- An All-or-None (AON) order also demands the whole pie, but it has patience. An All-or-None order requires the broker to execute the entire order quantity at once. However, unlike a FOK, an All-or-None order remains active if the entire order quantity cannot be executed immediately. It waits in the shadows until the full block of shares is available.

To understand where your execution price actually comes from, we must look at the entities providing liquidity: the Market Makers. These institutions stand ready to buy and sell securities, acting as the bridge between public buyers and sellers.

The Bid-Ask Spread

Market makers quote two prices: the Bid and the Ask.

- The bid price represents the highest price a market maker is willing to pay for a security. Consequently, a customer sells a security to a market maker at the bid price.

- The ask price represents the lowest price a market maker is willing to accept to sell a security. Therefore, a customer buys a security from a market maker at the ask price.

The bid price is always lower than the ask price. The mathematical difference between the bid price and the ask price is known as the bid-ask spread. This spread is essentially the market maker's gross profit margin for taking on the risk of providing liquidity.

Principal vs. Agency Capacities

When your firm handles your trade, it acts in one of two distinct legal capacities. The firm's capacity dictates how it behaves and how it charges you.

The Principal Capacity (The Dealer) A firm acts in a principal capacity when trading securities out of its own inventory. Think of a used car dealership: the dealer buys a car to put on their lot, and later sells it from their lot to a buyer. A firm acting in a principal capacity operates as a dealer. Because the firm is putting its own capital at risk, it does not charge a flat fee. Instead:

- A firm acting in a principal capacity charges a markup when selling securities to a customer.

- A firm acting in a principal capacity charges a markdown when buying securities from a customer.

The Agency Capacity (The Broker) A firm acts in an agency capacity when matching buyers with sellers. Think of a real estate agent: they do not buy the house themselves; they merely find a buyer for the seller. A firm acting in an agency capacity does not trade from its own inventory. A firm acting in an agency capacity operates as a broker. Because they take no inventory risk, a firm acting in an agency capacity charges a commission for executing the trade.

Trades are fundamentally expressions of belief about the future. We categorize these beliefs into two primary market sentiments.

A bullish investor expects the price of a specific security or the overall market to rise. Conversely, a bearish investor expects the price of a specific security or the overall market to fall.

Long vs. Short Positions

How you express that sentiment determines the mechanics of your position and the geometry of your risk.

An investor opens a long position by purchasing a security. A long position represents a bullish trading strategy; you buy low, hoping to sell high. The risk here is finite. The maximum potential loss on a long stock position is limited to the original investment amount. If you buy a stock for $50, the worst-case scenario is the stock goes to $0. You lose $50.

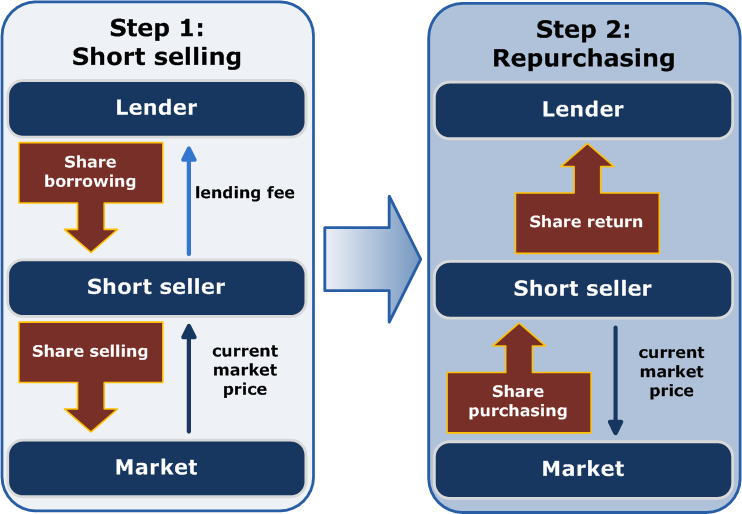

But what if you are bearish? An investor opens a short position by borrowing securities to sell in the open market, hoping to buy them back later at a lower price to return to the lender. A short position represents a bearish trading strategy. The risk here is mathematically terrifying. Because a stock's price can theoretically rise to infinity, the maximum potential loss on a short stock position is theoretically unlimited.

Covered vs. Naked Strategies

Because financial markets offer complex instruments like options and short selling, investors can execute trades that expose them to massive liabilities. Regulators categorize these strategies based on whether the investor possesses a safety net.

- Covered Strategies: An investor executing a covered strategy owns the underlying security. Alternatively, an investor executing a covered strategy may hold an offsetting position instead of owning the underlying security outright. Because the investor has the assets to meet their obligations if the market moves against them, covered strategies reduce the risk of loss compared to naked strategies.

- Naked Strategies: An investor executing a naked strategy lacks ownership of the underlying security. Furthermore, an investor executing a naked strategy lacks an offsetting position to mitigate risk. If the market swings violently, they must purchase the security at current, potentially ruinous market prices to fulfill their obligation. Thus, naked strategies carry high risk due to full exposure to adverse price movements.

In the heavily regulated securities industry, knowing who made the decision to trade is just as crucial as the trade itself. A registered representative cannot simply trade on a client's behalf on a whim.

Non-Discretionary vs. Discretionary Orders

By default, all client accounts are non-discretionary. A non-discretionary order requires the customer to specify the exact trading action (buy or sell), the exact asset (e.g., Apple stock), and the trade quantity (e.g., 100 shares). The industry colloquially refers to this as the "Three A's": Action, Asset, and Amount. If the client provides all three, the representative is merely an order-taker.

If a registered representative makes decisions regarding any of the Three A's, they are exercising discretionary authority:

- A registered representative exercising discretionary authority chooses the specific trading action without client consultation.

- A registered representative exercising discretionary authority chooses the specific asset without client consultation.

- A registered representative exercising discretionary authority chooses the specific trade quantity without client consultation.

Because this grants immense power to the broker, the regulatory hurdles are stringent. A registered representative must obtain written authorization from a client prior to executing a discretionary order. Furthermore, a firm principal must approve a discretionary account in writing before the first discretionary trade occurs.

The Time and Price Exception: What if a client says, "Buy 100 shares of Apple today whenever you think the price is right"? The client has specified the Action, the Asset, and the Amount. Therefore, a registered representative deciding only the time of execution does not constitute discretionary authority, and a registered representative deciding only the price of execution does not constitute discretionary authority.

However, this freedom is strictly temporary. Time and price discretion granted by a customer is valid only for the business day on which the customer grants the discretion. If the sun sets and the trade isn't done, the broker cannot carry that discretion into tomorrow.

Solicited vs. Unsolicited Trades

Even within a non-discretionary account, FINRA meticulously tracks where the initial spark for a trade originated. This helps regulators monitor for suitable recommendations and potential market manipulation.

- A solicited order occurs when a registered representative recommends a specific trade to a customer. Even if the customer makes the final decision, the idea came from the professional.

- An unsolicited order occurs when a customer initiates a trade idea without a recommendation from the registered representative.

To maintain a flawless audit trail, firms must explicitly mark order tickets to indicate whether a trade was solicited, and firms must explicitly mark order tickets to indicate whether a trade was unsolicited. Similarly, firms must explicitly mark order tickets to indicate whether a trade was discretionary.

As a professional in this industry, the order ticket is your legal footprint. By ensuring every ticket correctly reflects the order parameters, the firm's capacity, and the origin of the decision, you uphold the structural integrity that makes modern capital markets possible.