Strategies for Mitigation of Risk

A naval architect never designs a ship with a single, massive, hollow hull. If a breach occurs, the entire vessel floods and sinks. Instead, they divide the hull into watertight compartments. A breach in one section is contained, allowing the ship to stay afloat and navigate to port. In finance, constructing an investment portfolio requires the exact same structural engineering. A client’s life savings cannot be entirely exposed to the failure of a single company, nor can it drift aimlessly as market forces batter its hull. As a future registered representative, your mandate is to build and maintain these financial bulkheads. The tools at your disposal are diversification, rebalancing, and hedging.

Before we can protect a portfolio, we must lay its foundation. This begins with asset allocation, which is the process of deciding how to distribute an investor's wealth among different asset classes. The primary asset classes include equities (stocks), fixed-income securities (bonds), and cash equivalents (money market funds, Treasury bills). How you allocate capital among these categories dictates the fundamental risk and return expectations of the portfolio.

Once the allocation is set, we employ diversification. Diversification is an investment strategy that spreads capital across different assets, sectors, or asset classes. You are not merely buying many things; you are buying many different kinds of things.

The Core Objective: The primary goal of diversification is to reduce the overall volatility of an investment portfolio.

The Physics of Risk: Systematic vs. Unsystematic

To understand why diversification works, we must understand the nature of financial risk. Risk in the markets is not a monolithic force; it comes in two distinct flavors.

- Unsystematic Risk: This is the financial risk specific to a single company or industry. A pharmaceutical firm failing an FDA trial, a CEO scandal, or a massive factory fire—these events destroy value for one specific asset but leave the broader market untouched. Unsystematic risk is also referred to as business risk or specific risk.

- Systematic Risk: This is the inherent risk of an entire market or asset class declining in value. Wars, global pandemics, surging interest rates, and macroeconomic recessions affect everything. Systematic risk is also referred to as market risk.

Here is the grand unified theory of portfolio construction: Diversification reduces unsystematic risk within an investment portfolio, but diversification cannot eliminate systematic risk.

If you own fifty pharmaceutical stocks, you have diversified away the unsystematic risk of a single company going bankrupt, but you are still fully exposed to the unsystematic risk of the healthcare sector. If you own stocks across twenty different industries, you have diversified away industry risk, but a global recession (systematic risk) will still pull the entire portfolio down.

| Risk Type | Alternate Names | Cause | Mitigated By |

|---|---|---|---|

| Unsystematic | Business Risk, Specific Risk | Company/Industry-specific events | Diversification |

| Systematic | Market Risk | Macroeconomic events, interest rates | Hedging, Asset Allocation |

The Math of Correlation

How do we measure the effectiveness of our diversification? We use a statistical concept called correlation. Correlation measures how the prices of two assets move in relation to each other.

If Asset A and Asset B move in perfect lockstep, their correlation is high (positive). Buying both provides almost zero diversification benefit. You have simply bought twice as much of the same structural risk. Conversely, assets with low or negative correlation provide the greatest diversification benefit when combined in a portfolio. If Asset A zigs while Asset B zags, the overall volatility of the portfolio is dramatically smoothed out.

For retail investors who lack the capital to buy hundreds of individual, non-correlated stocks and bonds, mutual funds and exchange-traded funds (ETFs) provide built-in diversification by holding baskets of various securities. By purchasing a single share of an S&P 500 ETF, an investor instantly owns a fraction of 500 distinct companies.

A portfolio is not a static object. Because financial markets are dynamic, a portfolio is subject to constant drift.

Imagine you build a portfolio with a target asset allocation of 60% equities and 40% fixed-income securities. Over the next year, a massive bull market causes the equities to soar in value, while the fixed-income portion remains relatively flat. Without you doing anything, your portfolio's actual allocation might become 75% equities and 25% fixed-income. Market price fluctuations cause a portfolio's actual asset allocation to drift away from the target asset allocation over time.

Because equities carry higher risk than bonds, this drift means your client is now exposed to significantly more risk than they originally agreed to.

The Mechanics of Realignment

Portfolio rebalancing is the process of realigning the asset weightings of a portfolio to their original target percentages. The fundamental purpose of portfolio rebalancing is to maintain the investor's desired risk-reward profile.

To restore the portfolio to its 60/40 target, you must execute two deliberate actions:

- Rebalancing requires an investor to sell a portion of outperforming asset classes (in this case, the equities).

- Rebalancing requires an investor to buy more of underperforming asset classes (in this case, the fixed-income securities).

Notice the psychological brilliance of this mechanical process. Human emotion begs us to buy more of what is going up and sell what is going down. Rebalancing forces discipline: you systematically sell high and buy low.

Timing and Friction

When do we rebalance? Professionals generally use one of two methodologies:

- Periodic rebalancing: This occurs automatically at set time intervals such as quarterly or annually, regardless of market performance.

- Tolerance-band rebalancing: This occurs when an asset class weight deviates from the target allocation by a predetermined percentage (e.g., if any asset class drifts more than 5% from its target, a rebalance is triggered).

Regulatory Warning: Rebalancing is mathematically elegant but carries real-world friction. Selling appreciated assets during portfolio rebalancing can trigger capital gains taxes in taxable brokerage accounts. As a representative, you must weigh the benefit of restoring the risk profile against the tax drag of realizing those gains. (Note: Rebalancing inside tax-advantaged accounts like IRAs does not trigger these immediate capital gains).

If diversification is your ship's watertight compartments, hedging is the life raft.

Hedging is an investment strategy designed to offset potential financial losses in a companion investment. While diversification involves buying inherently different assets to reduce overall volatility, hedging involves taking a very specific, targeted position designed to move in the exact opposite direction of an asset you already own.

Because hedging requires a highly specific, asymmetrical payoff, hedging an equity position is commonly achieved using derivative contracts. Specifically, options contracts are the primary derivative tools used by retail investors to hedge equity positions.

The Cost of Protection

Insurance is never free. Establishing a hedging strategy using options requires the investor to pay an upfront premium.

If you own a $500,000 house, you pay a $2,000 annual premium to insure it against fire. If the house doesn't burn down, you lose the $2,000. Finance works the same way. The cost of an options premium reduces the overall potential return of the hedged investment. The goal of a hedge is not to maximize profit; the goal is to survive a worst-case scenario.

Hedging Scenarios in Practice

Let's examine how professionals use these tools to mitigate specific directional risks.

1. The Long Stock Position (Protecting Against the Floor)

When an investor buys a stock (goes long), they want the price to rise. However, a long stock position carries the risk of the stock price falling to zero.

To hedge this downside market risk, the investor can execute a protective put strategy, which simply means buying a put option on a currently owned stock. A put option gives the buyer the right to sell the stock at a specified strike price. If the stock drops to zero, the investor can exercise the put option and force the market to buy the shares at the strike price, capping their catastrophic loss.

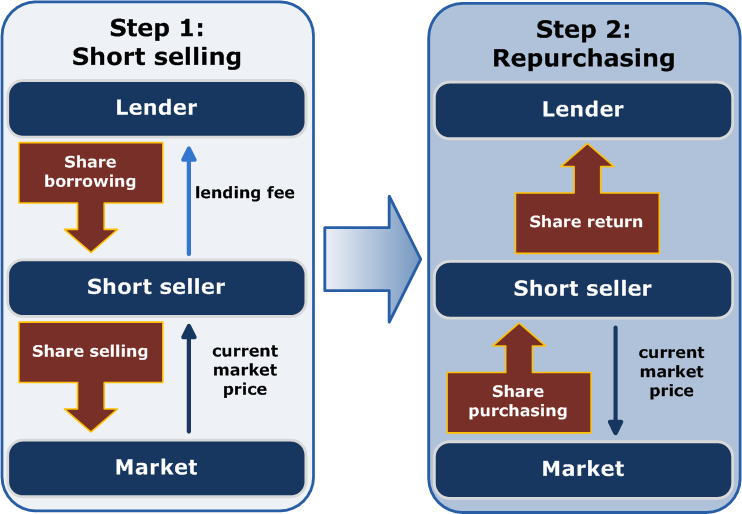

2. The Short Stock Position (Protecting Against the Sky)

When an investor shorts a stock, they borrow shares and sell them, hoping to buy them back later at a lower price. This is deeply dangerous. Because a stock's price has no mathematical ceiling, a short stock position carries theoretically unlimited risk if the stock price rises.

To mitigate this upside market risk, the investor must secure the right to buy the stock back at a fixed price, no matter how high the market goes. Therefore, buying a call option hedges a short stock position against upside market risk.

3. Broad Market Risk (Hedging the Systematic)

What if the investor owns a massive, beautifully diversified portfolio of 500 stocks, but fears a global macroeconomic crash? Buying put options on 500 individual stocks is cost-prohibitive.

Instead, investors use inverse exchange-traded funds (ETFs). These funds use sophisticated derivatives internally and are designed to increase in value when their underlying benchmark index declines. Investors use inverse ETFs to hedge a broad equity portfolio against a general market decline (systematic risk). If the market drops 10%, the equity portfolio loses value, but the inverse ETF gains value, softening the blow.

4. International Exposure (The Currency Variable)

When a client invests in foreign assets—say, a Japanese manufacturing firm or European bonds—they are exposed to the fluctuating exchange rates between the U.S. Dollar and foreign currencies. Even if the foreign asset performs perfectly, a highly unfavorable swing in currency values can wipe out the return. Currency risk can be hedged by purchasing foreign currency options or futures contracts, effectively locking in an exchange rate and neutralizing the variable.

Summary of Hedging Strategies

| Companion Position | Primary Risk | Appropriate Hedging Tool | Result |

|---|---|---|---|

| Long Stock | Price falls to zero | Buy a Put Option (Protective Put) | Locks in a floor selling price |

| Short Stock | Price rises infinitely | Buy a Call Option | Locks in a ceiling purchase price |

| Broad Equity Portfolio | General market decline | Buy an Inverse ETF | Offsets systemic market losses |

| Foreign Investments | Exchange rate volatility | Currency Options / Futures | Neutralizes currency devaluation |

As you prepare for your SIE exam and your subsequent career, remember that generating returns is only half the job of the financial industry. The other half—often the more vital half—is the rigorous, systematic management of risk. Through proper asset allocation, disciplined rebalancing, and strategic hedging, you ensure that when the inevitable storms hit the financial markets, your client's ship remains afloat.